日本長期脫炭素電源拍賣第三回結果:大間原發首次落標,非鋰電池超越鋰電池

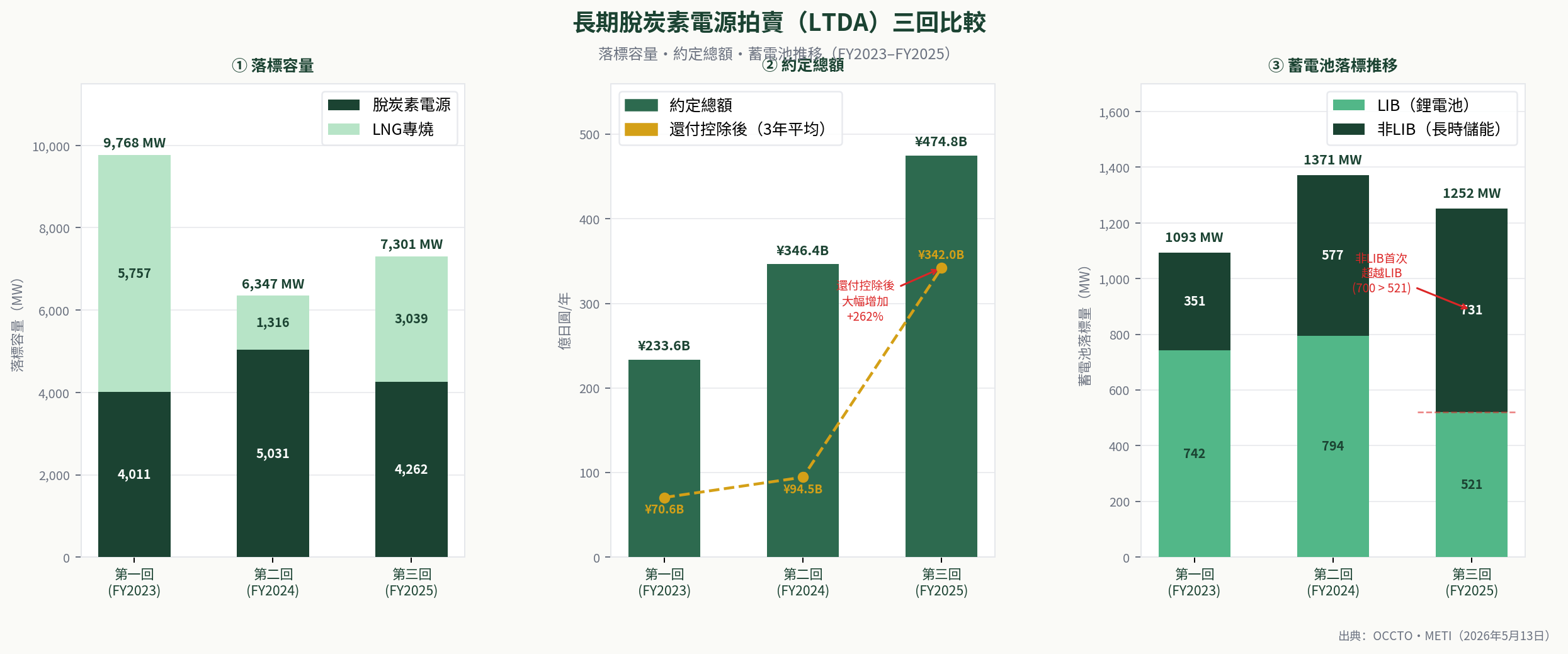

2026年5月13日,電力廣域的運営推進機関(OCCTO)正式公告2025年度長期脫炭素電源拍賣(LTDA)落標結果,標誌著這項自2023年度啟動的制度進入第三個年度。本次落標容量7,300 MW(調整係數適用後),32件案件取得容量確保契約,約定總額達4,748億日圓/年,較第二回(3,464億日圓/年)大幅增加37.1%,創三回最高紀錄。

## 一、制度概要與本回募集條件

LTDA是日本為確保脫炭素電源新規投資而設計的長期容量確保機制,落標電源可取得原則20年的固定費水準容量收入,同時須將其他市場(現貨、需給調整等)收益的約90%還付。

