Introduction: Japan's BESS Market at a Structural Inflection Point

By the end of 2025, grid connection study applications for standalone BESS projects in Japan had reached 170.8 GW, more than doubling from 70 GW in mid-2024. Yet only 0.62 GW of BESS capacity has been physically connected to the national grid—a ratio of nearly 275:1 between applications and realized deployment. On March 1, 2026, TEPCO ordered its first-ever economic curtailment in the Tokyo grid area, cutting up to 1.84 million kW during peak solar hours. This milestone means all nine of Japan's grid areas have now experienced economic curtailment—a development that expands the strategic value of BESS from high-renewable-penetration regions to a truly national scale.

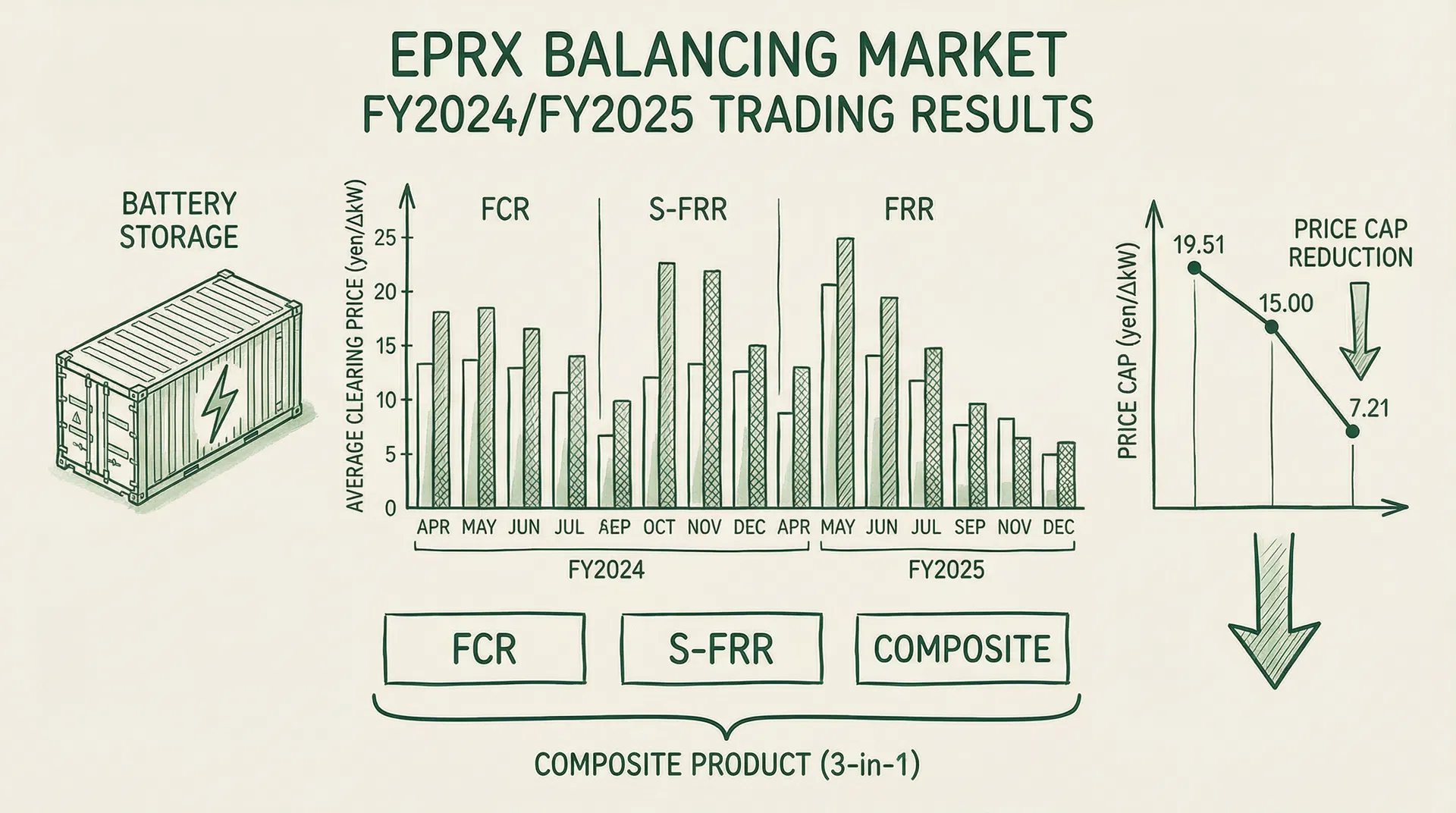

Revenue Structure: The Four-Market Stacking Model

| Revenue Source | Market Mechanism | Revenue Characteristics | FY2025 Reference |

