FY2026 日本時間前市場全面改革:透明化、5區域制與BESS套利新策略

背景:為何 FY2026 是時間前市場的轉折點

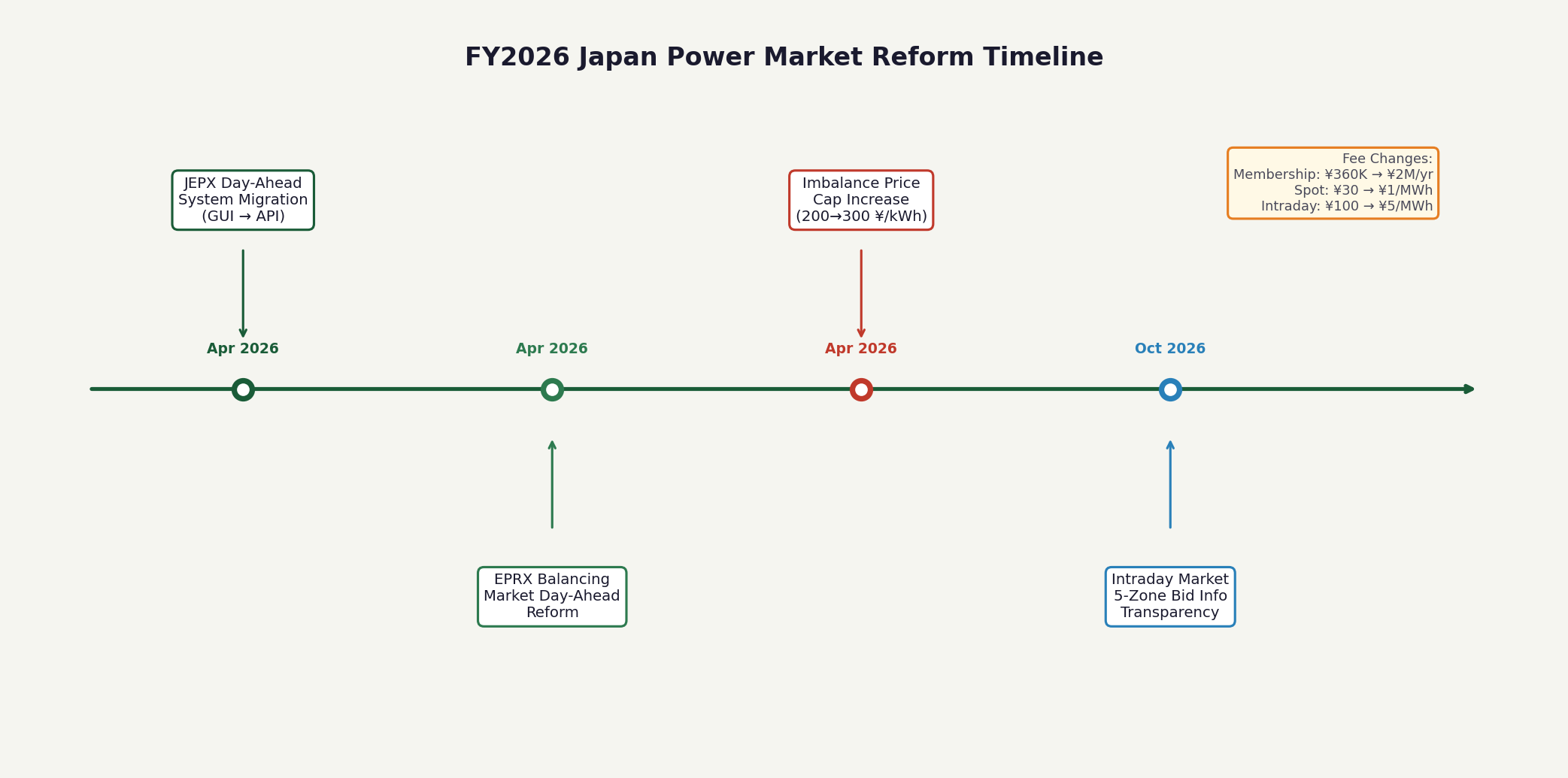

日本時間前市場(時間前市場,Intraday Market)自2005年開設以來,長期扮演「現貨市場的補充角色」——交易量僅占現貨的5–8%,流動性薄弱,價差不透明。然而,FY2026 將以三項同步改革打破這一格局:JEPX 系統 API 全面遷移(4月)、不平衡料金上限擴大(4月)、以及5區域投標透明化(10月)。這三項改革的疊加效應,將使時間前市場從「緊急調度工具」轉型為「主動套利場域」。