### 還付控除機制說明

**還付控除**(Refund Deduction / Market Revenue Clawback)是LTDA制度的核心財務設計之一。落標事業者在容量確保契約期間,須將其在JEPX現貨市場、需給調整市場(三次調整力等)、容量市場等其他市場所獲收益的約90%返還給OCCTO,匯入容量拠出金財源,最終由電力零售商代收、終端消費者負擔。

制度目的在於防止落標事業者「雙重獲益」——既享有LTDA提供的20年固定費水準容量收入保障,又完整保留其他市場的上行收益。還付控除後的純容量收入計算方式如下:

**純容量收入 = 約定容量收入 − 其他市場收益 × 還付率(約90%)**

還付率依電源種類及契約條件而異,依據METIOCCTO制定的計算規則每年度精算。當JEPX卸售市場價格低迷時,其他市場收益減少,還付金額隨之縮小,落標事業者的純容量收入因而增加。本回(第3回)還付控除後約定總額從第2回的945億日圓大幅增至3,420億日圓,正是因為2024〜2025年度JEPX價格水準持續低於LTDA參照水準,導致還付金額大幅縮小。

本回募集量設定為脫炭素電源500萬kW(5,000 MW)、LNG專燒火力293萬kW(2,930 MW),合計793萬kW(7,930 MW)。

應標總量為1,085.7萬kW(10,857 MW),其中脫炭素電源610.7萬kW(6,107 MW)、LNG專燒475萬kW(4,750 MW)。最終落標量7,300 MW,整體落標率66.6%。值得注意的是,LNG專燒本回落標率僅63.9%,為三回中首次未能100%落標,顯示LNG新設投資意願在高燃料成本環境下出現分化。

## 二、脫炭素電源落標結果詳解

本回脫炭素電源落標量4,262 MW(28件),各電源種落標情況如下:

| 電源種 | 應標量 | 落標量 | 落標率 |

|--------|--------|--------|--------|

| 既設火力改修(脫炭素火力) | 518 MW | 518 MW | 100% |

| 蓄電池(LIB,3–6小時) | 1,526 MW | 552 MW | 36.2% |

| 蓄電池(非LIB,6小時以上) | 1,207 MW | 700 MW | 58.0% |

| 揚水(新設替換) | 187 MW | 187 MW | 100% |

| 既設原子力(安全對策投資) | 559 MW | 559 MW | 100% |

| 原子力(新設:大間) | 1,382 MW | 1,382 MW | 100% |

| 生質能發電 | 102 MW | 102 MW | 100% |

| **脫炭素電源合計** | **6,107 MW** | **4,262 MW** | **69.8%** |

**大間原子力發電所(電源開發)**以1,382 MW取得落標,成為史上首座完成LTDA落標的新設核電廠,也是本回單一案件最大落標容量。大間原發採用全爐心MOX燃料設計,實需給年度預計2029年度以後,其容量確保契約的落標是日本核電新設政策推進的重要里程碑。

**蓄電池領域**出現結構性轉變:非LIB(鋰電池以外,包含液流電池、鐵空氣電池等長時儲能技術)落標量700 MW,首次超越LIB的552 MW。這一趨勢反映出LTDA制度設計中對長時儲能(6小時以上)的差異化支持,以及電池技術多元化的加速進展。

## 三、三回比較:落標量、約定額與蓄電池推移

以下為三回LTDA脫炭素電源落標結果的完整比較:

| 指標 | 第一回(FY2023) | 第二回(FY2024) | 第三回(FY2025) |

|------|----------------|----------------|----------------|

| 入標實施月 | 2024年1月 | 2025年1月 | 2026年1月 |

| 公告月 | 2024年4月 | 2025年5月 | 2026年5月 |

| 募集量(MW) | 4,000 | 5,000 | 5,000 |

| 應標量(MW) | 7,806 | 12,305 | 6,107 |

| 落標量(MW) | 4,011 | 5,031 | 4,262 |

| 落標率 | 51.4% | 40.9% | **69.8%** |

| 約定總額(億日圓/年) | 2,336 | 3,464 | **4,748** |

| 還付控除後(過去3年平均)[^1] | 706億日圓 | 945億日圓 | **3,420億日圓** |

| 蓄電池落標量(MW) | 1,093 | 1,371 | 1,252 |

| 其中非LIB(MW) | — | 410 | **700** |

還付控除後約定總額從第二回的945億日圓大幅增至第三回的3,420億日圓,主因是近年卸売市場價格(JEPX系統均價)持續低於LTDA設定的參考水準,導致還付金額減少,實際容量收入增加。這一趨勢對持有LTDA落標電源的事業者而言是重大利多,但也意味著制度成本(最終由消費者負擔)的上升。

