2026年4月中部電力市場結構性價格飆升:JERA鯨魚效應與JPX中部期貨上市

## 事件背景:一份合約的終止如何撼動整個市場

2026年3月31日,一份在電力業界幾乎無人不知的合約悄然到期。JERA——由東京電力與中部電力合資成立、目前是日本最大的發電事業者——與其母公司旗下的零售子公司東京電力エナジーパートナー(東電EP)及中部電力ミライズ之間的「集團內部電力購售協議(Group PPA)」正式終止。

這份協議的存在,意味著JERA所生產的大量電力可以繞過公開市場、直接以議定價格供應給集團內的零售商。協議終止後,這部分電力必須轉入JEPX現貨市場公開競標,而東電EP與中部電ミライズ也必須從市場上重新採購。

結果是立竿見影的。4月1日受渡分的JEPX現貨市場,系統プライス平均值跳升至¥23.15/kWh,最高值達¥34.6/kWh,東京エリアプライス日均值更達¥26.96/kWh。

## 鯨魚入海:東電EP與中部電ミライズ的採購行為轉變

市場分析師以「鯨魚(クジラ)」來形容東電EP與中部電ミライズ突然大量進入現貨市場的現象。這兩家公司的客戶基礎龐大,對電力供應有剛性需求,因此在競標時傾向於以高價確保得標,而非以邊際成本思維出價。

根據市場觀察,3月中旬兩家公司的現貨市場調達比率分別僅有約2%(東電EP)與約7%(中部電ミライズ)。進入4月後,東電EP的比率迅速攀升至約30%,中部電ミライズ則接近50%。這種採購行為的劇烈轉變,直接推高了競標曲線的底部,使整個市場的均衡價格上移。