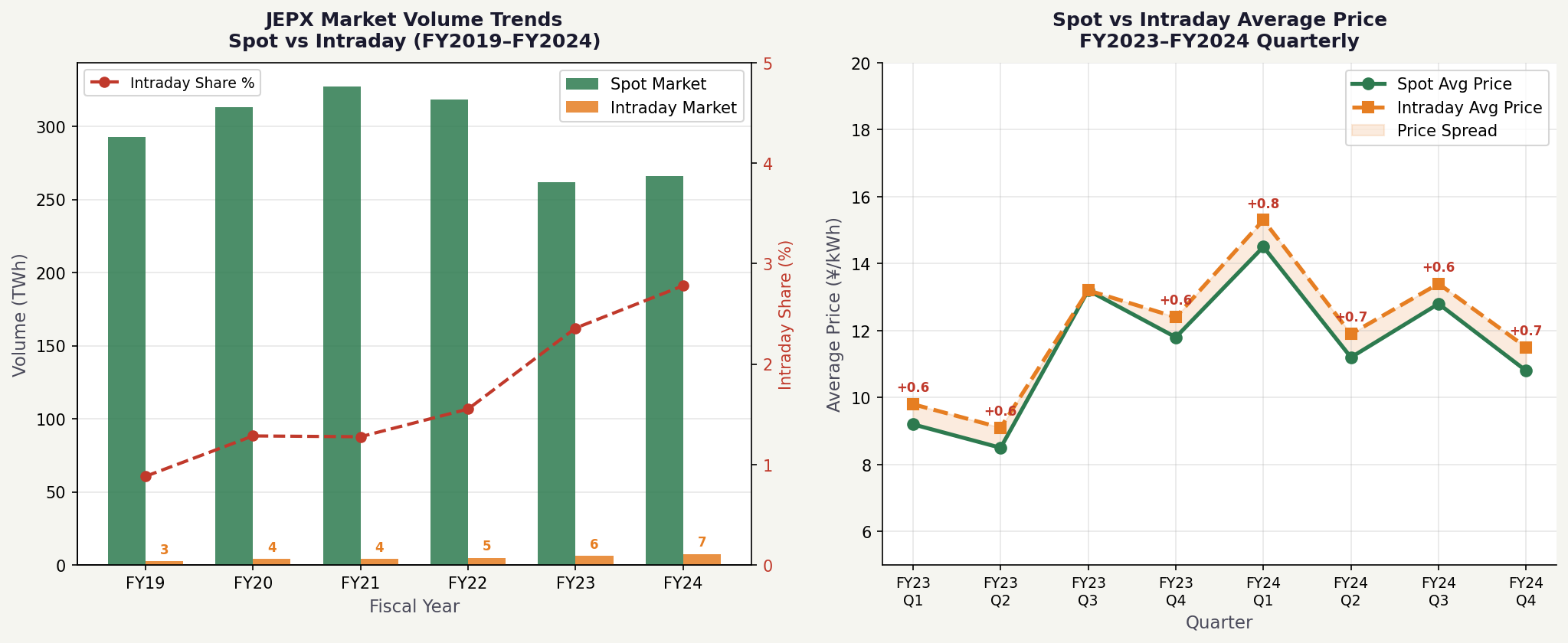

從數量面看,時間前市場的成長趨勢已相當明確。根據 JEPX 2024年度事業報告書,FY2021 的年間交易量為 5.2 TWh,至 FY2024 已成長至 8.9 TWh,年均複合成長率(CAGR)達 19.7%。相比之下,現貨市場同期成長率僅約 3–4%。這一差距反映了市場參與者對近即時調度工具的需求正在快速上升,尤其是再生能源滲透率提高後,日內電力供需波動加劇所帶來的結構性需求。

三大改革詳解

改革一:JEPX API 全面遷移(2026年4月)

JEPX 將於 2026年4月 完成交易系統 API 的全面遷移,從舊版 FTP 批次下載模式升級為 RESTful API 即時串流。這一變化看似技術性,實則對市場參與者的競爭格局影響深遠。新 API 提供毫秒級的訂單簿更新(Order Book Update),使具備自動化交易系統的參與者(BESS 運營商、電力交易商)能夠在現貨結果公布後的數分鐘內,即時調整時間前市場的投標策略。

對於尚未建立自動化系統的中小型零售商與再生能源業者而言,API 遷移意味著「資訊不對稱」的加劇。舊版 FTP 模式下,大型業者與小型業者的資訊取得速度差距有限;新 API 環境下,系統整合能力將直接決定套利窗口的捕捉效率。

改革二:不平衡料金上限擴大(2026年4月)

現行制度下,不平衡料金(Imbalance Price)的計算上限設有緩衝機制,使極端價格事件的衝擊被部分吸收。FY2026年4月起,上限將擴大至現貨均價的 ±100%(即最高可達現貨均價的2倍),與歐洲主要電力市場的不平衡定價機制接軌。

此改革的核心邏輯是「強化不平衡懲罰」,迫使市場參與者更積極地利用時間前市場進行倉位平衡(Position Balancing),而非依賴系統運營商的調整力。對 BESS 運營商而言,這是一個雙向機會:一方面,高不平衡風險促使再生能源業者購買更多時間前市場電力,提升市場流動性;另一方面,BESS 自身若持有不平衡倉位,損失也將相應擴大。

改革三:5區域投標透明化(2026年10月)

