Japan's Long-Term Decarbonization Power Supply Auction (LTDA) guarantees 20-year fixed-cost recovery to incentivize large-scale investment in decarbonized power sources. However, the widely cited "90% refund rule" is not a flat rate — it operates as a three-tier structure. This article provides a comprehensive breakdown of how LTDA revenue is calculated and what rights and obligations fall on successful bidders.

1. The Two-Layer Revenue Structure

LTDA revenue consists of two fundamentally different income streams.

① Fixed Income (Capacity Assurance Contract Amount)

An annual capacity payment (JPY/kW/year) paid by OCCTO for 20 years, based on the winning bid price. This income is designed to recover construction costs and fixed O&M expenses. It is indexed to core CPI for annual adjustments and is entirely retained by the operator — no refund obligation applies.

② Market Revenue (Other Market Income)

Revenue earned from operating in the JEPX wholesale market, the balancing market (ΔkW) [Primary, Secondary ①②, Tertiary ①②], non-fossil value certificate markets, and equivalent PPA arrangements. Since fixed costs are already covered by ①, this income functions as a bonus layer. However, the majority must be returned to OCCTO under the tiered refund rules.

Core principle: Fixed income (①) is retained 100% by the operator. Market revenue (②) is subject to the three-tier refund obligation. The refund applies only to ② — never to ①.

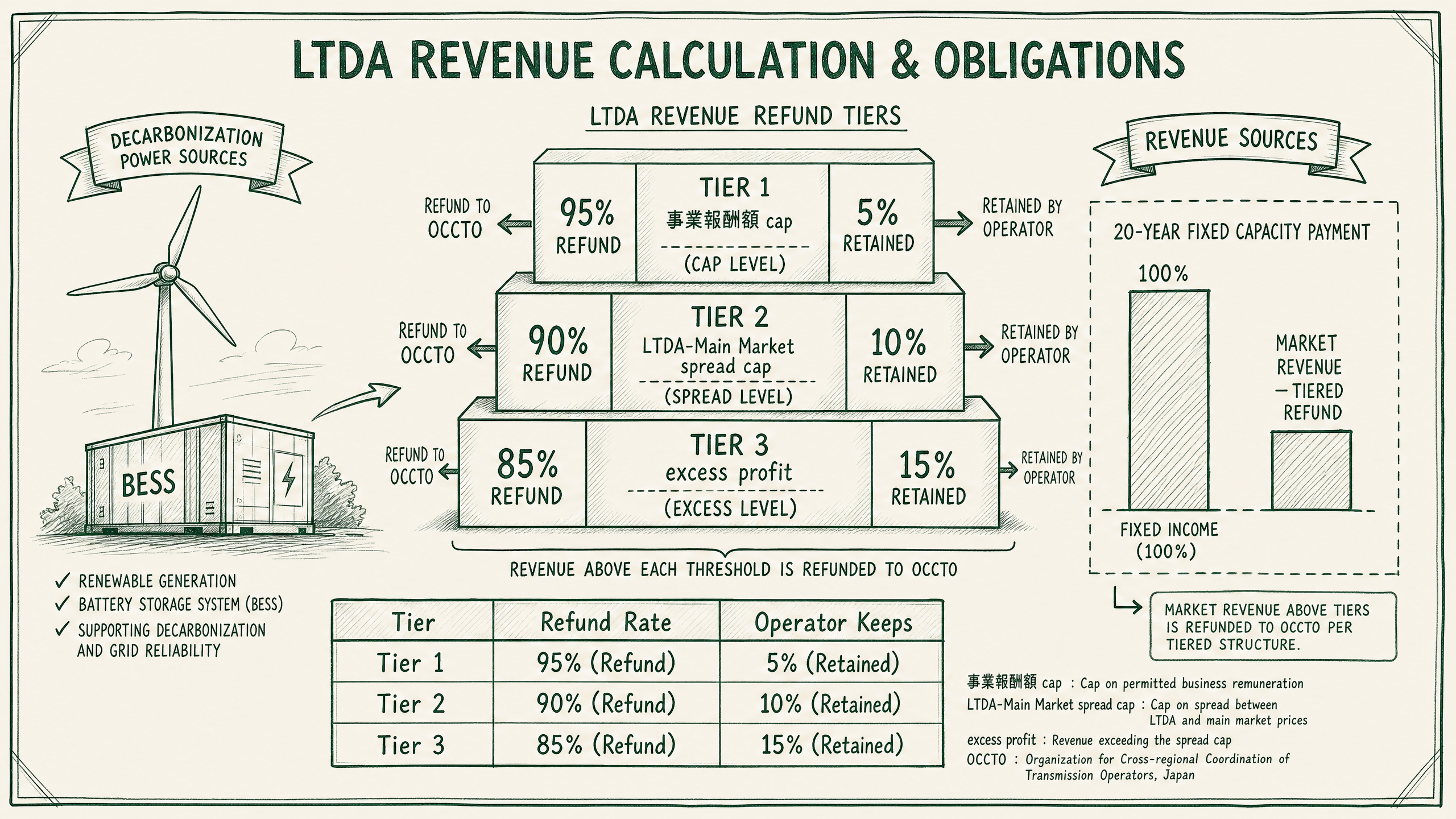

2. The Three-Tier Refund Structure

The "90% refund rule" is a simplification. The actual mechanism has three tiers:

| Tier |

Applicable Range |

Refund Rate |

Operator Retains |

| Tier 1 |

Market revenue up to the Business Return Amount |

95% |

5% |

| Tier 2 |

Above Business Return Amount, up to the spread between LTDA contract price and Main Auction price |

90% |

10% |

| Tier 3 |

Excess profit above Tier 2 ceiling |

85% |

15% |

Business Return Amount: The appropriate profit embedded in the bid price, calculated by OCCTO using a WACC-based formula applied to the investment base. Rounds 1–2 used a uniform 5% WACC for all power source types. From Round 3 (FY2025 bidding), WACC is differentiated by lead time: 4%/5%/6%. Battery storage, with a 4-year lead time, is now subject to a 4% WACC cap. → Glossary: Business Return Amount

Cost Line Items in the 事業報酬額 Calculation

The bid price includes both fixed costs and variable costs:

| Cost Category |

Key Line Items |

| Fixed Costs (Capital) |

Construction costs (capex), capital cost (WACC × investment base), property tax, insurance, fixed O&M (scheduled maintenance, repairs, personnel, miscellaneous) |

| Fixed Costs (O&M) |

Fixed personnel costs, fixed repair costs, fixed consumables, grid connection fees (fixed portion) |

| Variable Costs |

Fuel costs, purchased power, imbalance profit/loss, generation-side charges (kWh levy), market transaction fees |

The 事業報酬額 represents the "appropriate investor return" applied to the fixed cost portion (especially capital costs) via WACC. Variable costs are deducted from other market revenues as "actual variable costs" during clawback calculations.

Why three tiers? Tier 1 (95% refund) prevents double-counting of profit already embedded in the bid. Tier 2 (90% refund) captures the spread between the LTDA fixed price and the main market price — the structural excess return from the price guarantee. Tier 3 (85% refund) applies when markets spike unexpectedly, leaving operators a modest upside to reward operational excellence.

3. Scope of the Market Revenue Refund Obligation

The following revenue sources are subject to the refund obligation:

| Revenue Source |

Subject to Refund |

Notes |

| JEPX spot and intraday market |

Yes |

Primary refund target |

| Balancing market (ΔkW) |

Yes |

Primary, Secondary ①②, Tertiary ①② |

| Non-fossil value certificates |

Yes |

Includes FIT non-fossil certificates |

| Capacity market (Main Auction) income |

Yes |

When overlapping with LTDA contracted capacity |

| Corporate PPA revenue (at market-equivalent pricing) |

Yes |

Premiums above market price also included |

| LTDA fixed income (capacity assurance contract amount) |

No |

Retained 100% by operator |

The critical point is that the LTDA fixed income itself is never subject to refund. The obligation applies exclusively to revenue earned in other markets.

3-1. Financial Contract Income (Virtual Toll, etc.) and Refund Obligations

For income derived from financial cash-settled bilateral contracts such as "Virtual Toll" arrangements, OCCTO official documents do not contain explicit provisions. However, the following framework applies in practice:

| Nature of Income |

Included in Other Market Revenue |

| Bilateral power sales revenue (treated as kWh income) |

Included (refund obligation applies) |

| Hedge profit/loss (linked to kWh income or variable costs) |

Included (refund obligation applies) |

| Pure financial derivative profit/loss |

Requires individual confirmation (may not meet the "other income" definition under current rules) |

Note: Whether Virtual Toll and similar financial contract income is counted as "other market revenue" depends on the nature of the contract and accounting treatment. Confirmation with OCCTO/METI on a case-by-case basis is recommended.

Source: Electricity and Gas Market Surveillance Commission, "Report on Monitoring Other Market Revenue in Long-Term Decarbonisation Auctions" (31 July 2025)

4. Worked Example

The following illustrates revenue calculation for a 30 MW (6-hour) battery storage project.

