TOCOM Chubu Futures Liquidity Growth Path: From Early Discovery to Institutional Participation

1. Historical Context of the Chubu Futures Launch: From Two-Area to Three-Area Coverage

On April 13, 2026, the Tokyo Commodity Exchange (TOCOM) officially listed Chubu Area Electricity Futures (monthly and fiscal-year contracts), marking Japan's electricity futures market's transition from "two-area" (East and West) to "three-area coverage." The timing was not coincidental — the sharp widening of Chubu area APD (+8–10 yen/kWh) triggered by the JERA PPA termination provided the strongest market demand signal for Chubu futures.

Against this backdrop, TOCOM's total electricity futures trading volume for FY2025 reached approximately 4,547 GWh, up about 2.2x year-on-year, breaking the previous record. East Area Baseload Electricity Futures grew approximately 1.3x year-on-year, West Area Baseload Electricity Futures grew approximately 2.3x, and fiscal-year contracts introduced in May 2025 recorded approximately 771 GWh for the full year. This growth trajectory provides an important reference framework for analyzing Chubu futures liquidity development.

2. Current Liquidity Status: Characteristics and Challenges of the Early Discovery Phase

2.1 Market Structure in the Early Discovery Phase

The market structure of Chubu futures in the early listing period (April–September 2026) exhibits three typical characteristics. First, highly concentrated participation: primarily composed of major Chubu area retailers (Chubu Electric Power Miraiz, JERA Cross) and select trading houses, with financial institutions and international energy traders yet to enter in significant numbers. Second, high Basis uncertainty: the Basis between Chubu futures and JEPX Chubu area spot prices has not yet formed stable historical patterns, resulting in lower hedging efficiency compared to Tokyo futures. Third, constrained trading volume: monthly trading volume is estimated at 50–100 GWh, far below the liquidity depth of East Area futures.