|---|

| Spot Arbitrage | JEPX Day-Ahead Market | Variable, high volatility | Daily price spread ~¥20/kWh |

| Balancing Market | EPRX (FCR/S-FRR/Composite) | Weekly bidding, fixed cycles | FCR average ¥3.63/ΔkW·30min |

| Capacity Market/LTDA | OCCTO Main Auction/Long-Term Decarbonization Auction | Long-term fixed (LTDA: 20 years) | Capacity market average ~¥8,348/kW |

| OTC Bilateral Market | Tolling contracts, Battery PPA, Futures/Forwards | Long-term fixed or semi-fixed; improves bankability | EEX Japan 2025 volume: 149 TWh |

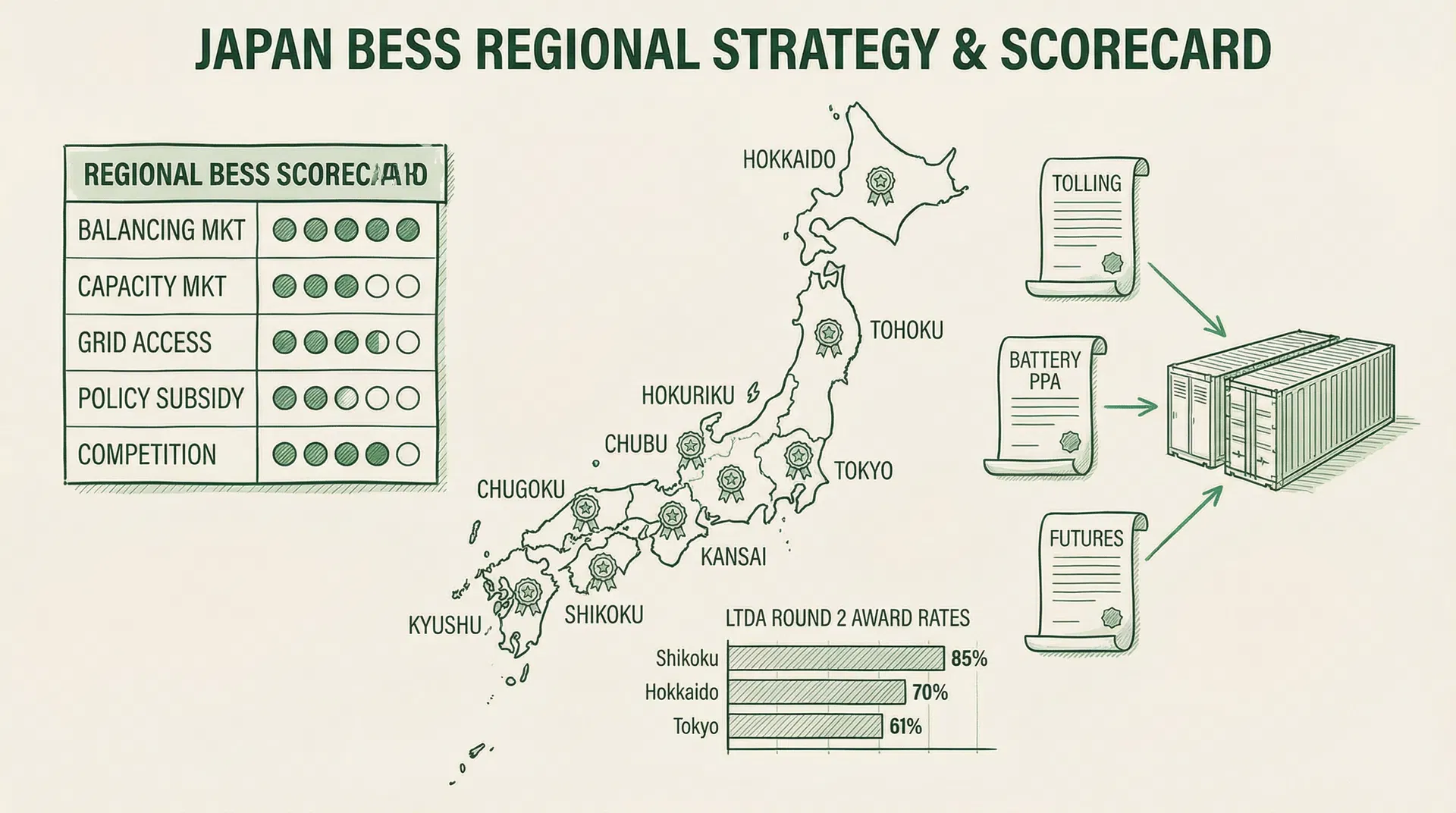

LTDA Round 2 Regional Award Analysis

| Area | Bid Volume (MW) | Awarded (MW) | Award Rate | Assessment |

|---|

| Shikoku | 812 | 692 | 85% | Highest award rate, strong demand |

| Hokkaido | 2,361 | 1,663 | 70% | High wind integration need |

| Tokyo | 4,057 | 2,481 | 61% | Largest awarded volume, deep market |

| Chugoku | 474 | 287 | 61% | Mid-scale, stable opportunities |

| Kansai | 738 | 361 | 49% | High nuclear baseload, moderate demand |

| Hokuriku | 232 | 96 | 41% | Small market |

| Chubu | 490 | 102 | 21% | Competitive, 60Hz area |

| Tohoku | 3,490 | 564 | 16% | Large bid volume, very low award rate |

| Kyushu | 965 | 99 | 10% | Lowest LTDA award rate (excess BESS competition); capacity market area price ¥15,112/kW (highest nationally) |

OTC Bilateral Market: BESS's Fourth Revenue Pathway

Against the backdrop of balancing market price cap reductions and intensifying LTDA competition, the OTC bilateral market is emerging as an indispensable fourth revenue pathway for BESS developers. In 2025, EEX Japan's trading volume reached 149 TWh (97% market share), more than 20 times higher than 2021 levels. Yet Japan's OTC market remains at just 0.2 times annual electricity consumption—compared to Germany's 12–13 times—indicating vast room for growth. Eurasia Group estimates Japan could reach 2,500 TWh by 2030, potentially becoming one of the world's largest traded power markets.

