2026年3月東京首次再生能源出力制御:數據解析、核電衝擊與政策矛盾

2026年3月1日(週日)上午11時,東京電力輸配電公司(TEPCO Power Grid)向其服務區域內的再生能源業者發出史上首次出力制御指令,要求在11:00至16:00期間限制發電出力。這一事件標誌著日本全國10個輸配電區域全部進入「棄電時代」,具有深遠的結構性意義。

一、事件數據:官方速報解析

根據東京電力輸配電公司於3月1日發布的官方速報,當日需給狀況如下:

| 項目 | 數值(MW) |

|---|---|

| 區域需求 | 25,430 |

| 揚水運轉(需要創出) | 6,170 |

| 域外送電 | 0(無可用跨區輸電容量) |

| 小計(需要側合計) | 31,600 |

| 供給力(制御前) | 33,440 |

| 供需缺口 | +1,840 |

| 再生能源出力制御量(TEPCO速報峰值) | 1,840 MW |

出力制御的具體構成為:太陽光與風力發電 1,810 MW、生質能發電 40 MW。最大餘剩電力發生於12:00至12:30,正值春季晴天的日照高峰。

[數據說明:TEPCO vs OCCTO]

TEPCO速報公布的「1,840 MW」為11:00–16:00整個制御時段的峰值(最大瞬間制御量,發生於12:00–12:30時段)。OCCTO再生能源出力抑制實績公表系統則記錄11:00–13:00時段的抑制出力合計最大值為1,149.774 MW,兩者統計口徑不同,並不矛盾。

根據OCCTO出力抑制実績公表系統,2026年3月東京電力區域共發生以下5次出力制御事件:

| 日期 | 制御時間帶 | 抑制出力合計最大值(MW) | 備注 |

|---|---|---|---|

| 2026/03/01 | 11:00–13:00 | 1,149.774 | 東京首次出力制御 |

| 2026/03/07 | 00:00–00:00 | 0.000 | 制御指令發出但實際削減量為零 |

| 2026/03/08 | 08:00–16:00 | 2,207.476 | — |

| 2026/03/21 | 08:00–16:00 | 1,783.202 | 無核電機組在線 |

| 2026/03/28 | 08:00–16:00 | 2,322.234 | — |

| 2026/03/29 | 08:00–16:00 | 2,553.222 | 月內最高峰值 |

值得注意的是,3月8日至29日的制御時間帶均擴大為08:00–16:00(8小時),遠長於首次制御的2小時,且峰值制御量持續攀升,最高達2,553 MW。3月21日的事件尤為值得關注:當天沒有核電機組在線,純粹由太陽能發電的高出力壓垮了系統靈活性,證明出力制御已不再依賴核電這一觸發因素,而是成為結構性常態。

二、歷史背景:全國棄電趨勢加速

在2026年3月之前,東京電力區域是日本唯一未發生過經濟性出力制御的大型電網。各區域首次出力制御時間線如下:

| 區域 | 首次出力制御年度 |

|---|---|

| 九州 | FY2018(最早) |

| 北海道、東北、中國、關西、四國、沖繩 | FY2022 |

| 中部、北陸 | FY2023 |

| 東京 | 2026年3月1日 |

從全國數據來看,棄電規模正在加速擴大:

- 2025年上半年(4–9月):全國9個區域棄電量合計 1.74 TWh,創下任何六個月期間的歷史新高

- 2025年1–8月:累計棄電量 1.77 TWh,較前年同期(1.28 TWh)增長 38.2%,占再生能源發電量的 2.3%

- 各區域棄電率(2025年前5個月):九州 7.6%、東北 5.8%(前年同期僅2.1%,大幅惡化)

三、核電重啟的排擠效應:柏崎刈羽6號機

2026年2月9日,東京電力柏崎刈羽原子力発電所6號機(ABWR,額定出力1,356 MW)再稼動,這是TEPCO自2011年福島事故後首座重啟的反應爐。6號機自福島事故後一直未商轉,近年雖通過部分新規制要求並完成安全對策,但仍需歷經地方同意等程序,方才推進重啟。

| 日期 | 事件 |

|---|---|

| 2026年1月21日 | 原子爐起動(首次嘗試),因警報觸發於1月23日停機 |

| 2026年2月9日 | 再稼動(原子爐重新達到臨界) |

| 2026年2月16日 | 連接電網,開始調整運轉(試驗性送電) |

| 2026年3月3日 | 達到100%滿載出力(1,356 MW),仍處調整運轉階段 |

| 2026年4月16日(預定) | 正式商業運轉(営業運転)開始,因設備不具合較原定延期約7週 |

注意:3月1日出力制御發生時,6號機雖已達滿載出力,但尚未完成正式商業運轉(営業運転預定4月16日),仍處調整運轉階段。此外,7號機(同為1,356 MW)的重啟計畫已延期至2029至2030年。

