Following the restart of Kashiwazaki-Kariwa Unit 6 in March 2026, the Tokyo metropolitan area experienced its first-ever renewable energy curtailment. This report analyzes how nuclear priority dispatch rules cause solar and wind curtailment, and examines policy responses including BESS deployment, transmission expansion, and FIT-to-FIP reform.

Executive Summary

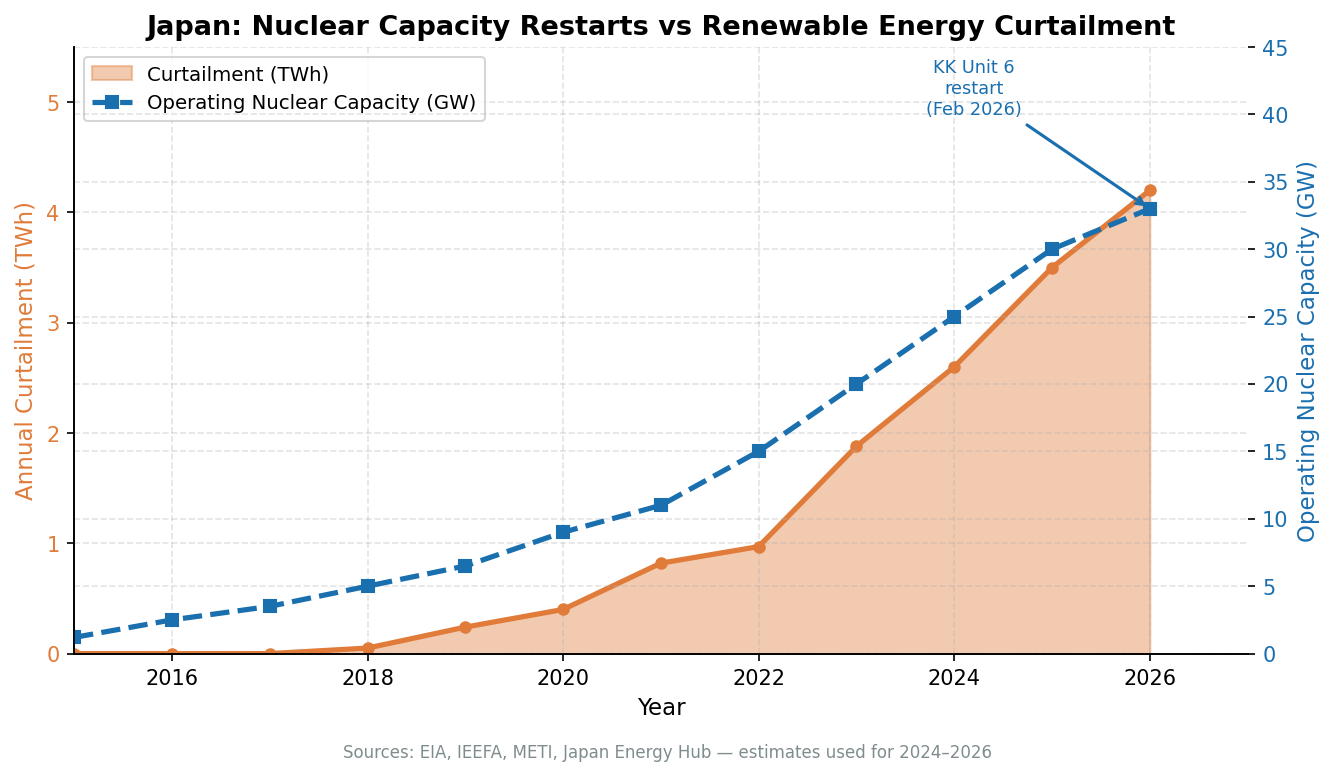

In early 2026, the Tokyo Electric Power Company (TEPCO) restarted Unit 6 of the Kashiwazaki-Kariwa Nuclear Power Plant—the world's largest nuclear facility by installed capacity. After a 15-year hiatus following the 2011 Fukushima disaster, the 1.35 GW reactor reached full output in early March 2026. While this restart bolsters Japan's energy security and displaces imported natural gas, it simultaneously catalyzed a historic milestone: the first-ever economic curtailment of renewable energy in the Tokyo metropolitan area. This report analyzes how the reintroduction of large-scale, inflexible baseload nuclear power intersects with Japan's growing solar and wind capacity, examining the direct mechanisms that triggered the Tokyo curtailment events, the indirect spillover effects across other regional grids, and the structural policy challenges Japan faces in balancing its dual goals of decarbonization and energy security.

1. The Catalyst: Kashiwazaki-Kariwa Unit 6 Restart

The Kashiwazaki-Kariwa Nuclear Power Station, located in Niigata Prefecture, comprises seven reactors with a combined capacity of nearly 8 GW, making it the world's largest nuclear facility. Unit 6 is the first to resume operations: after achieving reactor criticality on January 21, 2026, the unit was reconnected to the grid on February 9 and reached its rated full output of 1,356 MW on March 3.

The U.S. Energy Information Administration (EIA) estimates that Unit 6 will generate approximately 9.5 TWh annually, displacing roughly 1.3 million tons of liquefied natural gas (LNG). This aligns with the Japanese government's 7th Strategic Energy Plan, which targets a 20% nuclear share by fiscal year 2040 to reduce reliance on imported fossil fuels. However, the sudden injection of 1.35 GW of baseload power into the TEPCO grid fundamentally altered the region's supply-demand balance during low-demand periods.

2. The Direct Impact: Curtailment Reaches Tokyo

Historically, the Tokyo area—Japan's largest load center—was a net importer of electricity and the last remaining grid region to avoid renewable energy curtailment. This changed on March 1, 2026.