[^1]: **還付控除**(市場收益返還機制):落標事業者須將其他市場(現貨、需給調整等)收益的約90%返還給OCCTO,作為容量拠出金財源。純容量收入 = 約定容量收入 − 其他市場收益 × 還付率(約90%)。詳見[術語對照:還付控除](/glossary#kanpu_kojo)。

應標量方面,第三回6,107 MW較第二回12,305 MW大幅減少50.3%。分析原因,一方面是蓄電池應標量從第二回的約7,000 MW降至本回的2,733 MW,反映出市場對LTDA蓄電池落標條件趨嚴的預期調整;另一方面,部分事業者轉向需給調整市場(三次調整力)或容量市場尋求更短期的收益機會。

*圖:LTDA三回落標容量(脫炭素電源+LNG專燒)、約定總額(含還付控除後淨額)、蓄電池LIB/非LIB推移。出典:OCCTOMETI(2026年5月)*

## 四、LNG專燒落標結果與政策含義

| 指標 | 第一回(FY2023) | 第二回(FY2024) | 第三回(FY2025) |

|------|----------------|----------------|----------------|

| 募集量(MW) | 6,000 | 2,240 | 2,930 |

| 應標量(MW) | 5,757 | 1,316 | 4,750 |

| 落標量(MW) | 5,757 | 1,316 | **3,039** |

| 落標率 | 100% | 100% | **63.9%** |

| 約定總額(億日圓/年) | 1,766 | 456 | 1,444 |

本回LNG專燒應標量4,750 MW遠超募集量2,930 MW,但最終落標量3,039 MW(落標率63.9%),為三回中首次出現不落標情況(1,713 MW未落標)。這一結果顯示LNG新設投資在高燃料成本與碳中和政策壓力下,部分案件的收益性評估已難以通過LTDA的價格審查。

## 五、市場影響與展望

**蓄電池市場**:三回累計蓄電池落標量達3,716 MW(LIB 2,346 MW + 非LIB 1,110 MW + 揚水260 MW),加上容量市場的蓄電池落標量,日本蓄電池容量確保總量已超過5 GW。這批電源陸續進入實需給後,將對JEPX現貨市場的峰谷價差結構產生顯著影響,特別是在太陽光發電大量滲透的午間時段。

**核電新設政策**:大間原發的LTDA落標是日本政府「GX推進法」框架下核電新設政策的重要進展。然而,大間原發的商業運轉時程仍存在不確定性,且北海道地區的電力需求成長預測與輸送線容量限制,將是影響其容量拠出金計算的關鍵變數。

**制度設計的挑戰**:還付控除後約定總額的大幅增加(第三回3,420億日圓/年 vs 第二回945億日圓/年)反映出LTDA制度在卸売市場價格低迷環境下的財政壓力。METI正在研究引入「優先落標」機制,對已取得GX推進法認定的案件給予優先約定,以強化制度的政策引導效果。

**出典**:OCCTO「2025年度長期脱炭素電源拍賣落札結果公表」(2026年5月13日);METI「長期脱炭素電源拍賣相關」(2026年5月13日)

長期脱炭素電源オークション第3回落札結果:大間原発が史上初落札、非LIBが初めてLIBを上回る

2026年5月13日、電力広域的運営推進機関(OCCTO)が2025年度長期脱炭素電源オークション(LTDA)の落札結果を公表した。2023年度に創設されたLTDAは今回で第3回を迎え、落札容量7,300MW(調整係数適用後)・32件が容量確保契約を締結した。約定総額は4,748億円/年と、第2回(3,464億円/年)比37.1%増で3回累計の最高額を更新した。