根據美國能源資訊署(EIA)估算,6號機全年發電量約 9.5 TWh,可替代約 130萬頓LNG 進口。然而,這1,356 MW的穩定基載電力,在春季低需求時段直接壓縮了再生能源的入網空間。

日本優先給電規則規定,當電力供給過剩時,應依序採取:①抑制火力發電→②揚水運轉→③跨區送電→④再生能源出力制御→⑤最後才限制核電、水力、地熱。核電在此規則中受到保護,成為再生能源棄電的結構性推手。

四、電網靈活性的三重瓶頸

能源經濟與財務分析研究所(IEEFA)日本能源金融專家宮本道代指出,系統靈活性未能跟上再生能源整合的步伐,具體表現在三個層面:

(1)火力發電降載能力有限:火力發電廠通常只能將出力降至最大值的30%至50%,無法完全退出市場。在東京電力區域,當核電滿載且太陽能高出力時,火力已無進一步降載的空間。

(2)抽蓄水力已達飽和:3月1日的數據顯示,揚水運轉已達6,170 MW,幾乎是需求側調節的極限。電池儲能系統(BESS)規模仍然太小,無法吸收龐大的餘剩電力。

(3)跨區輸電容量瓶頸:「域外送電:0」直接說明問題。Rystad Energy東京分析師指出:「主要問題是高再生能源區域的輸電容量不足,太陽能建設速度超過了本地需求和輸出能力。」

五、政策矛盾:再生能源主力化 vs. 原發回歸

日本第7次能源基本計畫設定了至2040年將再生能源比例提升至40%至50%的目標(2024年度實績為23%)。然而,現實中卻面臨深刻的政策矛盾:一方面推動「再生能源主力化」;另一方面為確保能源安全,加速「原發回歸」。

這一趨勢已對投資環境造成實質衝擊。IEEFA報告顯示,在截至2025年3月的財政年度中,共有 52家再生能源開發商退出日本市場,其中包括8家破產。2025年新增風電和太陽能裝置容量增速僅3.3%,為2009年以來最低。