Three BESS OTC Business Models

| Model | Structure | Revenue Source | Best Suited For |

|---|

| Direct Market Participation | BESS operator directly participates in JEPX spot and futures markets | Spot arbitrage + futures hedge revenue | Large developers with trading capabilities |

| Aggregator Model | Contracts with licensed aggregator for market access | Revenue sharing or fixed fees | Mid-size developers without direct market access |

| Tolling Model | Long-term tolling contract with power retailer; operator transfers control in exchange for fixed tolling fee | Tolling fee (capacity payment) + variable component | Project-financed developers needing revenue certainty |

The tolling model is currently the most closely watched OTC structure among international BESS developers. On September 24, 2025, Akaysha Energy (Australia, one of the world's largest BESS developers) hosted an event in Tokyo on "utility-scale batteries and innovative tolling arrangements," with Orrick's Tokyo office serving as legal advisor. This signals that international mainstream BESS developers are actively pushing tolling contract structures in Japan.

Battery PPA: The Key to Renewable Integration

Battery PPA is another important OTC structure, particularly suited for co-located renewable energy + BESS projects. Under this model, the service provider installs and maintains the BESS, while the off-taker pays based on capacity or energy throughput without bearing upfront capital costs, over a contract term of typically 10–20 years. Payment structures include capacity payments (per MWh of available storage), energy throughput payments (per MWh discharged), and grid services payments (revenue sharing from ancillary services). Reference cases include Marubeni's 100 MWh project in Hokkaido and Gurin Energy's (Singapore) 2 GWh facility scheduled to begin construction in 2026.

