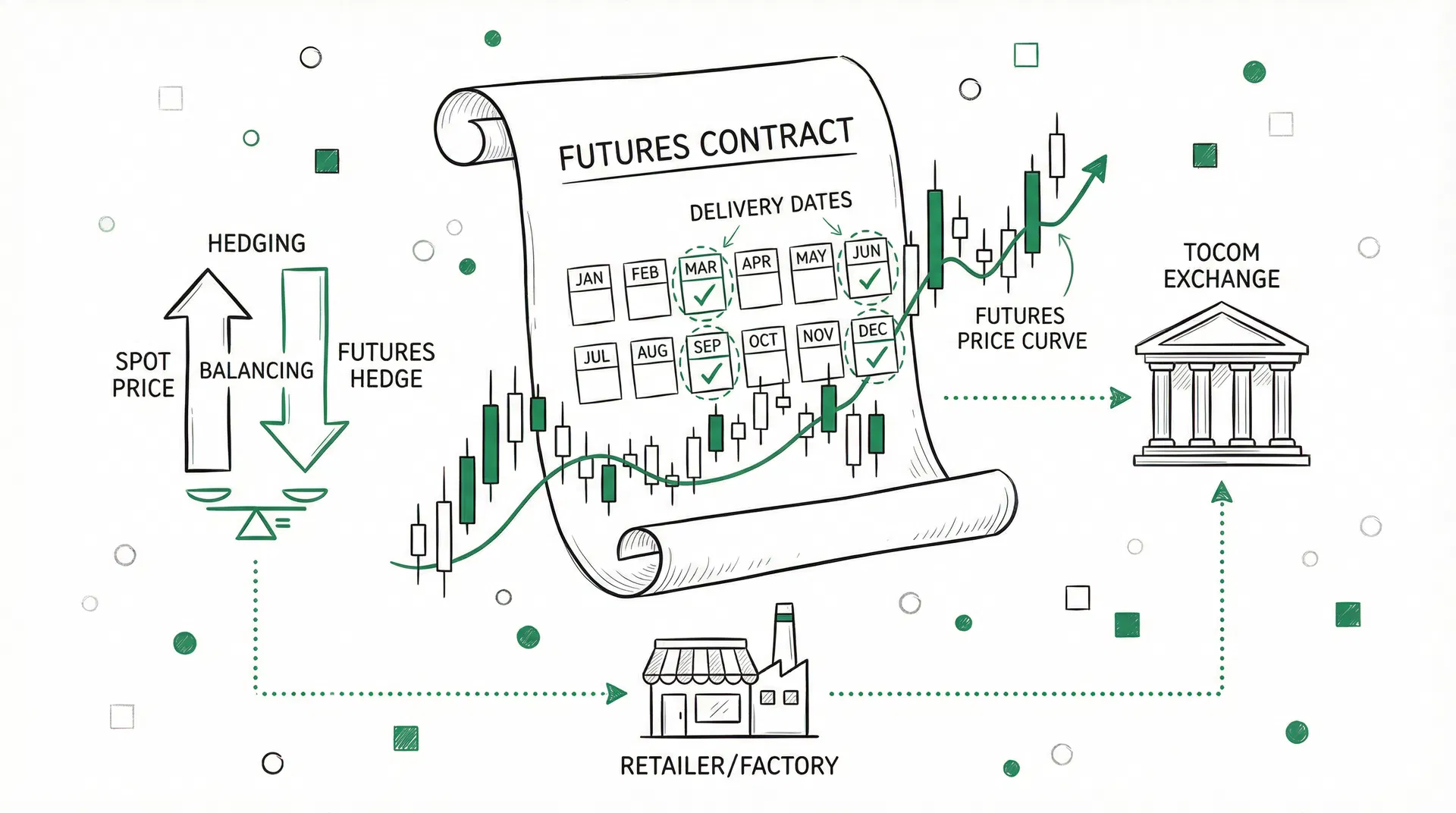

What Is the Electricity Futures Market?