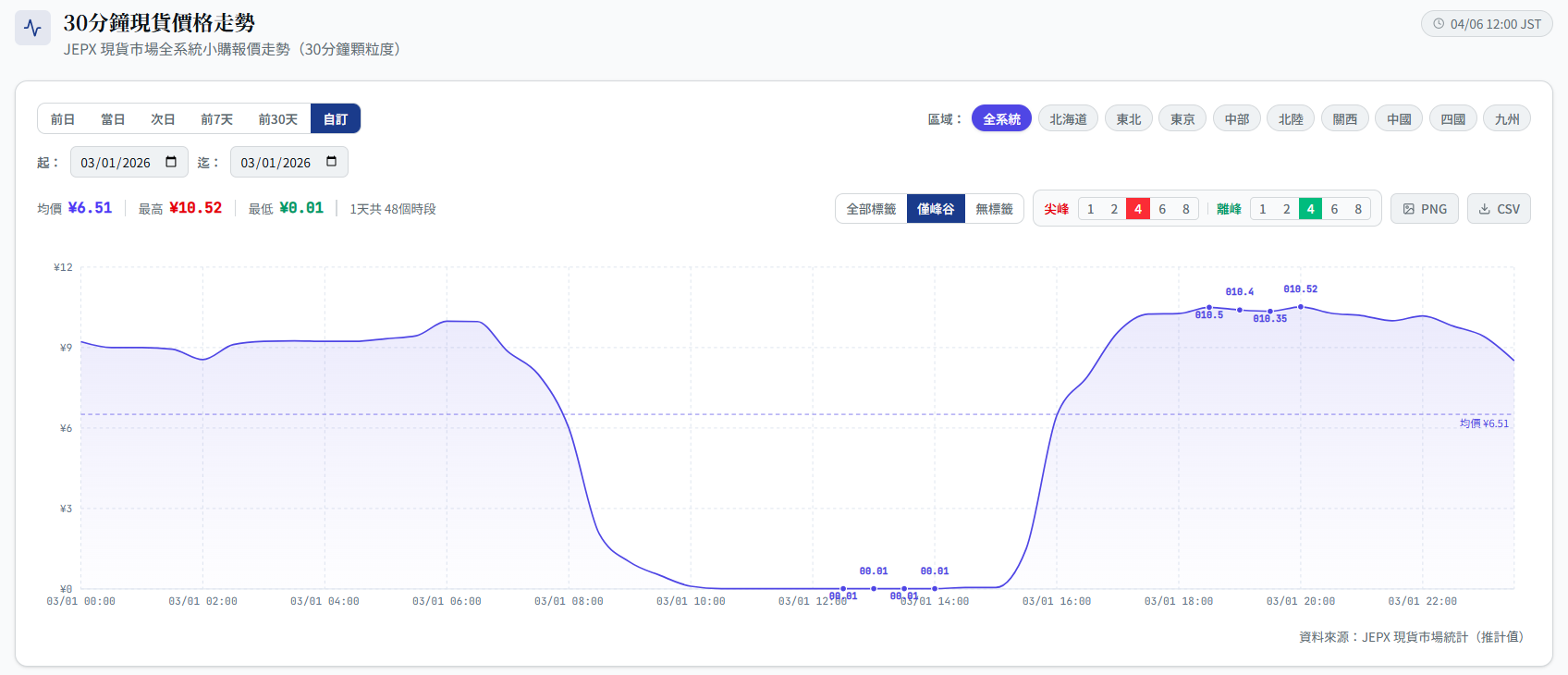

六、BESS 的套利機會:低電價時段的商業邏輯

出力制御的頻繁發生,意外地為電池儲能系統(BESS)創造了顯著的市場套利機會。當出力制御指令發出時,JEPX日前現貨市場的對應時段電價往往跌至接近零(¥0.01/kWh,即市場下限)——再生能源業者寧願以極低價格出售電力,也不願承擔出力制御帶來的發電收入損失。值得注意的是,日本JEPX現貨市場目前設有¥0.01/kWh的電價下限,並不存在歐洲市場常見的負電價機制。

BESS的套利邏輯如下:在出力制御時段(通常08:00–16:00的日照高峰),以接近市場下限(¥0.01–2/kWh)的極低電價從市場低價充電;待傍晚至夜間需求高峰(18:00–22:00)電價回升至¥15–30/kWh時放電,賺取價差。以2,000 MW·h容量的系統用蓄電站為例,單日套利收益可達數千萬日圓。

| 時段 | JEPX現貨電價特徵 | BESS操作 |

|---|---|---|

| 08:00–16:00(制御時段) | 接近市場下限(¥0.01–2/kWh) | 充電(低成本取得電力) |

| 18:00–22:00(夜間需求峰) | ¥15–30/kWh(一般水準) | 放電(高價出售電力) |

| 套利價差 | 每kWh可達¥13–28,年化收益率可觀 | |

【政策依據】 JEPX現貨市場電價下限(¥0.01/kWh)依據《電力廣域的運営推進機関業務規程》及JEPX交易規則第14條(最低申報電價)設定。此下限自2016年電力市場自由化後沿用至今,與德國EPEX SPOT(下限-500 €/MWh)、英國N2EX(下限-9,999 £/MWh)等允許深度負電價的歐洲市場形成鮮明對比。日本是否引入負電價機制,目前仍在METI電力・ガス取引監視等委員会的政策研究議程中。

此外,BESS還可參與需給調整市場(調整力市場),提供一次調整力(瞬時調頻)或三次調整力(ΔkW商品),疊加多重收益來源。日本2025年第二輪長期拍賣已授權1.4 GW BESS容量,東急不動產等企業投資300億日圓建設系統用蓄電站,正是看準了出力制御常態化帶來的套利空間。

從政策角度,出力制御時段的低電價訊號,是市場機制引導儲能投資的自然結果。目前JEPX現貨市場電價下限為¥0.01/kWh,日本尚未引入歐洲式的負電價機制。若未來政策改革允許電價跌破零,將進一步強化BESS的商業誘因,加速儲能部署,從而緩解棄電問題。

七、解決方案與未來展望

| 解決方案 | 現況與進展 |

|---|---|

| 跨區輸電擴建 | 日本正推進北海道至本州、九州至本州的輸電線路擴容,但工程週期長,短期難以緩解 |

| 電池儲能(BESS)擴張與套利 | 2025年第二輪長期拍賣授權1.4 GW BESS容量;出力制御時段低電價為BESS提供充電套利機會,東急不動產等企業投資300億日圓建設系統用蓄電站 |

| 虛擬電廠(VPP)與需求反應 | 東京電力已啟動住宅電池需求反應試驗計畫 |

| 負電價機制改革 | JEPX現貨市場電價下限目前為¥0.01/kWh,日本尚無負電價;若未來引入負電價機制,將強化BESS套利誘因,加速儲能部署 |

| 優先給電規則修訂 | 學界呼籲調整核電在優先給電規則中的地位,但政治阻力較大 |

八、結論

2026年3月東京電力區域首次實施的再生能源出力制御,是日本能源轉型的一個關鍵轉折點。OCCTO官方數據顯示,3月份共發生5次制御事件,峰值從首次的1,149.774 MW快速攀升至月底的2,553.222 MW,揭示了三個核心問題:其一,在缺乏足夠儲能與電網靈活性的情況下,單純增加裝置容量將面臨嚴重的棄電瓶頸;其二,核電重啟與優先給電規則的組合,在結構上不利於再生能源的市場化發展;其三,出力制御的投資抑制效應已開始顯現,威脅日本2040年再生能源目標的實現。