Futures and Forward Contracts: Hedging Spot Revenue

For BESS operators pursuing spot arbitrage strategies, EEX Japan's futures contracts provide critical hedging tools. By simultaneously buying futures for charging hours (locking in low prices) and selling futures for discharging hours (locking in high prices), BESS operators can convert highly variable spot arbitrage revenue into more predictable cash flows, reducing financing costs. EEX Japan added fiscal year contracts (April–March) in April 2025, launched order book trading in April 2025, and introduced monthly power options for Tokyo and Kansai areas in February 2025.

Medium-to-Long-Term Physical Trading Market (2028 Launch): The Largest Future Opportunity

METI is planning a new "medium-to-long-term physical power trading market" for 2028, enabling retailers to procure physical power 1–3 years in advance to meet the FY2030 procurement obligation (50–70% secured 3 years ahead). BESS operators can participate as sellers of future discharge capacity, potentially creating LTDA-like long-term fixed revenues without going through a competitive auction process. This represents the single largest structural shift in Japan's BESS OTC landscape over the next five years.

Superpeak Swap: A New OTC Product Pioneered by BESS

Against the backdrop of declining balancing market price caps and intensifying LTDA competition, the "Superpeak Swap" has emerged as one of the most rapidly growing OTC products among Japan's BESS operators. It is a fixed-for-floating electricity exchange contract targeting the evening peak period (typically 16:00–20:00), where power retailers pay a fixed unit price to hedge against JEPX spot price spikes, while BESS operators discharge during the contracted window to earn fixed revenues.

This time window is particularly valuable because solar generation drops sharply while demand peaks simultaneously, creating the most volatile JEPX spot prices of the day. For BESS operators, this window has minimal overlap with the balancing market (which runs around the clock), enabling Superpeak Swap to be stacked as a genuine "fourth revenue pillar." Critically, the fixed revenue stream can serve as collateral in project finance structures, dramatically improving the bankability of merchant BESS projects.

Case Study: HDRE Group (Star Trade Japan) × Chubu Electric Power Miraiz (January 2026)

On January 27, 2026, Star Trade Japan (Hoshiboshi Denryoku Japan Co., Ltd.), a subsidiary of HD Renewable Energy (HDRE, TPEX: 6873), and Chubu Electric Power Miraiz Co., Ltd. signed a peak-hour power supply and demand contract utilizing grid-scale battery storage. This marks HDRE Group's first commercial deployment of an insurance-based energy hedging solution in Japan, and stands as a landmark case study for the Superpeak Swap model.

| Parameter | Details |

|---|

| Seller (BESS Operator) | Star Trade Japan / Hoshiboshi Denryoku Japan (HDRE Group) |

| Buyer (Power Retailer) | Chubu Electric Power Miraiz Co., Ltd. (Chubu Electric Group) |

| Contracted Hours | 16:00–20:00 (evening peak) |

| Initial Contract Scale | 10 MW (5 sites in Chubu area) |

| Annual Volume | Approx. 9.09 million kWh |

| Operations Start | April 2026 |

| Expansion Plan | Considering scale-up to up to 300 MW |

The Chubu region is the heart of Japan's automotive and heavy manufacturing industry, with dense, price-sensitive electricity demand. Chubu Electric Power Miraiz procures a portion of its electricity from the JEPX spot market, making evening peak price spikes a significant operational risk. Under this agreement, the retailer gains stable fixed-price procurement during peak hours, while Star Trade partially stabilizes returns from its storage assets through structured agreements. Technically, the solution integrates AI-powered price forecasting models (adapted from Star Trade's proven Australian market framework) with real-time charge/discharge control via the proprietary Star Trade Platform.

Case Study: HDRE Helios (Hokkaido) — The 100% Merchant BESS Finance Model

In March 2026, HDRE's Hokkaido Helios project (50 MW / 104 MWh) secured approximately JPY 5.4 billion in project financing, issuing Japan's first green project bond backed by grid-scale battery storage assets. Arranged by Nomura Capital Investment and Nomura Securities, the bond received a BBB investment-grade rating from R&I, with a financing tenor of up to 19 years.