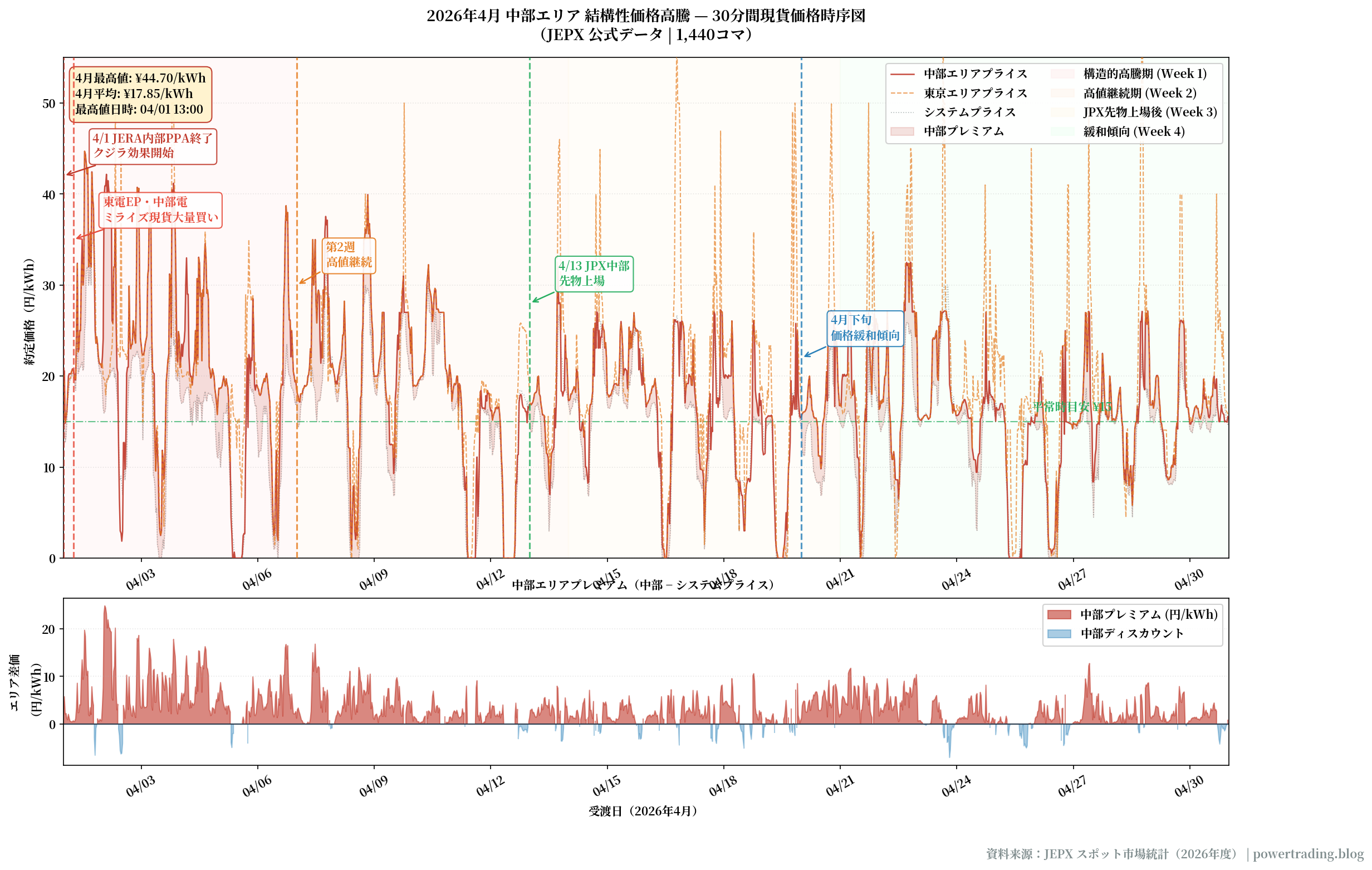

## 中部エリアの価格動態:最高值¥44.70/kWh

中部エリアプライスは4月中に最高¥44.70/kWhを記録した。月平均は¥17.85/kWhで、前月比で大幅な上昇となった。東京エリアとの連系容量制約が、中部エリアの孤立的な価格形成に寄与した局面もあった。

以下の表は4月1日〜14日の主要エリア平均スポット価格を示す:

| エリア | 4月1〜14日平均 | 3月平均 | 前月比 |

|--------|--------------|---------|--------|

| 東京 | ¥21.06/kWh | ¥14.4/kWh | +46% |

| 中部 | ¥19.89/kWh | 約¥13.5/kWh | +47% |

| 関西 | ¥15.02/kWh | 約¥11.0/kWh | +37% |

| 四国 | ¥7.63/kWh | 約¥9.0/kWh | -15% |

中部エリアが東京エリアに次ぐ高水準となった一方、四国エリアは逆に低下するなど、エリア間の価格分散が顕著に拡大した。

## 複合的な価格上昇要因

今回の価格高騰は、単一の原因によるものではなく、複数の要因が重なった構造的な現象である。

**第一の要因:JERAの限界費用入札とJKM連動**。JERAは市場競争法規に基づき、限界費用入札を実施している。2026年4月時点でアジア向けLNGスポット指標(JKM)は高水準で推移しており、これがJERAの入札価格のベースラインを押し上げた。

**第二の要因:中東情勢による燃料価格上昇**。イラン関連の地政学的リスクがLNG供給懸念を高め、燃料コストの上昇圧力となった。

**第三の要因:春季の需給構造**。春季は需要が低下するため通常は価格が低位に推移するが、2026年4月は太陽光発電量が低下した日に残余需要が高水準で推移し、特に夕方から夜間にかけて価格が急騰した。18時台には¥30/kWh超の水準となる日も複数確認された。

**第四の要因:市場調整項の転嫁構造**。多くの小売電気事業者が契約に「市場調整項」を設けており、スポット価格の上昇分が自動的に需要家の電気料金に転嫁される仕組みになっている。これにより、価格高騰の影響が実需要家にまで波及した。

## JPX中部電力先物の上場:ヘッジ手段の拡充

価格高騰が続く中、2026年4月13日にはJPX(東京商品取引所、TOCOMグループ)が中部エリア電力先物の取引を開始した。これは中部エリアにとって初めての国内取引所上場先物であり、市場参加者のリスクヘッジ手段が大幅に拡充された。

上場初日の取引は30契約(計1.47百万kWh)で、7月・8月・9月限月各5契約が成立した。ベースロード決済価格は¥22.2/kWh、昼間ロード決済価格は¥28.15/kWhで初値が形成された。初回の買い方は長野県松本市の情熱電力、売り方はEREXが務めた。

EEXは既に中部エリア先物を取り扱っていたが、TOCOM上場によって国内市場での流動性向上が期待される。東邦ガスなど中部エリアの主要小売事業者も「先物取引の拡大に期待する」とコメントしている。

## 電力自由化10周年の節目に問われる市場設計

2026年4月1日は、日本の電力小売完全自由化からちょうど10周年にあたる節目であった。その記念すべき日に、市場最大のプレーヤーが公開市場に参入し、価格が急騰したという事実は、日本の電力市場設計に対する重要な問いを投げかけている。