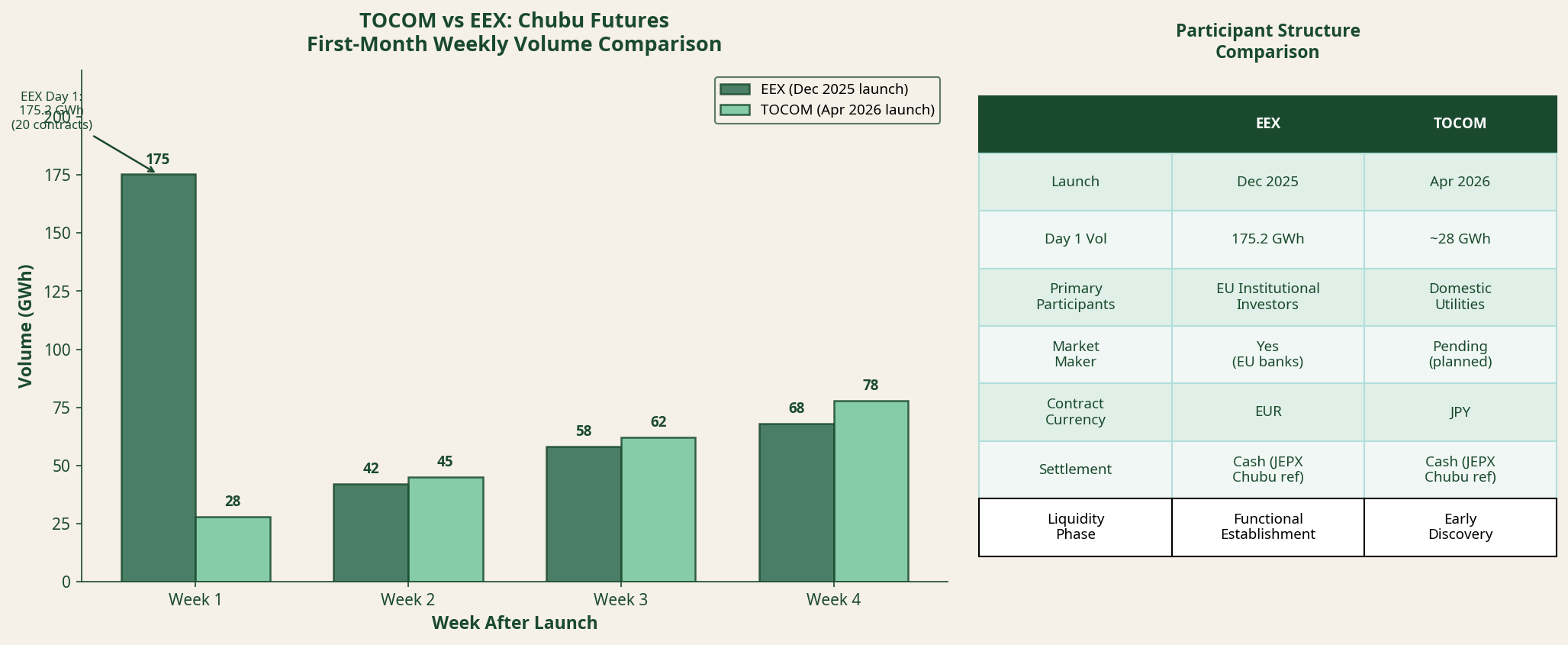

EEX (European Energy Exchange) pre-listed Chubu area futures on December 8, 2025, with 20 contracts (175,200 MWh) traded on the first day. EEX's early listing indicates that some European institutional investors have already begun paying attention to Chubu area electricity price risk, providing a potential source of international liquidity for TOCOM Chubu futures.

2.2 Core Barriers to Liquidity Formation

According to METI's Electricity Futures Activation Study Group, electricity futures liquidity formation faces three core barriers: insufficient participation by diverse players (especially financial institutions), insufficient trading volume on both buy and sell sides by electricity businesses, and insufficient agile service development by commodity exchanges. The challenges facing Chubu futures in the early listing period represent a concentrated manifestation of these three barriers for a new area product.

Table 1: Chubu Futures vs. Tokyo Futures Liquidity Comparison (April 2026)

Indicator

Tokyo Futures (Mature)

Chubu Futures (Early Discovery)

Monthly Trading Volume (est.)

300–500 GWh

50–100 GWh

Key Participants

Utilities + Financial Institutions + International

Miraiz + JERA + Trading Houses

Bid-Ask Spread

¥0.3–0.5/kWh

¥1.0–2.0/kWh (estimated)

Fiscal-Year Contract Share

~17% (771/4,547 GWh)

Monthly contracts dominant initially

Fee Discount

~50% discount (through Mar 2027)

~50% discount (through Mar 2027)

Basis Historical Pattern

Established stable patterns

Not yet formed (early listing)

Figure 2: TOCOM vs EEX Chubu futures weekly volume comparison (GWh) in the first month after launch, alongside participant structure comparison. EEX recorded a 175.2 GWh spike in Week 1 driven by European institutional investors; TOCOM shows lower initial volume dominated by domestic utilities but with a stable growth trend.

3. Three-Stage Liquidity Growth Path

3.1 Stage 1: Early Discovery Phase (April–September 2026)

The core task of the early discovery phase is building a Basis historical database. Following the JERA PPA termination, the Basis between Chubu futures and JEPX Chubu area spot prices exhibits high uncertainty. As APD data accumulates, market participants will gradually develop statistical understanding of Chubu Basis, and hedging efficiency will improve accordingly. The primary participants in this phase are businesses with direct electricity procurement needs in the Chubu area, who have the strongest hedging motivation and the highest tolerance for Basis uncertainty.

TOCOM's most critical measure in this phase is strengthening the market maker mechanism. According to TOCOM's market update materials published in October 2025, the market maker mechanism has played an important role in narrowing spreads in East and West Area futures, with regular condition reviews ensuring more orders are quoted at tighter spreads. Transplanting this mechanism to Chubu futures is the most important institutional safeguard for liquidity formation in the early discovery phase.