## Ⅰ.制度概要と本回募集条件

LTDAは脱炭素電源への新規投資を支援するための長期容量確保制度であり、落札電源には原則20年間の固定費水準の容量収入が付与される。一方、他市場(現物、需給調整等)収益の約9割を還付する義務を負う。

### 還付控除の仕組み

**還付控除**(市場収益返納)は、LTDAの中核的な財務設計の一つである。落札事業者は容量確保契約期間中、JEPX現物市場・需給調整市場(三次調整力等)・容量市場等の他市場で得た収益の約90%をOCCTOに返納する義務を負う。返納された資金は容量拠出金の原資として小売電気事業者経由で最終的に需要家が負担する。

制度の趣旨は、落札事業者が「二重取り」——LTDAによる20年間の固定費水準容量収入保証と他市場収益の全額享受——を行うことを防ぐことにある。還付控除後の純容量収入は以下の式で算出される:

**純容量収入 = 約定容量収入 − 他市場収益 × 還付率(約90%)**

還付率は電源種別・契約条件によって異なり、METI・OCCTOが定める算定ルールに基づいて毎年度精算される。JEPX卸売価格が低迷する局面では他市場収益が減少するため還付額も減少し、落札事業者の純容量収入が増加する。第3回(2025年度)において還付控除後約定総額が第2回の945億円から3,420億円へと大幅増加した主因は、2024〜2025年度のJEPX価格水準がLTDA参照水準を下回り、還付額が大幅に縮小したことによる。

本回の募集量は脱炭素電源500万kW(5,000MW)、LNG専焼293万kW(2,930MW)の計793万kW(7,930MW)。

応札総量は1,085.7万kW(10,857MW)で、最終落札量7,300MW、全体落札率66.6%となった。LNG専焼の落札率は63.9%と、3回で初めて100%を下回った。

## Ⅱ.脱炭素電源落札結果

脱炭素電源の落札量は4,262MW(28件)。電源種別の内訳は以下のとおり。

| 電源種 | 応札量 | 落札量 | 落札率 |

|--------|--------|--------|--------|

| 既設火力改修(脱炭素火力) | 518MW | 518MW | 100% |

| 蓄電池(LIB・3〜6時間) | 1,526MW | 552MW | 36.2% |

| 蓄電池(非LIB・6時間〜) | 1,207MW | 700MW | 58.0% |

| 揚水(新設・リプレース) | 187MW | 187MW | 100% |

| 既設原子力(安全対策投資) | 559MW | 559MW | 100% |

| 原子力(新設:大間) | 1,382MW | 1,382MW | 100% |

| バイオマス | 102MW | 102MW | 100% |

| **脱炭素電源合計** | **6,107MW** | **4,262MW** | **69.8%** |

**大間原子力発電所**(電源開発)は1,382MWで落札し、新設原発として史上初めてLTDA容量確保契約を締結した。全炉心MOX燃料を採用する大間原発の実需給年度は2029年度以降の見込みで、GX推進法に基づく原発新設政策の重要な節目となった。

**蓄電池**では、非LIB(液流電池・鉄空気電池等の長時間蓄電技術)の落札量700MWがLIBの552MWを初めて上回った。LTDAの6時間以上の蓄電池に対する差別化支援と、非LIB技術の商業化進展を反映している。

## Ⅲ.3回比較:落札量・約定額・蓄電池推移

| 指標 | 第1回(FY2023) | 第2回(FY2024) | 第3回(FY2025) |

|------|----------------|----------------|----------------|

| 入札実施月 | 2024年1月 | 2025年1月 | 2026年1月 |

| 公表月 | 2024年4月 | 2025年5月 | 2026年5月 |

| 募集量(MW) | 4,000 | 5,000 | 5,000 |

| 応札量(MW) | 7,806 | 12,305 | 6,107 |

| 落札量(MW) | 4,011 | 5,031 | 4,262 |

| 落札率 | 51.4% | 40.9% | **69.8%** |

| 約定総額(億円/年) | 2,336 | 3,464 | **4,748** |

| 還付控除後(過去3年平均)[^1] | 706億円 | 945億円 | **3,420億円** |

| 蓄電池落札量(MW) | 1,093 | 1,371 | 1,252 |

| うち非LIB(MW) | — | 410 | **700** |

還付控除後約定総額が第2回945億円から第3回3,420億円へと大幅増加した主因は、JEPX卸売市場価格がLTDA参照水準を下回る状態が継続し、還付額が減少したことにある。これは落札事業者にとって実質的な容量収入の増加を意味するが、制度コスト(最終的に消費者負担)の上昇でもある。