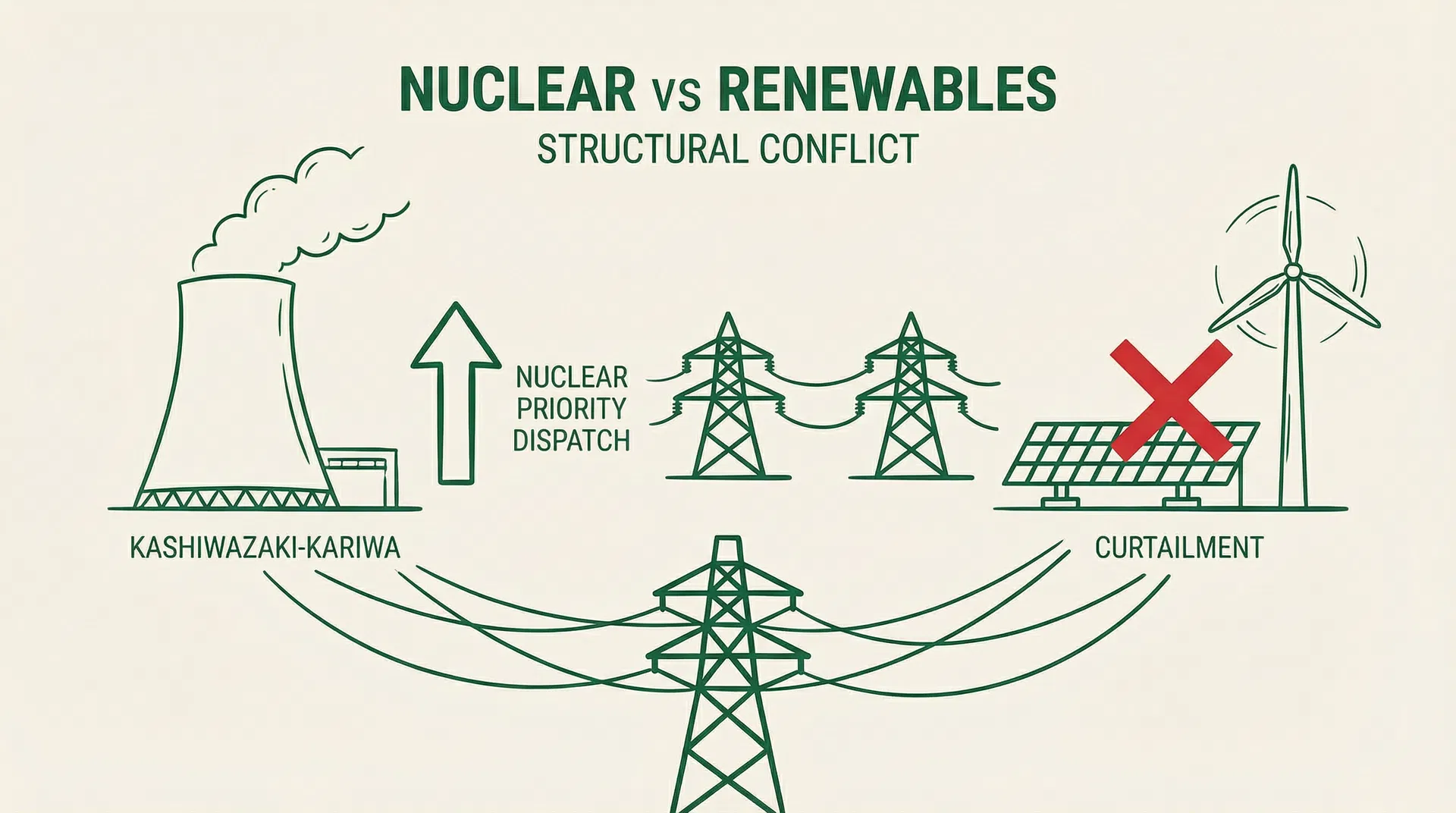

On a Sunday characterized by unusually warm spring weather and low industrial demand, solar generation in the Kanto region surged. Concurrently, Kashiwazaki-Kariwa Unit 6 was operating near its full 1.35 GW capacity. Because nuclear power operates as an inflexible baseload source and is legally protected from curtailment under Japan's grid rules, TEPCO was forced to curtail 1,840 MW of generation at its peak—comprising 1,810 MW of solar and wind, and 40 MW of biomass.

This event was not an anomaly. Subsequent curtailments occurred on March 7 (870 MW) and March 8. Notably, on March 21, TEPCO issued a curtailment order even when the nuclear plant was temporarily offline due to an electrical fault, indicating that while the nuclear restart was the immediate catalyst, the underlying volume of renewable capacity has now exceeded the grid's baseline flexibility.

Figure 1: Japan's operating nuclear capacity (GW) vs. annual renewable energy curtailment (TWh), 2015–2026. Sources: EIA, IEEFA, METI, Japan Energy Hub — estimates used for 2024–2026. Source: powertrading.club

"The onset of curtailment in the Tepco area is highly significant because it shows that even in Japan's largest power market—Tokyo, historically a net-importing load center—renewable deployment has begun to outpace system flexibility. This signals that curtailment is no longer a regional issue confined to areas like Kyushu, but a nationwide structural challenge." — Michiyo Miyamoto, Institute for Energy Economics and Financial Analysis (IEEFA)