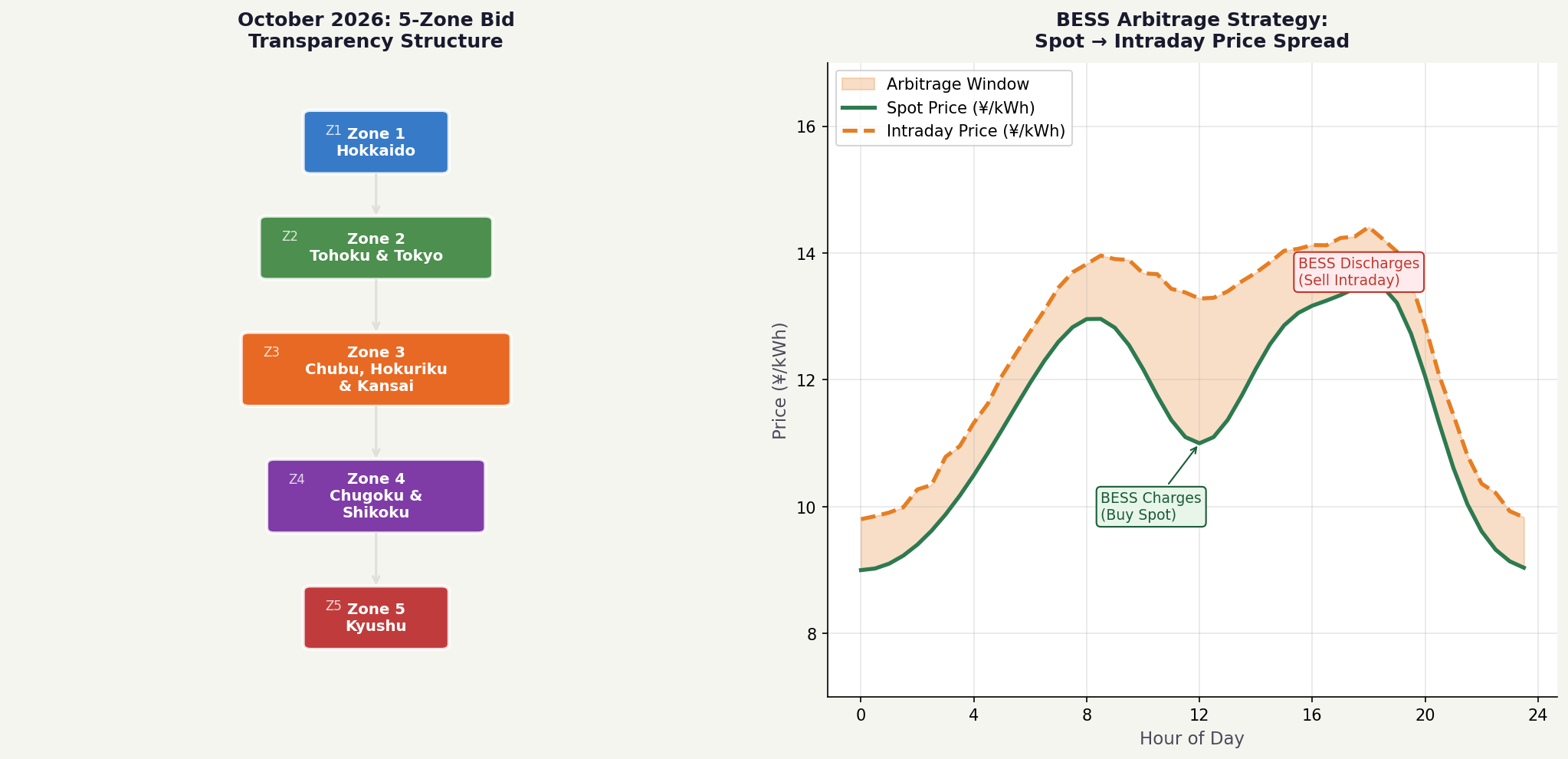

目前時間前市場採用全國統一投標制,區域價差資訊不透明。2026年10月起,JEPX 將引入5區域制(Zone 1: 北海道、Zone 2: 東北・東京、Zone 3: 中部・北陸・關西、Zone 4: 中國・四國、Zone 5: 九州),每個區域的投標量與成交價格將獨立公開。

5區域制的實施將使連系線壅塞(Interconnection Congestion)的價格信號更加清晰。以九州為例,當太陽能大量出力時,九州→中國的連系線往往達到滿載,導致九州現貨價格低於全國均價。在新制度下,Zone 5(九州)的時間前市場價格將獨立反映這一壅塞溢價,為跨區域套利提供更精確的定價基礎。

現貨-時間前價差:套利機會的量化分析

時間前市場的核心套利邏輯在於捕捉「現貨結算價」與「時間前成交價」之間的價差。根據 METI FY2024 監控報告的數據,全國平均現貨-時間前價差約為 ¥0.8–1.5/kWh,但區域與時段分布高度不均。