[^1]: **還付控除**(市場収益還付メカニズム):落札事業者はJEPX現物市場・需給調整市場・容量市場等の他市場で得た収益の約90%をOCCTOに返還し、容量拠出金の財源に充当する義務を負う。純容量収入 = 約定容量収入 − 他市場収益 × 還付率(約90%)。詳細は[用語集:還付控除](/glossary)を参照。

応札量は第2回12,305MWから第3回6,107MWへ50.3%減少した。蓄電池の応札量が約7,000MWから2,733MWへと大幅に減少したことが主因であり、非LIBの技術成熟度要件の厳格化や、需給調整市場(三次調整力)・容量市場への振り向けが背景にある。

*図:LTDA三回の落札容量(脱炭素電源+LNG専焼)、約定総額(還付控除後純額含む)、蓄電池LIB/非LIB推移。出典:OCCTO・METI(2026年5月)*

## Ⅳ.LNG専焼落札結果と政策的含意

| 指標 | 第1回(FY2023) | 第2回(FY2024) | 第3回(FY2025) |

|------|----------------|----------------|----------------|

| 募集量(MW) | 6,000 | 2,240 | 2,930 |

| 応札量(MW) | 5,757 | 1,316 | 4,750 |

| 落札量(MW) | 5,757 | 1,316 | **3,039** |

| 落札率 | 100% | 100% | **63.9%** |

| 約定総額(億円/年) | 1,766 | 456 | 1,444 |

第3回LNG専焼の応札量4,750MWは募集量2,930MWを大幅に上回ったが、1,713MWが不落札となった。3回で初めてLNG専焼が100%落札されなかったことは、燃料費高騰と脱炭素政策の下でLNG新設投資の採算性が分岐していることを示している。

## Ⅴ.市場への影響と今後の展望

**蓄電池市場**:3回累計の蓄電池落札量は3,716MW(LIB 2,346MW+非LIB 1,110MW+揚水260MW)に達した。これらが2027年度以降に実需給に入ると、太陽光大量導入が進む昼間時間帯を中心にJEPX現物市場の価格スプレッド構造に大きな影響を与えることが予想される。

**原発新設政策**:大間原発の落札はGX推進法の原発新設政策の最も具体的な成果であるが、商業運転時期の不確実性や北海道エリアの系統制約、容量拠出金の算定方法が今後の焦点となる。

**制度設計の課題**:還付控除後約定総額の急増(第3回3,420億円/年)は、JEPX価格水準に対するLTDAの財政的感応度の高さを示している。METIはGX推進法認定案件への優先約定制度の導入を検討中であり、制度の政策誘導機能の強化が今後の課題となっている。

*出典:OCCTO「2025年度長期脱炭素電源オークション落札結果公表」(2026年5月13日);METI「長期脱炭素電源オークションについて」(2026年5月13日)*

Japan LTDA 3rd Round Results 2026: Ōma Nuclear Plant Makes History, Non-LIB Batteries Surpass LIB for First Time

On May 13, 2026, the Organisation for Cross-regional Coordination of Transmission Operators (OCCTO) published the results of Japan's FY2025 Long-Term Decarbonisation Auction (LTDA), the third instalment of a mechanism introduced in FY2023 to support new investment in decarbonised power sources. A total of 7,300 MW across 32 projects secured capacity contracts (after adjustment factor application), with annual contract value reaching ¥474.8 billion — a 37.1% increase over the second round's ¥346.4 billion and the highest figure recorded across all three rounds.

## I. Mechanism Overview and Round 3 Procurement Parameters

The LTDA provides winning projects with fixed-cost-level capacity revenue for up to 20 years, in exchange for returning approximately 90% of revenues earned in other markets (spot, ancillary services, etc.) to the system.