Helios operates under a 100% merchant model with no subsidies or fixed-price offtake contracts, generating revenue through two pillars: JEPX spot trading and EPRX balancing market participation — without Superpeak Swap. Traditional project finance markets favor assets with predictable cash flows such as FIT-backed generation; Helios secured financing through the demonstrated stability of its dispatch-optimized spot arbitrage revenues and periodic balancing market award income. This case shows that Merchant BESS can achieve long-term project financing even without Superpeak Swap. Note that Superpeak Swap is a separate OTC product HDRE developed independently for the Chubu area (see above section) — a different commercial model from Hokkaido Helios. Together, these two cases illustrate HDRE's diversified Japan BESS strategy: breaking through with pure merchant financing in Hokkaido, while pioneering a retailer hedging market with Superpeak Swap in Chubu. These cases demonstrate that Superpeak Swap has the potential to fundamentally transform Superpeak Swap (OTC). Traditional project finance markets have historically favored assets with predictable cash flows such as FIT-supported projects. The "semi-fixed" revenue anchor provided by Superpeak Swap contracts secured the project's bankability, enabling long-term financing. This case demonstrates the potential for Superpeak Swap to fundamentally reshape the financing structure of merchant BESS projects in Japan.

Superpeak Swap's Role in the Revenue Stacking Framework

| Revenue Source | Time Window | Revenue Characteristics | Contribution to Bankability |

|---|

| Balancing Market (FCR/S-FRR) | All hours | High unit price but cap declining | Moderate |

| JEPX Spot Arbitrage | All hours | High volatility, AI-dependent | Low |

| Superpeak Swap (OTC) | 16:00–20:00 | Fixed revenue, strong time complementarity | High (functions as financing collateral) |

| Capacity Market (LTDA) | Full year | 20-year fixed but competition intensifying | Highest |

Nine-Area Scorecard

Scoring criteria: A Balancing Market (FCR/S-FRR award opportunities), B Capacity Market (LTDA award rate), C Grid Access Difficulty (inverse scoring—easier = higher score), D Policy Subsidy Accessibility, E Competition Intensity (inverse scoring), F Spot Arbitrage Potential (curtailment rate, daily peak-valley price spread), G Day-Ahead/Intraday Market Opportunity (day-ahead balancing market liquidity from FY2026). Each dimension scored 1–5; total out of 35.

| Area | A. Balancing | B. Capacity | C. Grid Access | D. Subsidies | E. Competition | F. Spot Arb. | G. Day-Ahead | Total |

|---|

| 🥇 Hokkaido | ★★★★★(5) | ★★★★★(5) | ★★★☆☆(3) | ★★★★☆(4) | ★★★☆☆(3) | ★★★★★(5) | ★★★★☆(4) | 29/35 |

| 🥈 Shikoku | ★★★★☆(4) | ★★★★★(5) | ★★★★☆(4) | ★★★★☆(4) | ★★★★☆(4) | ★★★★☆(4) | ★★★☆☆(3) | 28/35 |

| 🥉 Chugoku | ★★★★☆(4) | ★★★★☆(4) | ★★★☆☆(3) | ★★★☆☆(3) | ★★★★☆(4) | ★★★★☆(4) | ★★★☆☆(3) | 25/35 |

| Kyushu | ★★★★★(5) | ★★☆☆☆(2) | ★★☆☆☆(2) | ★★★☆☆(3) | ★★☆☆☆(2) | ★★★★★(5) | ★★★★☆(4) | 23/35 |

| Tohoku | ★★★★☆(4) | ★☆☆☆☆(1) | ★★★☆☆(3) | ★★★☆☆(3) | ★★★★☆(4) | ★★★☆☆(3) | ★★★☆☆(3) | 21/35 |

| Tokyo | ★★★☆☆(3) | ★★★★☆(4) | ★★☆☆☆(2) | ★★☆☆☆(2) | ★★☆☆☆(2) | ★★★☆☆(3) | ★★★★☆(4) | 20/35 |

| Chubu | ★★☆☆☆(2) | ★★☆☆☆(2) | ★★★☆☆(3) | ★★★★☆(4) | ★★★★☆(4) | ★★★☆☆(3) | ★★★☆☆(3) | 21/35 |

| Kansai | ★★★☆☆(3) | ★★★☆☆(3) | ★★☆☆☆(2) | ★★☆☆☆(2) | ★★★☆☆(3) | ★★★☆☆(3) | ★★★☆☆(3) | 19/35 |

| Hokuriku | ★★☆☆☆(2) | ★★★☆☆(3) | ★★★★☆(4) | ★★☆☆☆(2) | ★★★★☆(4) | ★★☆☆☆(2) | ★★☆☆☆(2) | 19/35 |