在時段分布上,早峰(07:00–09:00)與晚峰(17:00–21:00)的價差最為顯著,平均達 ¥1.2–2.0/kWh。這與太陽能出力的日內波動直接相關:正午前後太陽能大量出力壓低現貨價,而晚峰時段太陽能退出後,現貨價迅速回升,時間前市場往往提前反映這一預期,形成可捕捉的套利窗口。

在區域分布上,九州(Zone 5)的價差最大,FY2024 年均達 ¥1.8/kWh,遠高於東京(Zone 2)的 ¥0.6/kWh。這一差距源於九州高達38%的再生能源比例與有限的連系線容量,使日內供需波動更為劇烈。

BESS 套利策略框架

對於 BESS 運營商而言,FY2026 改革提供了一個結構性套利機會:在現貨市場低價時段(通常為正午太陽能高出力期)充電,在時間前市場高價時段(晚峰前後)放電出售。這一「現貨充電→時間前放電」策略的可行性,取決於三個關鍵條件:

第一,充放電價差須覆蓋 BESS 的往返效率損失(通常為 15–20%)與系統使用費。以典型 BESS 系統(往返效率85%)為例,若現貨均價為 ¥10/kWh,時間前均價為 ¥12.5/kWh,則每 kWh 的套利利潤約為 ¥12.5 × 0.85 - ¥10 = ¥0.625/kWh,扣除系統使用費(約 ¥0.3/kWh)後,淨利潤約 ¥0.3/kWh。

第二,API 整合能力決定套利窗口的捕捉效率。FY2026年4月 API 遷移後,具備自動化投標系統的 BESS 運營商可在現貨結果公布後的 5–10 分鐘內完成時間前市場的投標調整,而依賴人工操作的業者可能錯失最佳價差窗口。