3. The Systemic Mechanism: Priority Dispatch Rules

To understand why renewable energy is curtailed when nuclear plants restart, one must examine Japan's priority dispatch rules. When electricity supply exceeds demand, grid operators must reduce output to maintain grid frequency. The mandated order of reduction is as follows:

Priority Level

Generation Source

Curtailment Action

1st (First)

Thermal Power (Coal, LNG, Oil)

Reduced to minimum stable generation (typically 30–50% of capacity)

2nd

Pumped Hydro Storage

Activated to absorb excess power (if reservoir capacity allows)

3rd

Inter-regional Transmission

Excess power exported to neighboring grid regions

4th

Biomass Generation

Fully curtailed

5th

Solar and Wind (Variable RE)

Fully curtailed

6th (Last, Protected)

Nuclear, Geothermal, Run-of-river Hydro

Protected as "long-term fixed sources"; curtailed only as an absolute last resort

Under this framework, nuclear power is effectively immune to economic curtailment. When Kashiwazaki-Kariwa Unit 6 operates, it occupies a fixed 1.35 GW block of the grid's capacity. Furthermore, thermal plants cannot be completely shut off due to the technical requirements of ramping them back up for the evening peak; they must run at 30–50% capacity. Consequently, solar and wind operators bear the brunt of the curtailment burden, absorbing the financial losses of ungenerated electricity.