The hallmark of the functional establishment phase is financial institutions (securities firms, trading house financial divisions) beginning systematic participation in Chubu futures. Three trigger conditions exist for this phase: first, Chubu Basis historical data accumulates to six months or more, with statistical patterns initially established; second, progress on the Hamaoka Nuclear Power Plant restart review becomes clear, with the outlook for APD's structural transformation clarifying; and third, the deadline effect of the fee discount campaign (through March 2027) accelerates entry decisions by potential participants.

In this phase, monthly trading volume is expected to grow from 50–100 GWh to 200–500 GWh, Bid-Ask spreads narrow to ¥0.5–1.0/kWh, and fiscal-year contract share begins to rise. enechain's launch of Chubu area electricity forward curve provision in December 2025 provides market participants with important pricing references, contributing to the acceleration of liquidity formation in the functional establishment phase.

The core characteristic of the institutional participation phase is the activation of cross-area arbitrage trading. When all three of Tokyo, Chubu, and Kansai area futures have sufficient liquidity depth, Basis differences between areas will become arbitrage targets for institutional investors. Specifically, Tokyo futures long / Chubu futures short Basis arbitrage (APD arbitrage), and Chubu futures vs. Kansai futures Basis arbitrage, will attract international funds and specialist energy traders.

The most critical trigger condition for the institutional participation phase is the realization of the Hamaoka Nuclear Power Plant restart. After restart, Chubu area APD is expected to narrow from +8–10 yen/kWh to +2–4 yen/kWh, and the structural transformation of APD will generate large hedge re-adjustment demand, injecting new liquidity into the market.

4. Concrete Recommendations for Liquidity Enhancement

4.1 Market Maker Mechanism Optimization

The design of Chubu futures' market maker mechanism should draw fully on the experience of East and West Area futures while optimizing for Chubu area's specific characteristics. During the early discovery phase (April–September 2026), adopting "wide spread, high reward" market maker conditions is recommended to attract businesses with Chubu area electricity procurement experience as market makers. During the functional establishment phase (October 2026–March 2027), spread requirements should be progressively tightened to introduce financial institution market makers. During the institutional participation phase (April 2027 onwards), transitioning to a "competitive market maker mechanism" using market competition to maintain liquidity is recommended.

4.2 Cross-Area Arbitrage Strategies

For major businesses with multi-area electricity procurement capabilities (JERA, Marubeni, Sumitomo Corporation, etc.), cross-area arbitrage strategies offer opportunities to capture excess returns during the early liquidity formation period. The core strategy is "Tokyo futures long / Chubu futures short" Basis arbitrage: when Chubu APD exceeds its historical average, short Chubu futures while going long Tokyo futures, betting on APD narrowing. This strategy has the highest risk-adjusted return potential during the functional establishment phase, after progress on the Hamaoka restart review becomes clear.

Note that the effectiveness of cross-area arbitrage strategies depends on Chubu futures having sufficient liquidity depth. During the early discovery phase, large arbitrage positions may face slippage risk from insufficient liquidity; it is recommended to keep single arbitrage positions below 10 GWh and set strict stop-loss conditions.

4.3 Strategic Use of Fiscal-Year Contracts

Fiscal-year contracts are an important catalyst for Chubu futures liquidity growth. For major Chubu area retailers, it is recommended to actively utilize fiscal-year contracts during the functional establishment phase (October 2026–March 2027), building foundational hedge positions in the early listing of FY2027 fiscal-year contracts, and using a "fiscal-year + monthly" combination strategy to cover price risk across different time horizons. East Area futures fiscal-year contracts reached approximately 771 GWh for full-year 2025 (approximately 17% of total), providing a reference target for Chubu futures fiscal-year contract growth.