第三,區域選擇至關重要。5區域制實施後,九州(Zone 5)與中國(Zone 4)的時間前市場將呈現最大的區域價差,是 BESS 套利的優先部署區域。

各參與者類型的差異化衝擊

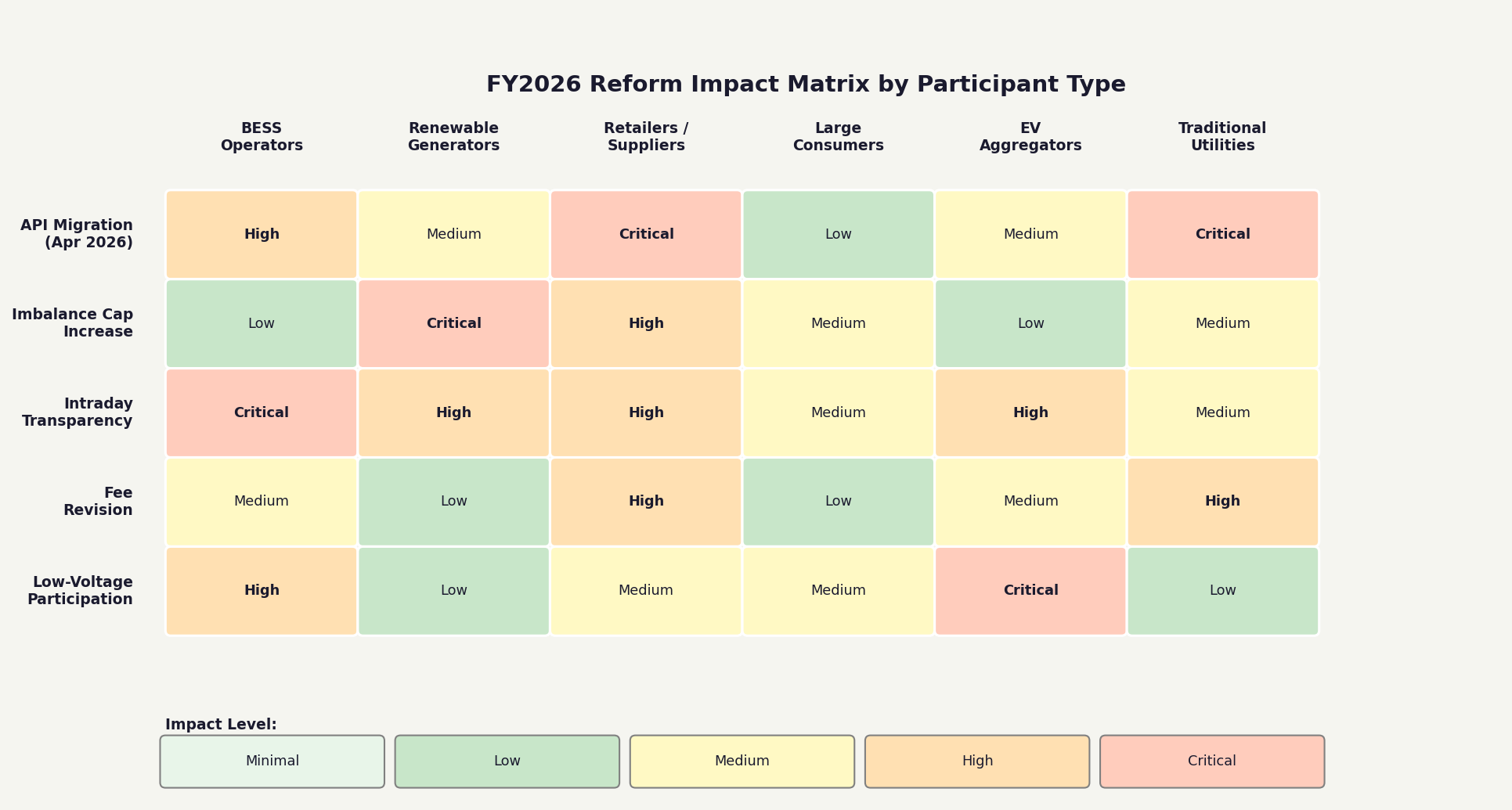

三大改革對不同市場參與者的衝擊程度差異顯著。下表整理了各改革對六類主要參與者的影響評估:

| 改革項目 | BESS運營商 | 再生能源業者 | 零售商/供應商 | 大型需求端 | EV聚合商 | 傳統電力公司 |

|---|---|---|---|---|---|---|

| API遷移(4月) | 高 | 中 | 關鍵 | 低 | 中 | 關鍵 |

| 不平衡上限擴大(4月) | 低 | 關鍵 | 高 | 中 | 低 | 中 |

| 5區域透明化(10月) | 關鍵 | 高 | 高 | 中 | 高 | 中 |

| 手續費調整 | 中 | 低 | 高 | 低 | 中 | 高 |

| 低壓參與開放 | 高 | 低 | 中 | 中 | 關鍵 | 低 |

低壓參與開放:FY2026 的隱藏機會

除三大主要改革外,FY2026 還將推進低壓(低圧、100V/200V)需求端資源參與時間前市場的試行計畫。目前時間前市場的最小交易單位為 0.1 MW(100 kW),對住宅太陽能、小型商業 BESS 等低壓資源而言門檻過高。試行計畫將引入聚合商(Aggregator)機制,允許多個低壓資源打包參與,最小聚合規模預計降至 1 MW。

這一機制對 EV 聚合商(V2G 服務商)尤為重要。日本 EV 保有量在 FY2025 已突破 150 萬輛,若 10% 的 EV 參與 V2G 聚合,理論上可提供約 750 MW 的可調度容量,相當於一座中型燃氣電廠。低壓參與開放將使這一潛在容量得以進入時間前市場,為 EV 車主創造額外收益,同時為電網提供分散式調頻資源。

結語:FY2026 是時間前市場的「元年」

FY2026 的三大改革將從根本上改變日本時間前市場的競爭格局。對於已建立自動化交易系統、具備 API 整合能力的 BESS 運營商而言,這是一個難得的先發優勢窗口:在市場流動性尚未充分提升、價差仍然顯著的過渡期,系統化的套利策略可帶來可觀的超額收益。

然而,改革也帶來了新的風險。不平衡上限擴大意味著倉位管理失誤的代價更高;5區域透明化雖提升了定價效率,也加速了套利機會的消失速度。市場參與者需要在「把握先發優勢」與「控制尾部風險」之間找到平衡,而這正是 FY2026 時間前市場競爭的核心命題。

FY2026 日本時間前市場の全面改革:透明化・5ゾーン制・BESS裁定の新戦略

背景:なぜFY2026が時間前市場の転換点なのか

日本の時間前市場は2005年の開設以来、「現物市場の補完的役割」を担ってきた。取引量は現物市場の5〜8%に留まり、流動性は薄く、価格差の透明性も低かった。しかしFY2026には、3つの改革が同時に実施される。JEPX取引システムAPIの全面移行(4月)、インバランス料金上限の拡大(4月)、そして5ゾーン入札透明化(10月)だ。これら3改革の複合効果により、時間前市場は「緊急調整ツール」から「能動的裁定の場」へと転換する。

取引量の成長トレンドはすでに明確だ。JEPX 2024年度事業報告書によれば、FY2021の年間取引量は5.2 TWhだったが、FY2024には8.9 TWhへと成長し、年平均成長率(CAGR)は19.7%に達する。同期間の現物市場成長率が3〜4%程度であることと比較すると、この差は市場参加者の近リアルタイム調整ニーズの急速な高まりを示している。特に再エネ浸透率の上昇に伴う日内需給変動の拡大が、構造的な需要を生み出している。

3大改革の詳細

改革1:JEPX API全面移行(2026年4月)

JEPXは2026年4月に取引システムAPIの全面移行を完了し、旧来のFTPバッチダウンロード方式からRESTful APIリアルタイムストリーミングへ移行する。この変更は技術的に見えるが、市場参加者の競争環境に深く影響する。新APIはミリ秒単位のオーダーブック更新を提供し、自動取引システムを持つ参加者(BESS事業者、電力トレーダー)が現物結果公表後数分以内に時間前市場の入札戦略をリアルタイムで調整できるようになる。