### Understanding the Refund Deduction (還付控除) Mechanism

The **refund deduction** (還付控除, also referred to as market revenue clawback) is one of the LTDA's core financial design features. During the capacity contract period, winning bidders are obligated to return approximately 90% of revenues earned in other markets — including the JEPX day-ahead and intraday spot markets, the balancing market (EPRX), and capacity market payments — to OCCTO. These returned funds are pooled into the capacity contribution charge (容量拠出金), collected from electricity retailers and ultimately borne by end consumers.

The rationale is to prevent winning bidders from receiving a "double benefit": a guaranteed 20-year fixed-cost-level capacity payment from LTDA while simultaneously retaining the full upside from other market revenues. Net capacity revenue is calculated as:

**Net Capacity Revenue = Contracted Capacity Revenue − Other Market Revenue × Clawback Rate (~90%)**

The clawback rate varies by resource type and contract terms, and is settled annually according to METI/OCCTO calculation rules. When JEPX wholesale prices are depressed, other-market revenues fall, reducing the clawback amount and increasing the winning bidder's net capacity income. This mechanism directly explains why the post-clawback contracted value in Round 3 surged from ¥94.5 billion (Round 2) to ¥342.0 billion: sustained low JEPX prices in FY2024–2025 significantly reduced clawback amounts, effectively increasing the net value of capacity contracts for winning bidders.

The Round 3 procurement target was set at 5,000 MW for decarbonised sources and 2,930 MW for dedicated LNG thermal, totalling 7,930 MW.

Total bids received reached 10,857 MW (6,107 MW decarbonised + 4,750 MW LNG), and the final contracted volume was 7,300 MW at an overall clearing rate of 66.6%. Notably, the LNG clearing rate fell to 63.9% — the first time in three rounds that LNG bids were not fully awarded — reflecting diverging investment economics for new LNG capacity under elevated fuel cost conditions.

## II. Decarbonised Source Results in Detail

The 4,262 MW of decarbonised sources contracted across 28 projects broke down as follows:

| Source Type | Bid Volume | Contracted | Clearing Rate |

|-------------|-----------|------------|---------------|

| Existing thermal retrofit (decarbonised) | 518 MW | 518 MW | 100% |

| Battery storage — LIB (3–6 hours) | 1,526 MW | 552 MW | 36.2% |

| Battery storage — non-LIB (6+ hours) | 1,207 MW | 700 MW | 58.0% |

| Pumped hydro (new / replacement) | 187 MW | 187 MW | 100% |

| Existing nuclear (safety investment) | 559 MW | 559 MW | 100% |

| Nuclear — new build (Ōma NPP) | 1,382 MW | 1,382 MW | 100% |

| Biomass | 102 MW | 102 MW | 100% |

| **Decarbonised total** | **6,107 MW** | **4,262 MW** | **69.8%** |

**Ōma Nuclear Power Plant** (operated by J-Power / Electric Power Development Co.) secured 1,382 MW — the largest single-project award in Round 3 and the first-ever capacity contract for a greenfield nuclear plant under the LTDA. Ōma is designed to operate on a full mixed-oxide (MOX) fuel core and is expected to enter commercial operation from FY2029 onwards. Its LTDA award represents a landmark milestone in Japan's GX Promotion Act framework for nuclear new-build.

**Battery storage** underwent a structural shift: non-LIB technologies (flow batteries, iron-air batteries, and other long-duration storage) contracted 700 MW, surpassing LIB's 552 MW for the first time. This reflects both the LTDA's differentiated support structure for 6-hour-plus storage and the accelerating commercial readiness of non-LIB technologies.