Liquidity Growth Trigger Events Timeline

April 2026TOCOM Chubu Futures LaunchEarly discovery phase begins. Market maker program (wide spread, high incentive) launches to attract participants with Chubu area procurement experience. JERA PPA termination triggers APD shock period; hedging demand surges.Stage 1 Start

July 2026 (Projected)APD Volatility Decline / Market Equilibrium ReconstructionChubu area APD retreats from shock-period peak (+8–10 ¥/kWh) toward new equilibrium band (+3–5 ¥/kWh). Basis patterns begin forming, improving predictability for financial institution entry.Stage 1 Milestone

October 2026Functional Establishment Phase / FY2027 Annual Contracts ListedMarket maker spread requirements tightened; financial institution market makers introduced. FY2027 annual contracts listed; major players begin building foundational hedge positions. Monthly volume target: 200–300 GWh.Stage 2 Start

January 2027 (Projected)NRA Hamaoka Mid-Term ReviewNRA publishes interim suitability review report for Hamaoka Unit 2. Positive progress would sharply raise market expectations for FY2027 restart, triggering structural Basis convergence expectations and prompting institutional investors to position early.Stage 2 Key Trigger

March 2027TOCOM Market Maker Program ReformTOCOM completes first evaluation of Chubu futures market maker program and adjusts incentive structure based on liquidity growth. Transition to competitive market maker regime.Stage 2 Milestone

April 2027Institutional Participation Phase BeginsFinancial institutions (banks, insurers) formally enter Chubu futures market. Cross-area arbitrage strategies activate. Monthly volume target exceeds 455 GWh (10% of East Area), reaching functional establishment benchmark.Stage 3 Start

FY2027 (Projected)Hamaoka Unit 2 Restart (Conditional)If NRA review proceeds smoothly, Hamaoka Unit 2 (1,380 MW) restart would structurally reduce Chubu APD (+8–10 → +2–4 ¥/kWh), saving TEPCO EP ¥0.6–0.8/kWh in marginal procurement costs. Chubu futures Basis enters new stable equilibrium; liquidity deepening accelerates.Stage 3 Structural Inflection

Chubu futures liquidity growth depends not only on market mechanism design but also heavily on the evolution of three external conditions.

First, the APD stabilization process following the JERA PPA termination. APD's high volatility is a double-edged sword for Chubu futures liquidity formation: on one hand, high APD strengthens hedging demand and provides a foundation for liquidity; on the other hand, APD uncertainty makes Basis difficult to predict, increasing uncertainty in hedging efficiency. The decline in APD volatility accompanying market equilibrium reconstruction (expected in H2 2026) will help Basis patterns form, thereby attracting more financial institution participation.

Second, progress on the Hamaoka Nuclear Power Plant restart review. As noted above, the Hamaoka restart is the most important structural inflection point for the Chubu area electricity market. The transparency of NRA review progress will directly affect market participants' expectation formation regarding Chubu futures' long-term Basis, in turn affecting the timing of the institutional participation phase's arrival.

Third, regulatory relaxation for financial institution participation. METI's Electricity Futures Activation Study Group report notes that expanding financial institution participation is essential for improving electricity futures market liquidity. Currently, Japanese financial institutions' participation in the electricity futures market is subject to certain regulatory constraints, and relaxation of these regulations will be an important institutional catalyst for accelerating the arrival of the institutional participation phase.

6. Conclusion: Liquidity Growth Timeline and Key Milestones

TOCOM Chubu futures' liquidity growth follows a traceable three-stage process. The early discovery phase (April–September 2026) focuses on Basis data accumulation and market maker mechanism establishment; the functional establishment phase (October 2026–March 2027) is marked by financial institution participation and fiscal-year contract activation; and the institutional participation phase (April 2027 onwards) is characterized by cross-area arbitrage activation and structural liquidity injection from the Hamaoka restart.

For electricity businesses, actively participating in Chubu futures during the early discovery phase is not only a practical fulfillment of hedging needs but also a strategic opportunity to accumulate market influence during the liquidity formation process. Early movers will gain informational advantages during the formation of Basis patterns, and this advantage will translate into sustainable competitive advantage during the institutional participation phase.