Japan's electricity futures market is built on two complementary platforms. Tokyo Commodity Exchange (TOCOM) launched electricity futures in 2019, while JEPX introduced OTC forward clearing services in 2020. Together, they give Japanese electricity market participants tools for long-term price locking and risk hedging.

[KEY DATA]

As of March 2026, TOCOM electricity futures average monthly open interest stands at approximately 8,000 contracts (1 contract = 1,000 kWh × 24 hours × delivery month days), with a notional value of roughly ¥20 billion per month.

TOCOM Electricity Futures Contract Specifications

TOCOM electricity futures use the monthly baseload electricity of the Tokyo Electric Power (TEPCO) service area (East Area) as the underlying asset.

| Parameter | Specification |

|---|

| Underlying | TEPCO area monthly baseload electricity |

| Contract size | 1,000 kWh × 24 hours × delivery month days |

| Price quotation | ¥/kWh (2 decimal places) |

| Minimum tick | ¥0.01/kWh |

| Settlement | Cash settlement (based on JEPX monthly average System Price) |

| Listed months | Rolling 24 monthly contracts |

| Margin system | SPAN margin managed by JPX Clearing Corporation |

Since 2024, TOCOM has also listed Kansai Electric Power (KEPCO) area (West Area) futures, enabling participants to hedge East–West regional price spread risk.

The Futures–Spot Price Relationship

Electricity futures prices and JEPX spot prices are closely linked through arbitrage, but they do not move in lockstep. Understanding this relationship is foundational to futures trading.