集団内PPAの終了は、市場の流動性を高めるという観点では望ましい変化である。しかし、その移行が急激であったために、市場参加者が対応する時間的余裕を持てなかった。電力・ガス取引監視等委員会は4月20日の第605回委員会においてこの問題を議題に取り上げており、今後の制度的な対応が注目される。

## 実務的示唆:小売事業者と需要家へのインプリケーション

今回の事件は、日本の電力市場における構造的なリスクを改めて浮き彫りにした。小売電気事業者にとっては、TOCOM先物や相対取引を活用した調達ポートフォリオの多様化が急務であり、特に中部エリアにおける先物ヘッジ比率の引き上げが推奨される。

需要家にとっては、市場連動型料金プランのリスクを再評価する機会となった。固定価格プランと市場連動プランの組み合わせ、あるいはコーポレートPPAによる価格安定化が有効な選択肢となりうる。

電力自由化10年を経て、日本の電力市場は成熟しつつある。しかし、今回のような構造的変化が価格に与える影響の大きさは、市場設計の継続的な改善と、参加者のリスク管理能力の向上が依然として重要な課題であることを示している。2026年4月 中部エリア構造的価格高騰:JERAクジラ効果とJPX中部先物上場

## 事件の背景:一つの契約終了が市場を揺るがす

2026年3月31日、電力業界で広く知られた一つの契約が静かに終了した。東京電力と中部電力の合弁会社として設立され、現在日本最大の発電事業者であるJERAと、その親会社グループ傘下の小売子会社である東京電力エナジーパートナー(東電EP)および中部電力ミライズとの間の「グループ内電力売買契約(グループ内PPA)」が正式に終了したのである。

この契約の存在は、JERAが生産した大量の電力が公開市場を経由せず、合意価格で直接グループ内小売業者に供給されることを意味していた。契約終了後、この電力はJEPXスポット市場での公開入札に回り、東電EPと中部電ミライズも市場から再調達しなければならなくなった。

その影響は即座に現れた。4月1日受渡分のJEPXスポット市場では、システムプライス平均値が¥23.15/kWhに跳ね上がり、最高値は¥34.6/kWh、東京エリアプライスの日均値は¥26.96/kWhに達した。

## クジラの入海:東電EP・中部電ミライズの調達行動の変容

市場アナリストは、東電EPと中部電ミライズが突然大量にスポット市場に参入した現象を「クジラ(市場の巨人)」と表現した。両社は膨大な顧客基盤を持ち、電力供給に対する硬直的な需要があるため、入札時には限界費用思考ではなく、高値でも確実に落札しようとする傾向がある。

市場観察によれば、3月中旬の両社のスポット市場調達比率は、東電EPが約2%弱、中部電ミライズが約7%程度に過ぎなかった。4月に入ると、東電EPの比率は約30%へ、中部電ミライズは約50%弱へと急上昇した。この調達行動の急激な変化が、入札カーブの底上げを直接引き起こし、市場全体の均衡価格を押し上げた。

## 中部エリアの価格動態:最高値¥44.70/kWh

中部エリアプライスは4月中に最高¥44.70/kWhを記録した。月平均は¥17.85/kWhで、前月比で大幅な上昇となった。東京エリアとの連系容量制約が、中部エリアの孤立的な価格形成に寄与した局面もあった。

以下の表は4月1日〜14日の主要エリア平均スポット価格を示す:

| エリア | 4月1〜14日平均 | 3月平均 | 前月比 |

|--------|--------------|---------|--------|

| 東京 | ¥21.06/kWh | ¥14.4/kWh | +46% |

| 中部 | ¥19.89/kWh | 約¥13.5/kWh | +47% |

| 関西 | ¥15.02/kWh | 約¥11.0/kWh | +37% |

| 四国 | ¥7.63/kWh | 約¥9.0/kWh | -15% |

中部エリアが東京エリアに次ぐ高水準となった一方、四国エリアは逆に低下するなど、エリア間の価格分散が顕著に拡大した。

## 複合的な価格上昇要因

今回の価格高騰は、単一の原因によるものではなく、複数の要因が重なった構造的な現象である。

**第一の要因:JERAの限界費用入札とJKM連動**。JERAは市場競争法規に基づき、限界費用入札を実施している。2026年4月時点でアジア向けLNGスポット指標(JKM)は高水準で推移しており、これがJERAの入札価格のベースラインを押し上げた。

**第二の要因:中東情勢による燃料価格上昇**。イラン関連の地政学的リスクがLNG供給懸念を高め、燃料コストの上昇圧力となった。

**第三の要因:春季の需給構造**。春季は需要が低下するため通常は価格が低位に推移するが、2026年4月は太陽光発電量が低下した日に残余需要が高水準で推移し、特に夕方から夜間にかけて価格が急騰した。18時台には¥30/kWh超の水準となる日も複数確認された。