自動化システムを持たない中小規模の小売事業者や再エネ事業者にとって、API移行は「情報非対称性」の拡大を意味する。旧FTP方式では大手と中小の情報取得速度の差は限定的だったが、新API環境ではシステム統合能力が裁定窓口の捕捉効率を直接左右する。

改革2:インバランス料金上限拡大(2026年4月)

現行制度ではインバランス料金の計算上限に緩衝機能があり、極端な価格イベントの影響が一部吸収されていた。FY2026年4月からは上限が現物均価の±100%(最大で現物均価の2倍)に拡大され、欧州主要電力市場のインバランス価格メカニズムに近づく。

この改革の核心は「インバランスペナルティの強化」であり、市場参加者がシステム運用者の調整力に依存するのではなく、時間前市場を積極的に活用してポジションバランスを取るよう促す。BESS事業者にとっては双方向の機会だ。高インバランスリスクが再エネ事業者の時間前市場電力購入を促し流動性を高める一方、BESS自身がインバランスポジションを持つ場合の損失も拡大する。

改革3:5ゾーン入札透明化(2026年10月)

現在の時間前市場は全国統一入札制を採用しており、地域価格差情報が不透明だ。2026年10月からJEPXは5ゾーン制(Zone 1: 北海道、Zone 2: 東北・東京、Zone 3: 中部・北陸・関西、Zone 4: 中国・四国、Zone 5: 九州)を導入し、各ゾーンの入札量と約定価格が独立して公開される。

5ゾーン制の実施により、連系線混雑の価格シグナルがより明確になる。九州を例にとると、太陽光が大量出力する際、九州→中国の連系線はしばしば満潮に達し、九州の現物価格が全国平均を下回る。新制度下ではZone 5(九州)の時間前市場価格がこの混雑プレミアムを独立して反映し、地域間裁定のより精確な価格基盤を提供する。

現物-時間前価格差:裁定機会の定量分析

時間前市場の核心的な裁定ロジックは「現物決済価格」と「時間前約定価格」の価格差を捕捉することにある。METI FY2024監視レポートのデータによれば、全国平均の現物-時間前価格差は約¥0.8〜1.5/kWhだが、地域・時間帯分布は高度に不均一だ。

時間帯分布では、朝ピーク(07:00〜09:00)と夕方ピーク(17:00〜21:00)の価格差が最も顕著で、平均¥1.2〜2.0/kWhに達する。これは太陽光出力の日内変動と直接関連している。正午前後に太陽光が大量出力して現物価格を押し下げ、夕方ピーク時に太陽光が退出すると現物価格が急回復する。時間前市場はこの予測を先取りして価格形成し、捕捉可能な裁定窓口を生み出す。

地域分布では、九州(Zone 5)の価格差が最大で、FY2024年平均は¥1.8/kWhと、東京(Zone 2)の¥0.6/kWhを大きく上回る。この差は九州の38%という高い再エネ比率と限られた連系線容量が日内需給変動をより激しくすることに起因する。

BESS裁定戦略フレームワーク

BESS事業者にとって、FY2026改革は構造的な裁定機会を提供する。現物市場の低価格時間帯(通常は太陽光高出力の正午)に充電し、時間前市場の高価格時間帯(夕方ピーク前後)に放電販売する「現物充電→時間前放電」戦略の実行可能性は、3つの重要条件に依存する。

第1に、充放電価格差がBESSのラウンドトリップ効率損失(通常15〜20%)とシステム利用料をカバーする必要がある。典型的なBESSシステム(ラウンドトリップ効率85%)を例にとると、現物均価が¥10/kWh、時間前均価が¥12.5/kWhの場合、1kWh当たりの裁定利益は¥12.5×0.85−¥10=¥0.625/kWhとなり、システム利用料(約¥0.3/kWh)を差し引いた純利益は約¥0.3/kWhとなる。

第2に、API統合能力が裁定窓口の捕捉効率を決定する。FY2026年4月のAPI移行後、自動入札システムを持つBESS事業者は現物結果公表後5〜10分以内に時間前市場の入札調整を完了できるが、手動操作に依存する事業者は最適な価格差窓口を逃す可能性がある。

第3に、地域選択が極めて重要だ。5ゾーン制実施後、九州(Zone 5)と中国(Zone 4)の時間前市場は最大の地域価格差を示し、BESS裁定の優先展開地域となる。