然而,危機中也孕育著機遇。出力制御常態化所帶來的低電價時段(電價跌至¥0.01/kWh市場下限附近),正在為BESS投資創造可量化的套利空間。若日本未來能推進電價下限改革並加速儲能部署,棄電問題或可在市場力量的驅動下逐步緩解。3月21日那次「無核電在線仍發生出力制御」的事件,是最有力的警示:東京棄電問題不是偶發事件,而是系統性挑戰的開始,也是儲能與電網改革的最大催化劑。

2026年3月・東京エリア初の出力制御:データ分析、原発再稼働の影響と政策的矛盾

2026年3月1日(日曜日)午前11時、東京電力パワーグリッド株式会社は、同社サービスエリアで初となる再生可能エネルギーの出力制御を実施した。制御時間は11:00〜16:00の5時間で、最大余剰電力の発生は12:00〜12:30に集中した。これにより、日本全国10の送配電エリアすべてが出力制御を経験したことになる。

1. 公式速報データの解析

東京電力パワーグリッドが3月1日に公表した速報によると、当日の需給状況は以下のとおりである。

| 項目 | 数値(MW) |

|---|---|

| 區域需求 | 25,430 |

| 揚水運転(需要創出) | 6,170 |

| 域外送電 | 0(連系線容量ゼロ) |

| 小計 | 31,600 |

| 供給力(制御前) | 33,440 |

| 需給差 | +1,840 |

| 再エネ出力制御量(TEPCO速報ピーク値) | 1,840 MW |

制御内訳は太陽光・風力発電 1,810 MW、バイオマス発電 40 MW。特筆すべきは「域外送電:0」という数値であり、出力制御実施時点で東京電力エリアから他エリアへの電力融通が一切できなかったことを意味する。

[データ説明:TEPCO速報 vs OCCTO実績]

TEPCO速報の「1,840 MW」は11:00–16:00の制御時間帯全体のピーク値(12:00–12:30コマに発生)。OCCTO再生可能エネルギー出力抑制実績公表システムによると、11:00–13:00時間帯の抑制出力合計最大値は1,149.774 MWであり、両者は統計口径が異なるため矛盾しない。

OCCTO出力抑制実績公表システムによると、2026年3月の東京エリアにおける制御実績は以下のとおりである。

| 日付 | 制御時間帯 | 抑制出力合計最大値(MW) | 備考 |

|---|---|---|---|

| 2026/03/01 | 11:00–13:00 | 1,149.774 | 東京エリア初の出力制御 |

| 2026/03/07 | 00:00–00:00 | 0.000 | 制御指示発出も実際削減量はゼロ |

| 2026/03/08 | 08:00–16:00 | 2,207.476 | — |

| 2026/03/21 | 08:00–16:00 | 1,783.202 | 原子力ゼロ稼働中に発生 |

| 2026/03/28 | 08:00–16:00 | 2,322.234 | — |

| 2026/03/29 | 08:00–16:00 | 2,553.222 | 月内最大値 |

3月8日以降の制御時間帯はすべゆ08:00–16:00(8時間)に拡大され、初回制御の2時間を大きく上回り、ピーク制御量も月内最高2,553 MWまで上昇した。特に3月21日の出力制御は原子力発電機が一切稼働していない状況で発生した。太陽光発電だけでシステムの柔軟性を超えたことを示しており、出力制御が原発再稼働とは独立した構造的問題であることを証明している。

2. 全国の出力制御動向

各エリアの初回出力制御年度は以下のとおりである。

| エリア | 初回出力制御年度 |

|---|---|

| 九州 | FY2018(最初) |

| 北海道・東北・中国・関西・四国・沖縄 | FY2022 |

| 中部・北陸 | FY2023 |

| 東京 | 2026年3月1日 |

- 2025年度上半期(4〜9月):全国9エリア合計 1.74 TWh(上半期として過去最高)

- 2025年度1〜8月累計:1.77 TWh(前年同期比 +38.2%)、再エネ発電量の 2.3%

- 九州エリア(2025年度前5ヶ月):棄電率 7.6%

- 東北エリア(2025年度前5ヶ月):棄電率 5.8%(前年同期2.1%から急増)