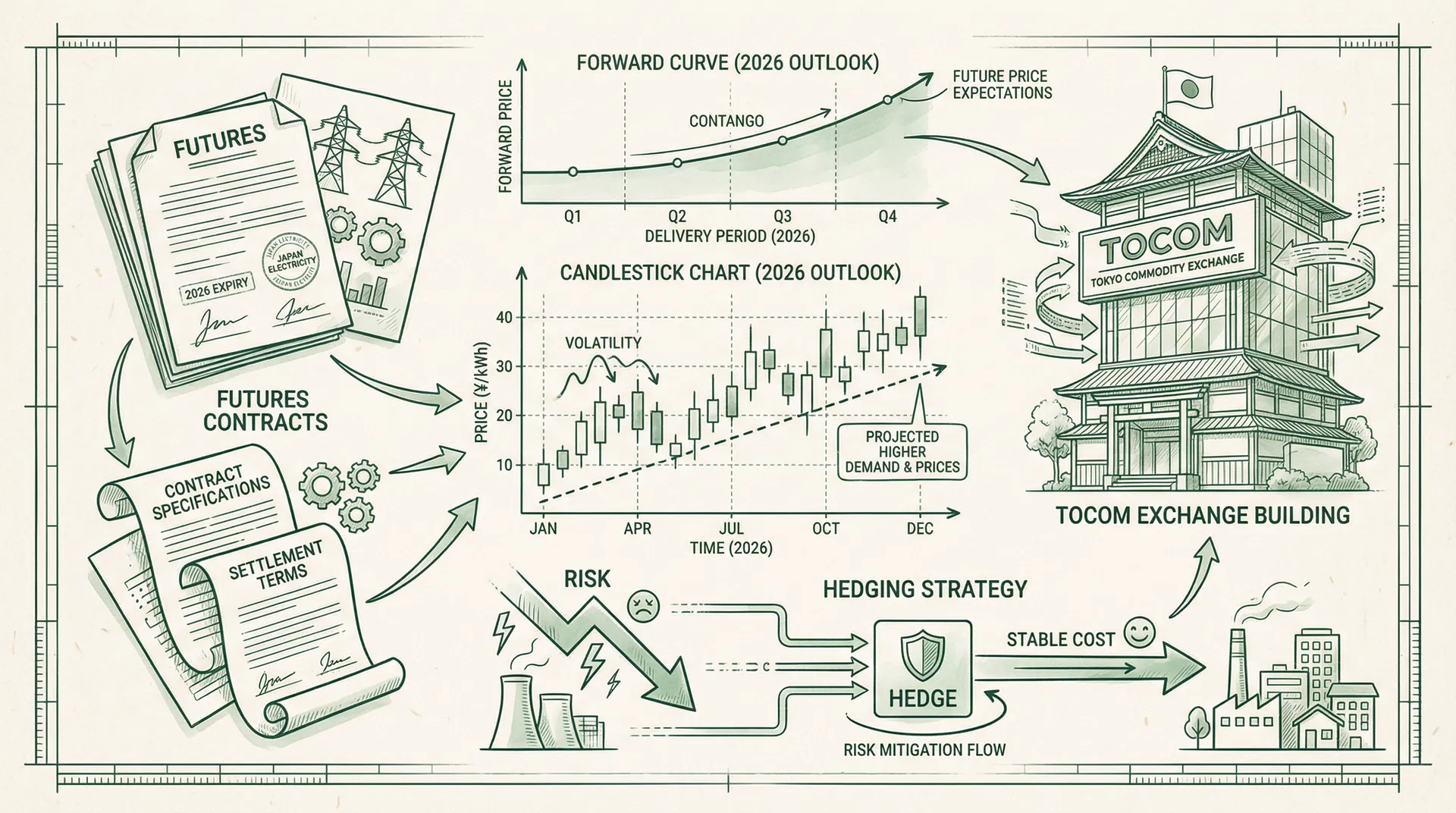

Contango and Backwardation

When futures prices exceed expected spot prices, the market is in contango — common for summer and winter peak contracts. When futures prices fall below expected spot prices, the market is in backwardation — often seen in spring contracts when renewable energy output is expected to be abundant.

The Basis Concept

Basis = Futures Price − Spot Price (JEPX System Price)

Basis fluctuations reflect market expectations about future supply and demand, liquidity premiums, and seasonal factors. For electricity retailers, managing basis risk is a critical component of any futures hedging strategy.

[Spring 2026 Market Observation]

The April 2026 futures contract settled at ¥11.2/kWh at end-March, while the actual April JEPX monthly average spot price came in at ¥9.8/kWh — a basis of +¥1.4/kWh, reflecting the market's overestimation of spring demand.

Hedging Strategies for Electricity Retailers

For retailers supplying electricity to households and businesses, the futures market offers three primary risk management approaches:

1. Full Hedge

The retailer charges customers a fixed electricity tariff while simultaneously buying an equivalent volume of TOCOM futures, locking in procurement costs at the futures price level. This eliminates spot price volatility risk but forgoes the benefit of lower spot prices if they fall sharply.

2. Partial Hedge

The retailer hedges only 50–70% of expected demand, retaining flexibility to procure the remainder on the spot market. This balances hedging costs against market opportunity and suits mid-sized retailers with some market judgment capability.

3. Dynamic Hedge (Delta Hedge)

As the delivery date approaches, the hedge ratio is dynamically adjusted based on updated demand forecasts and market conditions. This strategy requires strong quantitative analytical capability and is typically employed by large utilities or specialist trading desks.

Market Access Requirements

Participating in TOCOM electricity futures requires:

- TOCOM membership (or trading through a member broker)

- Registration with OCCTO (Organization for Cross-regional Coordination of Transmission Operators)

- Posting SPAN margin (calculated based on position size and market volatility)

Smaller retailers without TOCOM membership can access the market through OTC bilateral contracts with large utilities or financial institutions, then use JEPX's central clearing service to eliminate counterparty credit risk.