**第四の要因:市場調整項の転嫁構造**。多くの小売電気事業者が契約に「市場調整項」を設けており、スポット価格の上昇分が自動的に需要家の電気料金に転嫁される仕組みになっている。これにより、価格高騰の影響が実需要家にまで波及した。

## JPX中部電力先物の上場:ヘッジ手段の拡充

価格高騰が続く中、2026年4月13日にはJPX(東京商品取引所、TOCOMグループ)が中部エリア電力先物の取引を開始した。これは中部エリアにとって初めての国内取引所上場先物であり、市場参加者のリスクヘッジ手段が大幅に拡充された。

上場初日の取引は30契約(計1.47百万kWh)で、7月・8月・9月限月各5契約が成立した。ベースロード決済価格は¥22.2/kWh、昼間ロード決済価格は¥28.15/kWhで初値が形成された。初回の買い方は長野県松本市の情熱電力、売り方はEREXが務めた。

EEXは既に中部エリア先物を取り扱っていたが、TOCOM上場によって国内市場での流動性向上が期待される。東邦ガスなど中部エリアの主要小売事業者も「先物取引の拡大に期待する」とコメントしている。

## 電力自由化10周年の節目に問われる市場設計

2026年4月1日は、日本の電力小売完全自由化からちょうど10周年にあたる節目であった。その記念すべき日に、市場最大のプレーヤーが公開市場に参入し、価格が急騰したという事実は、日本の電力市場設計に対する重要な問いを投げかけている。

グループ内PPAの終了は、市場の流動性を高めるという観点では望ましい変化である。しかし、その移行が急激であったために、市場参加者が対応する時間的余裕を持てなかった。電力・ガス取引監視等委員会は4月20日の第605回委員会においてこの問題を議題に取り上げており、今後の制度的な対応が注目される。

## 実務的示唆:小売事業者と需要家へのインプリケーション

今回の事件は、日本の電力市場における構造的なリスクを改めて浮き彫りにした。小売電気事業者にとっては、TOCOM先物や相対取引を活用した調達ポートフォリオの多様化が急務であり、特に中部エリアにおける先物ヘッジ比率の引き上げが推奨される。

需要家にとっては、市場連動型料金プランのリスクを再評価する機会となった。固定価格プランと市場連動プランの組み合わせ、あるいはコーポレートPPAによる価格安定化が有効な選択肢となりうる。

電力自由化10年を経て、日本の電力市場は成熟しつつある。しかし、今回のような構造的変化が価格に与える影響の大きさは、市場設計の継続的な改善と、参加者のリスク管理能力の向上が依然として重要な課題であることを示している。Chubu Area Structural Price Spike in April 2026: The JERA Whale Effect and JPX Chubu Futures Listing

## Background: How the Termination of a Single Contract Shook the Market

On March 31, 2026, a contract well-known throughout Japan's electricity industry quietly expired. JERA — established as a joint venture between Tokyo Electric Power and Chubu Electric Power, and currently Japan's largest power generation company — formally terminated its "Group-Internal Power Purchase Agreement (Group PPA)" with its parent companies' retail subsidiaries: TEPCO Energy Partner (TEPCO EP) and Chubu Electric Power Miraiz.

The existence of this agreement meant that a substantial volume of electricity produced by JERA could be supplied directly to these group retailers at agreed prices, bypassing the public market entirely. Following the termination, this electricity had to enter the JEPX spot market for open bidding, while TEPCO EP and Chubu Electric Miraiz were forced to procure from the market anew.

The impact was immediate. For the April 1 delivery date, the JEPX spot market saw the system price average jump to ¥23.15/kWh, with a peak of ¥34.6/kWh and the Tokyo area daily average reaching ¥26.96/kWh.

## The Whale Enters the Water: The Procurement Behavior Shift of TEPCO EP and Chubu Electric Miraiz

Market analysts described the sudden large-scale entry of TEPCO EP and Chubu Electric Miraiz into the spot market as the "whale (kujira) effect." Both companies have enormous customer bases and face inelastic demand for electricity supply. As a result, they tend to bid at high prices to ensure procurement, rather than bidding at marginal cost.