## III. Three-Round Comparison: Contracted Capacity, Contract Value, and Battery Storage Trends

| Metric | Round 1 (FY2023) | Round 2 (FY2024) | Round 3 (FY2025) |

|--------|-----------------|-----------------|-----------------|

| Auction month | Jan 2024 | Jan 2025 | Jan 2026 |

| Results published | Apr 2024 | May 2025 | May 2026 |

| Procurement target (MW) | 4,000 | 5,000 | 5,000 |

| Total bids (MW) | 7,806 | 12,305 | 6,107 |

| Contracted volume (MW) | 4,011 | 5,031 | 4,262 |

| Clearing rate | 51.4% | 40.9% | **69.8%** |

| Annual contract value (¥B/yr) | 233.6 | 346.4 | **474.8** |

| Net of rebate (3-yr avg, ¥B/yr)[^1] | 70.6 | 94.5 | **342.0** |

| Battery storage contracted (MW) | 1,093 | 1,371 | 1,252 |

| of which non-LIB (MW) | — | 410 | **700** |

The sharp increase in net-of-rebate contract value — from ¥94.5 billion in Round 2 to ¥342.0 billion in Round 3 — is primarily driven by the sustained decline in JEPX spot prices relative to the LTDA reference level, which reduces the rebate amount and increases the effective capacity revenue received by project owners. While this is positive for contracted generators, it implies rising system costs ultimately borne by consumers.

[^1]: **Refund Deduction** (還付控除, market revenue clawback): LTDA winning bidders are obligated to return approximately 90% of revenues earned in other markets (JEPX spot, ancillary services, capacity market, etc.) to OCCTO during the capacity contract period. These funds are pooled into the capacity contribution charge (容量拠出金) collected from electricity retailers and ultimately borne by end consumers. Net capacity revenue = Contracted capacity revenue − Other market revenues × Rebate rate (~90%). See [Glossary: Refund Deduction](/glossary) for details.

Total bids in Round 3 (6,107 MW) fell 50.3% from Round 2 (12,305 MW), largely due to a sharp reduction in battery storage bids (from approximately 7,000 MW in Round 2 to 2,733 MW in Round 3). This reflects market participants' recalibration of LTDA economics for batteries, particularly as non-LIB technical maturity requirements became more stringent, and as some developers redirected capacity toward the ancillary services market (tertiary regulation) or the standard capacity market.

*Chart: LTDA contracted capacity (decarbonisation + LNG-dedicated), contract value (including net after refund deductions), and battery storage LIB/non-LIB trend across three rounds. Source: OCCTO/METI (May 2026)*

## IV. LNG Results and Policy Implications

| Metric | Round 1 (FY2023) | Round 2 (FY2024) | Round 3 (FY2025) |

|--------|-----------------|-----------------|-----------------|

| Procurement target (MW) | 6,000 | 2,240 | 2,930 |

| Total bids (MW) | 5,757 | 1,316 | 4,750 |

| Contracted volume (MW) | 5,757 | 1,316 | **3,039** |

| Clearing rate | 100% | 100% | **63.9%** |

| Annual contract value (¥B/yr) | 176.6 | 45.6 | 144.4 |

Round 3 LNG bids (4,750 MW) substantially exceeded the procurement target (2,930 MW), yet 1,713 MW went unawarded — the first time in three rounds that LNG bids have not been fully cleared. This outcome suggests that a portion of proposed LNG new-build capacity cannot clear LTDA's price review under current fuel cost and carbon policy conditions, marking a potential inflection point for Japan's LNG investment pipeline.

## V. Market Outlook

**Battery storage market**: Cumulative LTDA battery storage awards across three rounds now total 3,716 MW (LIB 2,346 MW + non-LIB 1,110 MW + pumped hydro 260 MW). As these assets enter commercial operation from FY2027 onwards, they will exert significant structural pressure on JEPX spot price spreads, particularly during solar-saturated midday hours when negative prices are already emerging.

**Nuclear new-build policy**: Ōma's LTDA award is the most tangible policy outcome of Japan's GX Promotion Act nuclear new-build programme to date. Key uncertainties remain around the commercial operation timeline, Hokkaido grid capacity constraints, and the capacity charge (容量拠出金) calculation methodology applicable to Hokkaido-area consumers.

**Mechanism design pressures**: The dramatic increase in net-of-rebate contract value (¥342.0B in Round 3 vs ¥94.5B in Round 2) highlights the LTDA's fiscal sensitivity to JEPX spot price levels. METI is reportedly considering a "priority contracting" mechanism that would give preference to projects already certified under the GX Promotion Act, to strengthen the policy signal embedded in the auction design.

*Sources: OCCTO "FY2025 LTDA Results Announcement" (May 13, 2026); METI "Long-Term Decarbonisation Auction Overview" (May 13, 2026)*