Short-Term Strategy Framework (FY2025-2026)

| Strategy | Target Areas | Core Logic | Key Risk |

|---|

| Balancing Market Priority | Tokyo, Shikoku, Hokkaido | Lock in high revenue before price cap reduction; FCR shortage rates still elevated | Revenue compression when cap drops to ¥7.21 in FY2026 |

| Spot Arbitrage + Futures Hedge | Tokyo, Kyushu (co-located) | Daily spread ~¥20/kWh; use EEX futures to lock in future price spreads | Battery cycle life consumption; futures liquidity still limited |

| Tolling Contract Negotiation | Tokyo, Hokkaido, Shikoku | Lock in long-term OTC tolling fees before competition intensifies; improves bankability | Counterparty credit risk; complex tolling fee negotiations |

| Day-Ahead Market Preparation | All areas | FY2026 April transition from weekly to day-ahead trading; early preparation critical | Market rules not fully finalized |

Long-Term Strategy Framework (FY2027+)

With LTDA Round 3's changed competitive landscape and continued balancing market price cap reductions, the core of long-term strategy shifts toward "revenue diversification" and "OTC market deepening." The 2028 launch of the medium-to-long-term physical power trading market will create entirely new long-term OTC revenue opportunities for BESS—operators can sell future discharge capacity to retailers without going through competitive auctions. The FY2030 retailer procurement obligation (50–70% secured 3 years ahead) will dramatically increase demand for BESS tolling contracts and Battery PPAs, further deepening OTC market liquidity. Developers who begin building OTC partnerships with major power retailers today will be best positioned when this market matures in 2028–2030.

Policy Subsidy Overview

| Subsidy Type | Rate | Conditions | Coverage |

|---|

| METI National Subsidy (Standard) | 50% of installation cost | >10MW, discharge time <6h | All areas |

| METI National Subsidy (Long-Duration) | 66% of installation cost | >10MW, discharge time ≥6h | All areas |

| Tokyo Metropolitan Government | Up to 2/3 of installation cost | Cap: ¥2B/project; ¥13B total FY2025 budget | Tokyo area |

| LTDA 20-Year Fixed Revenue | Pay-as-bid | Must win competitive auction | All areas |

Conclusion: From "First-Mover Advantage" to "Precision Deployment"

Japan's BESS market is transitioning from the "speculative application boom" of 2023–2024 toward a more rational "precision deployment" phase. Area selection has never been more critical. Hokkaido leads the nine-area scorecard with a top score of 29/35, driven by strong wind integration demand, FCR award opportunities, and spot arbitrage potential. Shikoku (28/35) ranks second with the highest national LTDA award rate (85%) and low competition intensity, offering greater bilateral contract negotiating leverage. Chugoku (25/35) provides stable mid-scale opportunities. Kyushu and Tohoku show clear structural demand but require careful assessment of grid bottlenecks and competitive saturation. Tokyo ranks sixth overall, yet its highest capacity market prices, most generous local subsidies, and most mature OTC market continue to make it an important target for large institutional investors.

Over the next 2–3 years, the maturation of the OTC market—particularly the 2028 launch of the medium-to-long-term physical power trading market—will provide BESS developers with entirely new revenue pathways, evolving Japan's BESS business model from "three-market stacking" to "four-market stacking." Developers who begin building OTC partnerships today will be best positioned for this transition.

"In Japan's BESS market, choosing the right grid area matters as much as choosing the right technology. The combination of grid connection location, competitive landscape, policy subsidies, and OTC partnership strategy determines the ultimate revenue ceiling of any project."