Assumptions

- LTDA contract price: JPY 70,000/kW/year

- Installed capacity: 30 MW (30,000 kW)

- Business Return Amount: approx. JPY 150 million/year (WACC 4% × investment base)

- Annual market revenue: JPY 500 million (JEPX + balancing market combined)

- Main Auction contract price: JPY 35,000/kW/year

Fixed Income (①)

LTDA Fixed Income = 70,000 JPY/kW/year × 30,000 kW = JPY 2,100 million/year

Market Revenue Refund Calculation (②)

Tier 1 ceiling = Business Return Amount = JPY 150 million

→ Refund = 150M × 95% = JPY 142.5 million

→ Retained = 150M × 5% = JPY 7.5 million

Tier 2 ceiling = (LTDA price − Main Auction price) × capacity

= (70,000 − 35,000) × 30,000 kW = JPY 1,050 million

→ Tier 2 amount = 1,050M − 150M = JPY 900 million

→ Refund = 900M × 90% = JPY 810 million

→ Retained = 900M × 10% = JPY 90 million

Tier 3 amount = 500M − 1,050M = 0 (within Tier 2 in this scenario)

Total refund = 142.5 + 810 = JPY 952.5 million

Total market retained = 7.5 + 90 = JPY 97.5 million

Annual Revenue Summary

Fixed income (①): JPY 2,100 million

Market income retained (②): JPY 97.5 million

Total: JPY 2,197.5 million/year

Key takeaway: Of the JPY 500 million in market revenue, only JPY 97.5 million (approximately 19.5%) is retained. However, the JPY 2,100 million fixed income provides a stable, predictable revenue base. KPMG analysis suggests that LTDA projects achieve an IRR of approximately 3.2% from capacity payments alone — a "bond-like return" — but the stable DSCR profile significantly improves project finance bankability.

5. Operator Rights

Successful LTDA bidders are granted the following rights.

5-1. Right to Receive Capacity Assurance Contract Payments

The right to receive annual payments from OCCTO equal to the contract price × installed capacity, for 20 years, with CPI-based annual adjustments.

5-2. Right to Operate Freely in Other Markets

Operators may freely participate in the JEPX, balancing market, non-fossil certificate market, and other markets. Revenue from these markets is subject to the tiered refund obligation, but participation itself is unrestricted.

5-3. Right to Apply for Equipment Modifications

During the supply provision period, operators may apply to OCCTO for approval of equipment modifications or upgrades where operationally necessary.

5-4. Right to Participate in Release Auctions

If supply capacity becomes surplus due to changes in demand conditions, operators may return a portion of their contracted capacity through a release auction.

6. Operator Obligations

6-1. Supply Provision Obligation

Operators must commence supply provision within four years of winning the auction and must reliably deliver the contracted capacity during the actual supply year.

6-2. Capacity Verification Test Compliance

Operators must respond to OCCTO's capacity verification tests (kW confirmation) and demonstrate the contracted capacity. Shortfalls identified in verification tests may result in penalties.

6-3. Market Revenue Refund Obligation

Operators must return the applicable portion of other-market revenue to OCCTO under the three-tier rules. Refunds are settled on an annual basis.

6-4. Capacity Factor Requirement Compliance

From Round 3 (FY2025 bidding) onward, operators must achieve annual capacity factors appropriate for their power source type. Specific thresholds for battery storage are still under discussion, but this introduces a new compliance risk — particularly for weather-dependent sources.

6-5. Reporting and Disclosure Obligations

Operators are required to submit regular reports to OCCTO covering generation performance, market revenue, and other operational data.

7. Round 3 Changes and Future Outlook

Round 3 (FY2025 bidding) introduced several significant changes affecting revenue calculation.

| Parameter |

Rounds 1–2 |

Round 3 (FY2025) |

| WACC cap (Business Return Rate) |

5% uniform across all sources |

Differentiated by lead time: 4%/5%/6% |

| Battery storage WACC |

5% |

4% (4-year lead time) |

| Minimum operating duration (batteries) |

3 hours or more |

6 hours or more (3–6h tier abolished) |

| LiB procurement cap |

Effectively ~1 GW |

0.4 GW (significantly reduced) |

| Price ceiling |

JPY 100,000/kW/year |

JPY 200,000/kW/year |

| Cell manufacturing country restriction |

None |

Specific-country dependency ≤ 30% |

Looking ahead, METI announced in June 2025 that it is considering a reform to the refund rules from Round 4 onward — introducing a mechanism that allows operators to retain more market revenue as a reward for operational excellence, rather than applying a uniform refund rate.

8. Summary — LTDA as a "Fixed-Cost Guarantee with Capped Upside"

The LTDA revenue structure can be summarized as: guarantee full fixed-cost recovery in exchange for substantially limiting market upside.

- Fixed income (capacity assurance contract amount) is retained 100%, forming the bankability foundation

- Market revenue is limited to 5–15% operator retention under the three-tier refund rules

- From Round 3, higher barriers apply: lower WACC, 6-hour duration requirement, reduced LiB quota

- Round 4 refund rule reform is under consideration — monitor policy developments closely

Glossary links: LTDA | Capacity Assurance Contract Amount | Business Return Amount | Refund Deduction | Capacity Market

References