4. Indirect Impacts: The National Ripple Effect

The dynamic observed in Tokyo is a magnification of a structural issue that has been developing nationwide since 2018. As more nuclear reactors restart across Japan, the curtailment of renewable energy intensifies, often spilling across regional borders.

4.1 The Kyushu Precedent

The Kyushu region serves as the clearest example of this interaction. Kyushu Electric Power has restarted all four of its commercial nuclear reactors (Genkai 3 & 4, and Sendai 1 & 2). By fiscal year 2023, nuclear power accounted for 39% of Kyushu's total generation. Concurrently, Kyushu possesses over 12.8 GW of solar capacity. With nuclear occupying the baseload and inter-regional transmission to Honshu capped at 2.78 GW, Kyushu experienced an 8.3% renewable curtailment rate in FY2023, representing roughly 12.9 TWh of lost clean energy.

4.2 Inter-regional Spillover

The restart of nuclear plants also causes indirect curtailment in neighboring regions. As the Kansai region restarted its nuclear fleet—increasing its nuclear generation share from 31% in FY2022 to 44.4% in FY2023—the region became more self-sufficient. This reduced Kansai's need to import electricity from the neighboring Shikoku and Chugoku regions. Stripped of their primary export market, Shikoku and Chugoku were forced to drastically increase the curtailment of their own domestic solar and wind generation.

Nationally, solar and wind curtailment reached a record 1.88 TWh in FY2023 and accelerated further to 1.74 TWh in just the first half of 2025. The trajectory suggests that as Japan aims to restart up to 30 reactors to meet its 2040 targets, renewable curtailment will continue to escalate unless structural grid reforms are implemented.

5. Structural Bottlenecks and Policy Responses

5.1 Transmission Constraints

Japan's grid is highly fragmented. Hokkaido and Kyushu possess the greatest renewable energy potential, yet they are physically isolated from the major demand centers in Tokyo and Osaka. The interconnection capacity between Hokkaido and Honshu is currently limited to 900 MW, while upgrading Hokkaido's internal transmission network would cost an estimated JPY 1.1 trillion (USD 7.6 billion). The current regulatory framework requires local ratepayers to bear these upgrade costs, making large-scale transmission expansion financially prohibitive without national cost-sharing reforms.

5.2 Proposed Solutions

Battery Energy Storage Systems (BESS): Private investment is accelerating. In April 2026, a consortium led by Tokyu Land announced a JPY 30 billion investment in 174 MW of grid-scale storage, while Neoen is advancing a 100 MW / 400 MWh facility in Hyogo.

Data Center Relocation: The Ministry of Economy, Trade and Industry (METI) has launched subsidy programs covering up to 50% of setup costs for data centers willing to locate in Kyushu and Hokkaido, aiming to align new electricity demand directly with areas of high renewable generation.

Market Reforms: To incentivize flexibility, METI is pushing renewable asset owners to transition from fixed Feed-in-Tariff (FIT) contracts to Feed-in-Premium (FIP) schemes. A forthcoming rule change will prioritize the dispatch of FIP assets over FIT assets during curtailment events, effectively forcing older solar plants to co-locate with batteries or face severe financial losses.

Supplementary: Tokyo Power Grid — Capacity Mix, Demand Structure, and BESS Landscape

Generation Mix Overview (End of 2025)

The TEPCO service territory (primarily the Kanto region) is Japan's largest single electricity demand center, consuming approximately 288 TWh annually—roughly 34% of the national total. Its generation mix has undergone fundamental transformation since 2011 and is entering yet another structural adjustment phase following the Kashiwazaki-Kariwa restart.

