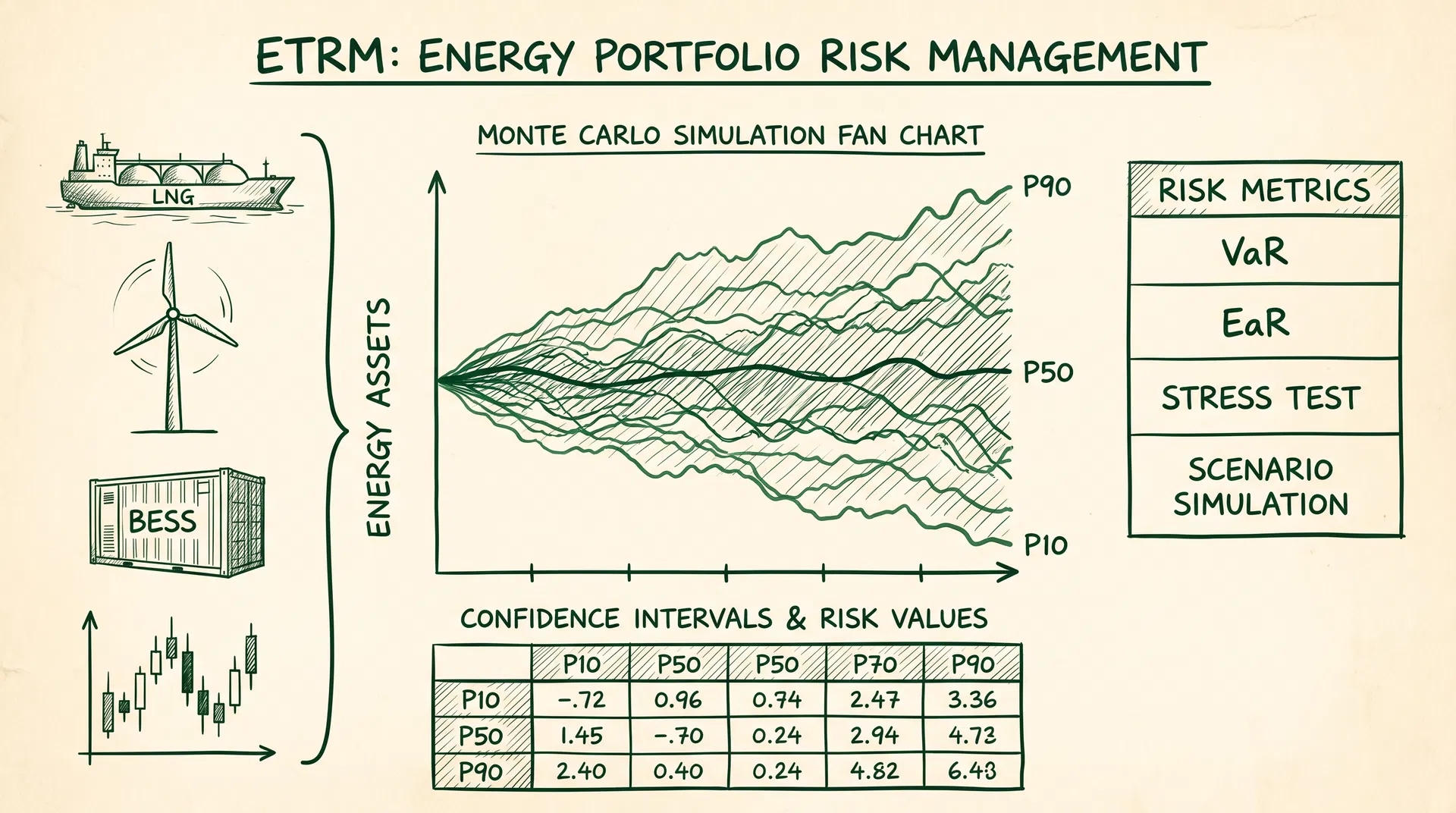

ETRM in Depth: Risk Quantification, Scenario Simulation & Portfolio Management in Japan's Power Market

This article systematically introduces the advanced application of ETRM (Energy Trading and Risk Management) in Japan's power market: from short-, medium-, and long-term price forecasting, Monte Carlo scenario simulation, and stress testing, to the computational frameworks for EaR (Earnings at Risk) and VaR (Value at Risk). It further explores how portfolio management combining LNG long-term contracts, renewable energy PPAs, BESS, JEPX spot, and JPX futures can achieve risk-return optimization in Japan's uniquely high-volatility market environment.