3. 柏崎刈羽6号機再稼働の影響

2026年2月9日、東京電力は柏崎刈羽原子力発電所6号機(ABWR、定格出力1,356 MW)を再稼働させた。これはTEPCOが2011年の福島事故以来、初めて稼働させた原子炉である。6号機は福島事故後ずっと商業運転を停止しており、新規制基準への適合や安全対策工事、地元同意などの手続きを経て、ようやく再稼働に至った。

| 日付 | 経緯 |

|---|---|

| 2026年1月21日 | 原子炉起動(初回試み)→ 1月23日に警報発生で停止 |

| 2026年2月9日 | 再稼働(原子炉が臨界に達する) |

| 2026年2月16日 | 発電機接続・調整運転(試験送電)開始 |

| 2026年3月3日 | 電気出力100%(1,356 MW)到達、調整運転継続中 |

| 2026年4月16日(予定) | 営業運転開始(設備不具合により当初予定から約7週間延期) |

注記:3月1日の出力制御発生時点では、6号機は満負荷出力に達していたものの、営業運転(商業運転)はまだ開始されておらず(予定:4月16日)、調整運転の段階にあった。また、7号機(同じく1,356 MW)の再稼働計画は2029〜2030年に延期されている。

米EIAの試算によれば、6号機の年間発電量は約 9.5 TWh、約 130万トンのLNG 輸入を代替できる。しかし、この1,356 MWの安定した基幹電源が、春季の低需要期に再生可能エネルギーの系統接続を圧迫した。

日本の優先給電ルールでは、電力供給過剰時の対応順序を①火力発電抑制→②揚水運転→③域外送電→④再エネ出力制御→⑤水力・原子力・地熱の順と定めており、原子力は事実上保護されている。

4. 系統柔軟性の三重の制約

(1)火力発電の出力調整能力の限界:火力発電所は通常、最大出力の30〜50%までしか出力を下げられない。東京エリアでは、原子力が満負荷稼働し太陽光が高出力の状況下で、火力のさらなる出力抑制余地がなくなっていた。

(2)揚水発電の飽和:3月1日の速報データが示すように、揚水運転はすでに6,170 MWに達しており、需要側調整の限界に近い。電池蓄電システム(BESS)は規模がまだ小さく、大量の余剰電力を吸収できない。

(3)連系線容量のボトルネック:「域外送電:0」という数値が端的に示すように、出力制御当日は他エリアへの送電が一切できなかった。Rystad Energyの東京アナリストは「主な問題は再エネ比率の高いエリアからの送電容量不足だ」と述べている。

5. 政策的矛盾:再エネ主力化と原発回帰の相克

第7次エネルギー基本計画は2040年度の再エネ比率目標を40〜50%(2024年度実績23%)と設定している。しかし、エネルギー安全保障の観点から原発回帰を加速させており、この二重政策が系統容量の制約下で衝突している。

IEEFAの報告によれば、2025年3月期に 52社の再エネ開発事業者が日本市場から撤退(うち8社が倒産)した。2024年の新規風力・太陽光設備容量の増加率はわずか3.3%で、2009年以来最低水準となった。

6. BESSの裁定機会:低電価時間帯の商業ロジック

出力制御の頻発は、電池蓄電システム(BESS)に大きな市場機会をもたらしている。出力制御指示が発出される時間帯には、JEPXスポット市場の電価が市場下限(¥0.01/kWh)付近まで急落することがある。再エネ事業者は出力制御による収益損失を回避するため、極小の電価でも送電を希望する。なお、日本のJEPXスポット市場には現在¥0.01/kWhの電価下限が設けられており、欧州市場のようなマイナス電価制度は存在しない。

BESSの裁定ロジックは以下のとおりである。出力制御時間帯(08:00–16:00)に市場下限付近(¥0.01–2/kWh)の低電価で安く充電し、夕方から夜間の需要ピーク(18:00–22:00)に電価が¥15–30/kWhまで回復した際に放電して差益を獲得する。

| 時間帯 | JEPXスポット電価の特徴 | BESS操作 |

|---|---|---|

| 08:00–16:00(制御時間帯) | 市場下限付近(¥0.01–2/kWh) | 充電(低コストで電力調達) |

| 18:00–22:00(夜間ピーク) | ¥15–30/kWh(通常水準) | 放電(高電価で送電) |

| 裁定差益 | 1kWhあたり¥13–28、年化収益率は十分に見込める | |

【法的根拠】 JEPXスポット市場の電価下限(¥0.01/kWh)は、「電力広域的運営推進機関業務規程」およびJEPX取引規程第14条(最低申告電価)に基づく。この下限は2016年の電力市場完全自由化以降適用されており、ドイツEPEX SPOT(下限-500€/MWh)や英国N2EX(下限-9,999£/MWh)など深度のマイナス電価を許容する欧州市場とは対照的である。日本へのマイナス電価導入については、METI電力・ガス取引監視等委員会の政策検討議题となっている。