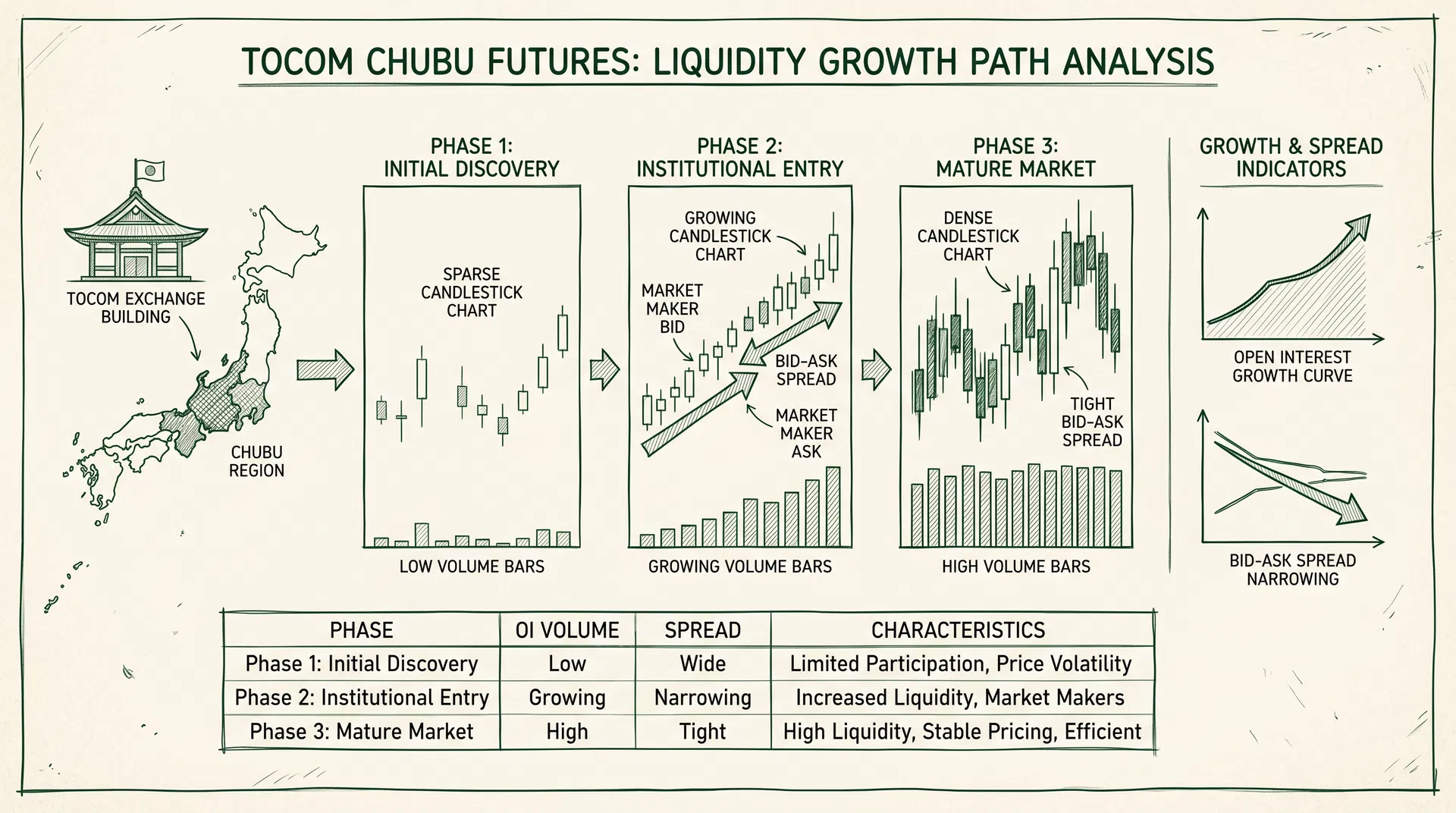

Liquidity Outlook

Compared to European power markets such as Nord Pool and EEX, Japan's electricity futures market remains relatively illiquid. Key reasons include the dominance of large utilities as market participants, limited hedging awareness among smaller retailers, and the ongoing development of spot market liquidity.

However, as Japan's full retail liberalization deepens and the 2026 retail tariff review cycle progresses, futures market participation is expected to grow steadily, with liquidity improving over the medium term.

"The electricity futures market is critical infrastructure for Japan's energy transition. Mastering futures hedging tools is the key capability that allows electricity retailers to maintain stable operations in a volatile market."