各参加者タイプへの差異化インパクト

3大改革が異なる市場参加者に与えるインパクトの程度は大きく異なる。下表は各改革が6つの主要参加者タイプに与える影響評価をまとめたものだ。

| 改革項目 | BESS事業者 | 再エネ事業者 | 小売/供給事業者 | 大口需要家 | EVアグリゲーター | 従来型電力会社 |

|---|---|---|---|---|---|---|

| API移行(4月) | 高 | 中 | 重大 | 低 | 中 | 重大 |

| インバランス上限拡大(4月) | 低 | 重大 | 高 | 中 | 低 | 中 |

| 5ゾーン透明化(10月) | 重大 | 高 | 高 | 中 | 高 | 中 |

| 手数料改定 | 中 | 低 | 高 | 低 | 中 | 高 |

| 低圧参加開放 | 高 | 低 | 中 | 中 | 重大 | 低 |

低圧参加開放:FY2026の隠れた機会

3大主要改革に加え、FY2026には低圧(100V/200V)需要側リソースの時間前市場参加試行計画も推進される。現在の時間前市場の最小取引単位は0.1MW(100kW)であり、住宅用太陽光や小型商業BESSなどの低圧リソースには参入障壁が高い。試行計画ではアグリゲーター機能を導入し、複数の低圧リソースをパッケージ化して参加させることで、最小アグリゲーション規模を1MWまで引き下げる予定だ。

この仕組みはEVアグリゲーター(V2Gサービス事業者)にとって特に重要だ。日本のEV保有台数はFY2025に150万台を突破しており、10%のEVがV2Gアグリゲーションに参加すれば、理論上約750MWの調整可能容量を提供できる。これは中規模ガス火力発電所1基分に相当する。低圧参加開放によりこの潜在容量が時間前市場に参入し、EV所有者に追加収益をもたらすと同時に、電力系統に分散型周波数調整リソースを提供することになる。

結論:FY2026は時間前市場の「元年」

FY2026の3大改革は日本の時間前市場の競争環境を根本的に変える。自動取引システムを構築し、API統合能力を持つBESS事業者にとって、これは先行者優位の窓口だ。市場流動性がまだ十分に向上しておらず、価格差が依然として顕著な移行期において、体系的な裁定戦略は相当な超過収益をもたらし得る。

しかし改革は新たなリスクももたらす。インバランス上限拡大はポジション管理ミスのコストを高め、5ゾーン透明化は価格効率を高める一方で裁定機会の消滅速度も加速させる。市場参加者は「先行者優位の確保」と「テールリスクの制御」のバランスを見つける必要があり、それこそがFY2026時間前市場競争の核心命題となる。

Japan's FY2026 Intraday Market Overhaul: Transparency, 5-Zone Structure, and New BESS Arbitrage Strategies

Background: Why FY2026 Is the Inflection Point for Japan's Intraday Market

Japan's intraday market (時間前市場) has played a supplementary role since its launch in 2005—trading volumes hovering at just 5–8% of the spot market, thin liquidity, and opaque price spreads. FY2026 will disrupt this status quo with three simultaneous reforms: full JEPX API migration (April), imbalance price cap expansion (April), and 5-zone bid transparency (October). The compounding effect of these three changes will transform the intraday market from an "emergency dispatch tool" into an "active arbitrage arena."

The growth trajectory is already unmistakable. According to JEPX's FY2024 Annual Business Report, annual intraday trading volume grew from 5.2 TWh in FY2021 to 8.9 TWh in FY2024, a compound annual growth rate (CAGR) of 19.7%—compared to just 3–4% CAGR for the spot market over the same period. This divergence reflects the structural demand created by increasing renewable energy penetration and the resulting amplification of intraday supply-demand volatility.

The Three Reforms in Detail

Reform 1: Full JEPX API Migration (April 2026)

JEPX will complete the migration of its trading system API in April 2026, transitioning from legacy FTP batch downloads to RESTful API real-time streaming. While this appears technical, it has profound implications for competitive dynamics. The new API provides millisecond-level order book updates, enabling participants with automated trading systems—BESS operators and power traders—to adjust intraday market bidding strategies within minutes of spot market results being published.

For smaller retailers and renewable generators without automated systems, the API migration means widening information asymmetry. Under the legacy FTP model, the speed advantage of large players over smaller ones was limited. In the new API environment, system integration capability will directly determine the efficiency of arbitrage window capture.

Reform 2: Imbalance Price Cap Expansion (April 2026)

Under the current framework, imbalance price calculations include a buffer mechanism that partially absorbs extreme price events. From April 2026, the cap will expand to ±100% of the spot average price (i.e., up to twice the spot average), aligning with imbalance pricing mechanisms in major European power markets.

The core logic of this reform is to "strengthen imbalance penalties," compelling market participants to more actively use the intraday market for position balancing rather than relying on the system operator's adjustment capacity. For BESS operators, this creates a two-way opportunity: higher imbalance risk incentivizes renewable generators to purchase more intraday market power, improving liquidity; however, BESS operators holding imbalance positions will also face amplified losses.

Reform 3: 5-Zone Bid Transparency (October 2026)

The current intraday market uses a national unified bidding system with opaque regional price differentials. From October 2026, JEPX will introduce a 5-zone structure (Zone 1: Hokkaido, Zone 2: Tohoku & Tokyo, Zone 3: Chubu, Hokuriku & Kansai, Zone 4: Chugoku & Shikoku, Zone 5: Kyushu), with each zone's bid volumes and clearing prices published independently.