Market observations indicate that in mid-March, the spot market procurement ratios for the two companies were approximately 2% (TEPCO EP) and approximately 7% (Chubu Electric Miraiz) respectively. By April, TEPCO EP's ratio had rapidly climbed to approximately 30%, while Chubu Electric Miraiz approached 50%. This dramatic shift in procurement behavior directly elevated the floor of the bidding curve, pushing the market equilibrium price upward across the board.

## Chubu Area Price Dynamics: Peak at ¥44.70/kWh

The Chubu area price reached a peak of ¥44.70/kWh during April, with a monthly average of ¥17.85/kWh — a substantial increase from the previous month. Transmission capacity constraints between the Chubu and Tokyo areas contributed to isolated price formation in the Chubu region during certain periods.

The following table shows average spot prices for major areas from April 1 to 14:

| Area | Apr 1–14 Average | March Average | Month-on-Month |

|------|-----------------|---------------|----------------|

| Tokyo | ¥21.06/kWh | ¥14.4/kWh | +46% |

| Chubu | ¥19.89/kWh | ~¥13.5/kWh | +47% |

| Kansai | ¥15.02/kWh | ~¥11.0/kWh | +37% |

| Shikoku | ¥7.63/kWh | ~¥9.0/kWh | -15% |

While Chubu recorded the second-highest prices after Tokyo, Shikoku actually declined, highlighting a notable expansion of inter-area price divergence.

## Multiple Compounding Factors Behind the Price Surge

The price spike was not caused by a single factor, but rather represented a structural phenomenon driven by the convergence of multiple forces.

**First factor: JERA's marginal cost bidding and JKM linkage.** JERA submits bids based on marginal cost in compliance with market competition regulations. In April 2026, the Japan Korea Marker (JKM) — the Asian LNG spot price benchmark — was trading at elevated levels, which pushed up the baseline of JERA's bid prices.

**Second factor: Fuel price increases due to Middle East tensions.** Geopolitical risks related to Iran heightened concerns about LNG supply, creating upward pressure on fuel costs.

**Third factor: Spring demand-supply dynamics.** While spring typically sees lower demand and lower prices, April 2026 saw elevated residual demand on days with reduced solar generation output, with prices spiking particularly in the evening and nighttime hours. Multiple days recorded prices exceeding ¥30/kWh in the 18:00 time slot.

**Fourth factor: Market adjustment clause pass-through.** Many retail electricity suppliers have incorporated "market adjustment clauses" into their contracts, automatically passing through spot price increases to end consumers. This mechanism caused the price spike to ripple through to actual electricity users.

## JPX Chubu Electricity Futures Listing: Expanding Hedging Tools

Amid the ongoing price surge, JPX (Tokyo Commodity Exchange, TOCOM Group) commenced trading of Chubu area electricity futures on April 13, 2026. This marked the first domestic exchange-listed futures for the Chubu area, significantly expanding the risk hedging tools available to market participants.

On the first day of trading, 30 contracts (totaling 1.47 million kWh) were executed, with 5 contracts each for the July, August, and September maturities. The base load settlement price was established at ¥22.2/kWh, and the daytime load settlement price at ¥28.15/kWh. The first buyer was Jounetsu Denryoku (based in Matsumoto, Nagano Prefecture), and the first seller was EREX.

While EEX had already been offering Chubu area futures, the TOCOM listing is expected to improve liquidity in the domestic market. Major Chubu area retailers including Toho Gas have expressed expectations for increased futures trading activity.

## Market Design Questions at the 10th Anniversary of Full Liberalization

April 1, 2026 marked exactly the 10th anniversary of Japan's full retail electricity liberalization. The fact that on this milestone date, the market's largest player entered the public market and prices surged dramatically raises important questions about Japan's electricity market design.

The termination of the group-internal PPA is a welcome development from the perspective of improving market liquidity. However, the abruptness of the transition left market participants insufficient time to adapt. The Electricity and Gas Market Surveillance Commission addressed this issue at its 605th meeting on April 20, and institutional responses going forward will be closely watched.

## Practical Implications: For Retailers and End Consumers

This event has once again highlighted the structural risks inherent in Japan's electricity market. For retail electricity suppliers, diversifying procurement portfolios through TOCOM futures and bilateral contracts is urgent, with particular emphasis on increasing the futures hedging ratio in the Chubu area.

For end consumers, this event provides an opportunity to reassess the risks of market-linked pricing plans. A combination of fixed-price and market-linked plans, or price stabilization through corporate PPAs, may be effective options.

Ten years into electricity liberalization, Japan's electricity market is maturing. Yet the magnitude of the price impact from structural changes such as this one demonstrates that continuous improvement of market design and enhancement of participants' risk management capabilities remain critical challenges.