Generation Type

Capacity (GW)

Share (est.)

Key Characteristics

LNG Thermal (JERA)

~40

~47%

Dispatchable, primary balancing resource

Solar PV (FIT/FIP)

~18

~21%

Midday surplus in spring/autumn sunny days

Pumped Hydro

~6.2

~7%

Key peaking resource, reservoir-constrained

Nuclear (KK Unit 6)

1.356

~2%

Baseload, non-dispatchable, priority dispatch

Coal

~10

~12%

Baseload, low operational flexibility

Wind / Biomass / Other

~9

~11%

Distributed, variable output

Historical Evolution of the Power Mix (2011–2026)

Year

Key Event

Impact on Generation Mix

2011

Fukushima accident; nationwide nuclear shutdown

LNG share surged to 55%+; electricity prices spiked

2012

FIT scheme launched

Solar PV capacity began exponential growth

2015–2018

Nuclear restarts in Kyushu and other regions

First curtailment events in Kyushu; LNG demand began declining

2022–2024

Curtailment surge nationwide

FY2023 national curtailment reached record 1.88 TWh

Feb 2026

Kashiwazaki-Kariwa Unit 6 restart (1,356 MW)

First curtailment in Tokyo; ~1.3 Mt LNG displaced annually

Electricity Demand Structure

Demand Sector

Share (est.)

Trend

Commercial (offices, retail, hotels)

~45%

Partially offset by remote work; data center demand growing rapidly

Residential

~30%

Slow long-term decline due to population shrinkage and efficiency gains

Industrial (manufacturing)

~25%

Below national average; relatively stable

According to OCCTO's latest demand forecast, driven by a data center construction boom and semiconductor factory expansion, the national demand is projected to grow at an average annual rate of approximately 1.1% from 2024 to 2034, with the TEPCO service territory expected to reach approximately 288.3 TWh by 2034.

BESS Status and Outlook

According to IEEFA's March 2026 report, only 0.62 GW of grid-scale BESS capacity has been physically connected to Japan's national grid (up from just 0.07 GW in early 2024), compared to 170.8 GW in applications—a gap of 275 times.

BESS Market Indicator

Value (end-2025)

Physically grid-connected (nationwide)

0.62 GW

Under contract (LTDA, etc.)

28.7 GW

Under grid connection study

170.8 GW

Tokyo Metropolitan Gov. FY2025 subsidies (15 projects)

187.8 MW / 758.9 MWh

LTDA Decarbonization Auction (Rounds 1+2)

2.4 GW

Japan BESS construction cost (FY2024)

~JPY 68,000/kWh (2.5–3x global average)

The normalization of curtailment in the Tokyo area is creating powerful market incentives for BESS. During curtailment periods, JEPX spot prices collapse to ¥0.01/kWh, while evening peak prices reach ¥10–15/kWh—creating substantial arbitrage opportunities for early BESS entrants.

6. Conclusion

The restart of Kashiwazaki-Kariwa Unit 6 is a watershed moment for Japan's energy policy. While it successfully reduces reliance on imported fossil fuels and provides zero-carbon baseload power, it has exposed the profound inflexibility of the Japanese power grid. By pushing the Tokyo metropolitan area into economic curtailment for the first time, the restart demonstrates that Japan's current priority dispatch rules—which protect nuclear generation at the expense of solar and wind—are fundamentally incompatible with the simultaneous expansion of both energy sources.

Without aggressive investment in inter-regional transmission lines, grid-scale battery storage, and demand-side flexibility, the continued restart of Japan's nuclear fleet will result in the increasing curtailment of renewable energy, undermining the economic viability of future wind and solar projects.

This site uses cookies to remember your language preference and collect anonymous traffic statistics to improve our content. You can choose to accept or decline non-essential cookies. Learn more