The 5-zone structure will make interconnection congestion price signals far more transparent. In Kyushu, for example, when solar output surges, the Kyushu→Chugoku interconnection frequently reaches full capacity, pushing Kyushu spot prices below the national average. Under the new system, Zone 5 (Kyushu) intraday prices will independently reflect this congestion premium, providing a more precise pricing foundation for cross-regional arbitrage.

Spot-Intraday Price Spread: Quantifying the Arbitrage Opportunity

The core arbitrage logic of the intraday market is capturing the spread between the spot settlement price and the intraday clearing price. According to METI's FY2024 Monitoring Report, the national average spot-intraday spread is approximately ¥0.8–1.5/kWh, but the distribution across regions and time periods is highly uneven.

By time period, the morning peak (07:00–09:00) and evening peak (17:00–21:00) show the most significant spreads, averaging ¥1.2–2.0/kWh. This is directly linked to intraday solar output variability: heavy solar output around noon depresses spot prices, while the rapid spot price recovery after solar withdrawal in the evening peak is anticipated by the intraday market, creating a capturable arbitrage window.

By region, Kyushu (Zone 5) shows the largest spread, averaging ¥1.8/kWh in FY2024—far exceeding Tokyo (Zone 2) at ¥0.6/kWh. This gap stems from Kyushu's 38% renewable energy ratio and limited interconnection capacity, which amplifies intraday supply-demand volatility.

BESS Arbitrage Strategy Framework

For BESS operators, the FY2026 reforms provide a structural arbitrage opportunity: charge during low spot price periods (typically midday high-solar-output periods) and discharge into the intraday market during high-price periods (around the evening peak). The viability of this "spot charge → intraday discharge" strategy depends on three critical conditions.

First, the charge-discharge price spread must cover BESS round-trip efficiency losses (typically 15–20%) and system usage fees. For a typical BESS system (85% round-trip efficiency), if the spot average is ¥10/kWh and the intraday average is ¥12.5/kWh, the arbitrage profit per kWh is ¥12.5 × 0.85 − ¥10 = ¥0.625/kWh. After deducting system usage fees (approximately ¥0.3/kWh), the net profit is approximately ¥0.3/kWh.

Second, API integration capability determines arbitrage window capture efficiency. After the April 2026 API migration, BESS operators with automated bidding systems can complete intraday market bid adjustments within 5–10 minutes of spot results being published, while operators relying on manual operations may miss the optimal spread windows.

Third, regional selection is critical. After the 5-zone system launches, Kyushu (Zone 5) and Chugoku (Zone 4) intraday markets will exhibit the largest regional price differentials, making them priority deployment regions for BESS arbitrage.

Differentiated Impact by Participant Type

The three reforms have markedly different impacts on different market participants. The table below summarizes the impact assessment for six major participant types.

| Reform | BESS Operators | Renewable Generators | Retailers/Suppliers | Large Consumers | EV Aggregators | Traditional Utilities |

|---|---|---|---|---|---|---|

| API Migration (Apr) | High | Medium | Critical | Low | Medium | Critical |

| Imbalance Cap Expansion (Apr) | Low | Critical | High | Medium | Low | Medium |

| 5-Zone Transparency (Oct) | Critical | High | High | Medium | High | Medium |

| Fee Revision | Medium | Low | High | Low | Medium | High |

| Low-Voltage Participation | High | Low | Medium | Medium | Critical | Low |

Low-Voltage Participation: The Hidden Opportunity in FY2026

Beyond the three major reforms, FY2026 will also advance a pilot program for low-voltage (100V/200V) demand-side resources to participate in the intraday market. The current minimum trading unit of 0.1 MW (100 kW) creates a high barrier for residential solar, small commercial BESS, and similar low-voltage resources. The pilot program will introduce an aggregator mechanism allowing multiple low-voltage resources to participate as a package, with the minimum aggregation size expected to drop to 1 MW.

This mechanism is particularly significant for EV aggregators (V2G service providers). Japan's EV fleet surpassed 1.5 million units in FY2025, and if 10% of EVs participate in V2G aggregation, they could theoretically provide approximately 750 MW of dispatchable capacity—equivalent to a mid-sized gas-fired power plant. Low-voltage participation will channel this latent capacity into the intraday market, creating additional revenue for EV owners while providing distributed frequency regulation resources to the grid.

Conclusion: FY2026 as the Intraday Market's "Year Zero"

The three FY2026 reforms will fundamentally reshape the competitive landscape of Japan's intraday market. For BESS operators with established automated trading systems and API integration capabilities, this represents a rare first-mover advantage window: during the transition period when market liquidity has not yet fully improved and spreads remain significant, systematic arbitrage strategies can generate substantial excess returns.

However, the reforms also introduce new risks. Imbalance cap expansion raises the cost of position management errors; while 5-zone transparency improves pricing efficiency, it also accelerates the erosion of arbitrage opportunities. Market participants must find the balance between "capturing first-mover advantage" and "controlling tail risk"—and that is precisely the central challenge of FY2026 intraday market competition.