さらに、BESSは需給調整市場への参加を通じて一次調整力(瞬時調波)や三次調整力(ΔkW商品)を提供することで、裁定収益に加えて複数の収益源を積み上げることができる。日本で2025年第2回長期入札で認定した1.4 GWのBESSや、東急不動産等が投資する300億円規模の系統用蓄電所は、出力制御の常態化がもたらす裁定機会を見込んでいる。

政策面では、出力制御時間帯の低電価シグナルは市場メカニズムが蓄電投資を誘導する自然な結果である。現在JEPXスポット市場の電価下限は¥0.01/kWhであり、日本にはマイナス電価制度が存在しない。将来的に電価下限の引き下げや撤廃が実現すれば、BESSの商業的誘因がさらに強まり、蓄電展開が加速されることが期待される。

7. 解決策と展望

| 対策 | 現状と進捗 |

|---|---|

| 広域連系線の増強 | 北海道〜本州、九州〜本州間の送電容量拡大を推進中。工期が長く、短期的な緩和は難しい |

| BESS拡大と裁定 | 2025年第2回長期入札で1.4GWを認定。出力制御時間帯の低電価がBESS充電裁定の機会を提供。東急不動産等が300億円規模の系統用蓄電所を建設中 |

| VPP・需要反応 | 東京電力が住宅用電池を活用した需要反応パイロット事業を開始 |

| 電価下限制度の改革 | JEPXスポット市場の電価下限は現在¥0.01/kWhで、日本にはマイナス電価制度がない。将来的な電価下限の引き下げはBESS裁定誘因を強化し、蓄電展開を加速する可能性がある |

| 優先給電ルールの見直し | 学識者から原子力の優先度引き下げを求める声があるが、政治的ハードルは高い |

8. 結論

2026年3月の東京エリア初出力制御は、日本のエネルギー転換における重大な転換点である。OCCTO公式データによると、3月中に5回の制御が発生し、ピーク値は初回の1,149.774 MWから月末の2,553.222 MWへと急上昇した。蓄電・系統柔軟性の不足、原発再稼働と優先給電ルールの組み合わせ、そして投資抑制効果という三つの課題が同時に顕在化した。

しかし、危機の中にも機会がある。出力制御の常態化がもたらす低電価時間帯(電価が¥0.01/kWhの市場下限付近まで急落)は、BESS投資に定量化可能な裁定空間を生み出している。日本が電価下限制度の改革と蓄電展開を同時に進めれば、棄電問題は市場力によって段階的に緩和される可能性がある。3月21日の「原発ゼロでも出力制御」という事実は、東京の棄電問題が偶発的な事象ではなく、構造的な課題の始まりであると同時に、蓄電と電網改革の最大の触媒でもある。

Tokyo's First Renewable Curtailment in March 2026: Data Analysis, Nuclear Impact, and Policy Contradictions

At 11:00 JST on Sunday, March 1, 2026, TEPCO Power Grid issued its first-ever instruction to renewable energy generators to reduce output in the Tokyo service area. The curtailment ran for five hours until 16:00, with peak surplus power occurring between 12:00 and 12:30. With this event, all ten of Japan's transmission system operator (TSO) areas have now experienced economic curtailment.

1. Official Data: What the Numbers Show

TEPCO Power Grid's same-day press release provided the following supply-demand snapshot for March 1:

| Item | Value (MW) |

|---|---|

| Area demand | 25,430 |

| Pumped hydro (demand creation) | 6,170 |

| Inter-regional exports | 0 (zero available capacity) |

| Total demand-side | 31,600 |

| Supply capacity (pre-curtailment) | 33,440 |

| Surplus | +1,840 |

| Renewable curtailment (TEPCO press release peak) | 1,840 MW |

The curtailed output comprised 1,810 MW of solar and wind, and 40 MW of biomass. The figure of zero inter-regional exports is particularly significant: at the moment curtailment was ordered, TEPCO had exhausted all available transmission capacity to neighboring areas.

[Data Note: TEPCO Press Release vs. OCCTO Actual Results]

TEPCO's "1,840 MW" figure is the peak value across the full 11:00–16:00 curtailment window (occurring in the 12:00–12:30 half-hour slot). The OCCTO Renewable Energy Curtailment Actual Results System records the maximum aggregate curtailment output for the 11:00–13:00 window as 1,149.774 MW. These figures use different statistical methodologies and are not contradictory.

According to the OCCTO Renewable Energy Curtailment Actual Results System, Tokyo's curtailment record for March 2026 is as follows:

| Date | Curtailment Window | Max Aggregate Curtailment (MW) | Note |

|---|---|---|---|

| 2026/03/01 | 11:00–13:00 | 1,149.774 | Tokyo's first-ever curtailment |

| 2026/03/07 | 00:00–00:00 | 0.000 | Instruction issued; actual reduction zero |

| 2026/03/08 | 08:00–16:00 | 2,207.476 | — |

| 2026/03/21 | 08:00–16:00 | 1,783.202 | Zero nuclear online |

| 2026/03/28 | 08:00–16:00 | 2,322.234 | — |

| 2026/03/29 | 08:00–16:00 | 2,553.222 | Monthly peak |

From March 8 onward, curtailment windows expanded to eight hours (08:00–16:00), far exceeding the initial two-hour event, with peak curtailment climbing to 2,553 MW by month-end. The March 21 event is particularly notable: it occurred with zero nuclear generation online, demonstrating that solar output alone was sufficient to overwhelm Tokyo's grid flexibility — curtailment has become structurally independent of nuclear dispatch.

2. National Context: Accelerating Curtailment Across Japan

| Area | First Curtailment |

|---|---|

| Kyushu | FY2018 (earliest) |

| Hokkaido, Tohoku, Chugoku, Kansai, Shikoku, Okinawa | FY2022 |

| Chubu, Hokuriku | FY2023 |

| Tokyo | March 1, 2026 |

- H1 FY2025 (April–September 2025): Total curtailment across nine areas reached 1.74 TWh, a record for any six-month period

- April–August 2025: Cumulative curtailment hit 1.77 TWh, up 38.2% year-on-year, representing 2.3% of total renewable generation

- Kyushu (first 5 months of FY2025): Curtailment rate of 7.6%

- Tohoku (first 5 months of FY2025): Curtailment rate of 5.8%, up sharply from 2.1% the prior year

3. The Nuclear Factor: Kashiwazaki-Kariwa Unit 6

On February 9, 2026, TEPCO restarted Unit 6 of the Kashiwazaki-Kariwa Nuclear Power Station — the company's first reactor to resume operations since the 2011 Fukushima accident. Unit 6 had remained offline since the Fukushima disaster; its restart followed years of safety upgrades to meet new regulatory standards and the completion of local consent procedures.

| Date | Event |

|---|---|

| January 21, 2026 | Initial reactor startup attempt; halted January 23 due to alarm |

| February 9, 2026 | Reactor restart (criticality achieved) |

| February 16, 2026 | Grid connection; commissioning (trial power generation) begins |

| March 3, 2026 | Full rated output of 1,356 MW reached; still in commissioning phase |

| April 16, 2026 (planned) | Commercial operation (営業運転) to begin — delayed ~7 weeks from original date due to equipment issues |

Note: At the time of the March 1 curtailment, Unit 6 was operating at full output but had not yet entered commercial operation (scheduled for April 16, 2026) — it remained in the commissioning phase. Unit 7 (also 1,356 MW) has had its restart timeline pushed back to 2029–2030.

The U.S. EIA estimates Unit 6 will generate approximately 9.5 TWh annually, displacing roughly 1.3 million tons of LNG imports. However, this 1,356 MW of inflexible baseload power directly reduced the grid headroom available for renewable generation during low-demand spring weekends.

Japan's priority dispatch rules protect nuclear from curtailment. The sequence for managing surplus power is: (1) reduce thermal → (2) pump hydro → (3) inter-regional exports → (4) curtail renewables → (5) only then reduce nuclear, hydro, and geothermal.

4. Three Structural Constraints on Grid Flexibility

Thermal generation floor constraints: Thermal plants can typically only reduce output to 30–50% of maximum capacity. In the Tokyo area, with nuclear running at full output and solar at peak generation, thermal plants had no further room to reduce.

Pumped hydro saturation: The March 1 data shows pumped hydro already operating at 6,170 MW — near its practical limit. BESS remains too limited in scale to absorb large surpluses. Japan awarded 1.4 GW of BESS in its second long-term auction in 2025, but deployment takes time.

Inter-regional transmission bottlenecks: The zero inter-regional export figure on March 1 tells the story directly. Rystad Energy analyst noted: "The main issue is insufficient grid transfer capacity from high-renewables regions. Photovoltaics build-out outpaced local demand and export capability."

5. Policy Contradiction: Renewable Expansion vs. Nuclear Revival

Japan's 7th Strategic Energy Plan targets a 40–50% renewable share by FY2040, up from 23% in FY2024. But the country simultaneously faces a deepening policy contradiction: promoting renewables as the main power source while accelerating nuclear revival for energy security.

An IEEFA report found that 52 renewable energy developers exited Japan in the fiscal year ended March 2025, including eight bankruptcies. New wind and solar capacity additions grew just 3.3% in 2024, the slowest pace since 2009.

6. The BESS Arbitrage Opportunity: Commercial Logic of Low-Price Curtailment Windows

The growing frequency of curtailment events has created a compelling market opportunity for battery energy storage systems (BESS). When curtailment instructions are issued, JEPX day-ahead spot prices for the corresponding periods often collapse toward the market floor of ¥0.01/kWh — renewable generators prefer to sell at near-floor prices rather than absorb the revenue loss from curtailment instructions. It is important to note that Japan's JEPX spot market currently has a price floor of ¥0.01/kWh and does not have a negative pricing mechanism as seen in European markets.

The BESS arbitrage logic is straightforward: charge cheaply during curtailment windows (typically 08:00–16:00 solar peak hours) when spot prices approach the market floor (¥0.01–2/kWh), then discharge during evening demand peaks (18:00–22:00) when prices recover to ¥15–30/kWh, capturing the spread.

| Time Window | JEPX Spot Price Characteristics | BESS Action |

|---|---|---|

| 08:00–16:00 (curtailment window) | Near market floor (¥0.01–2/kWh) | Charge (acquire power at minimal cost) |

| 18:00–22:00 (evening demand peak) | ¥15–30/kWh (normal levels) | Discharge (sell power at premium) |

| Arbitrage spread | ¥13–28 per kWh; annualized returns are commercially viable for grid-scale assets | |

[Policy Basis] The JEPX spot market price floor of ¥0.01/kWh is established under the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) Business Regulations and JEPX Trading Rules Article 14 (minimum bid price). This floor has been in effect since Japan's full electricity market liberalization in April 2016. It stands in sharp contrast to European markets that permit deep negative pricing — Germany's EPEX SPOT (floor: €-500/MWh), UK's N2EX (floor: £-9,999/MWh), and Nord Pool (floor: €-500/MWh). Whether Japan should introduce a negative pricing mechanism is currently under policy review at METI's Electricity and Gas Market Surveillance Commission.

Beyond price arbitrage, BESS assets can stack revenues by participating in Japan's frequency regulation markets (primary and tertiary balancing products), layering ancillary service income on top of energy arbitrage. Japan's 2025 second long-term capacity auction awarded 1.4 GW of BESS, and Tokyu Fudosan's ¥30 billion grid-scale storage investment is explicitly targeting the arbitrage opportunity created by chronic curtailment.

From a policy perspective, the low-price signal during curtailment windows is precisely the market mechanism that should incentivize storage investment. If Japan were to introduce a genuine negative pricing mechanism (the current JEPX floor is ¥0.01/kWh), BESS commercial incentives would strengthen further, accelerating deployment and gradually reducing curtailment volumes through market forces.

7. Solutions and Outlook

| Solution | Status |

|---|---|

| Inter-regional transmission expansion | Capacity upgrades between Hokkaido–Honshu and Kyushu–Honshu underway; long construction timelines limit near-term impact |

| BESS scale-up and arbitrage | 1.4 GW awarded in 2025 long-term auction; curtailment-window low prices create charging arbitrage opportunity; Tokyu Fudosan investing ¥30 billion in grid-scale storage |

| VPP and demand response | TEPCO launched residential battery demand response pilot |

| Price floor reform | Current JEPX floor is ¥0.01/kWh; Japan has no negative pricing mechanism. Lowering or removing the floor in the future would strengthen BESS arbitrage incentives and accelerate storage deployment |

| Priority dispatch revision | Academic calls to reduce nuclear's protected status face significant political resistance |

8. Conclusion

Tokyo's first renewable curtailment in March 2026 represents a structural inflection point for Japan's energy transition. OCCTO official data shows five curtailment events in March alone, with peak values surging from 1,149.774 MW on the first event to 2,553.222 MW by month-end. Three core problems have crystallized simultaneously: the mismatch between installed renewable capacity and grid flexibility; the structural incompatibility between nuclear priority dispatch and renewable integration; and the investment-chilling effect of curtailment risk.

Yet crisis also breeds opportunity. The low-price curtailment windows created by chronic curtailment — where spot prices collapse to the ¥0.01/kWh market floor — are generating quantifiable arbitrage space for BESS investors. If Japan can simultaneously advance price floor reform and storage deployment, market forces may gradually erode the curtailment problem from within. The March 21 event — curtailment occurring with zero nuclear generation online — is the clearest signal yet: Tokyo's curtailment challenge is not a one-off, but the beginning of a systemic problem and the greatest catalyst yet for storage investment and grid reform.