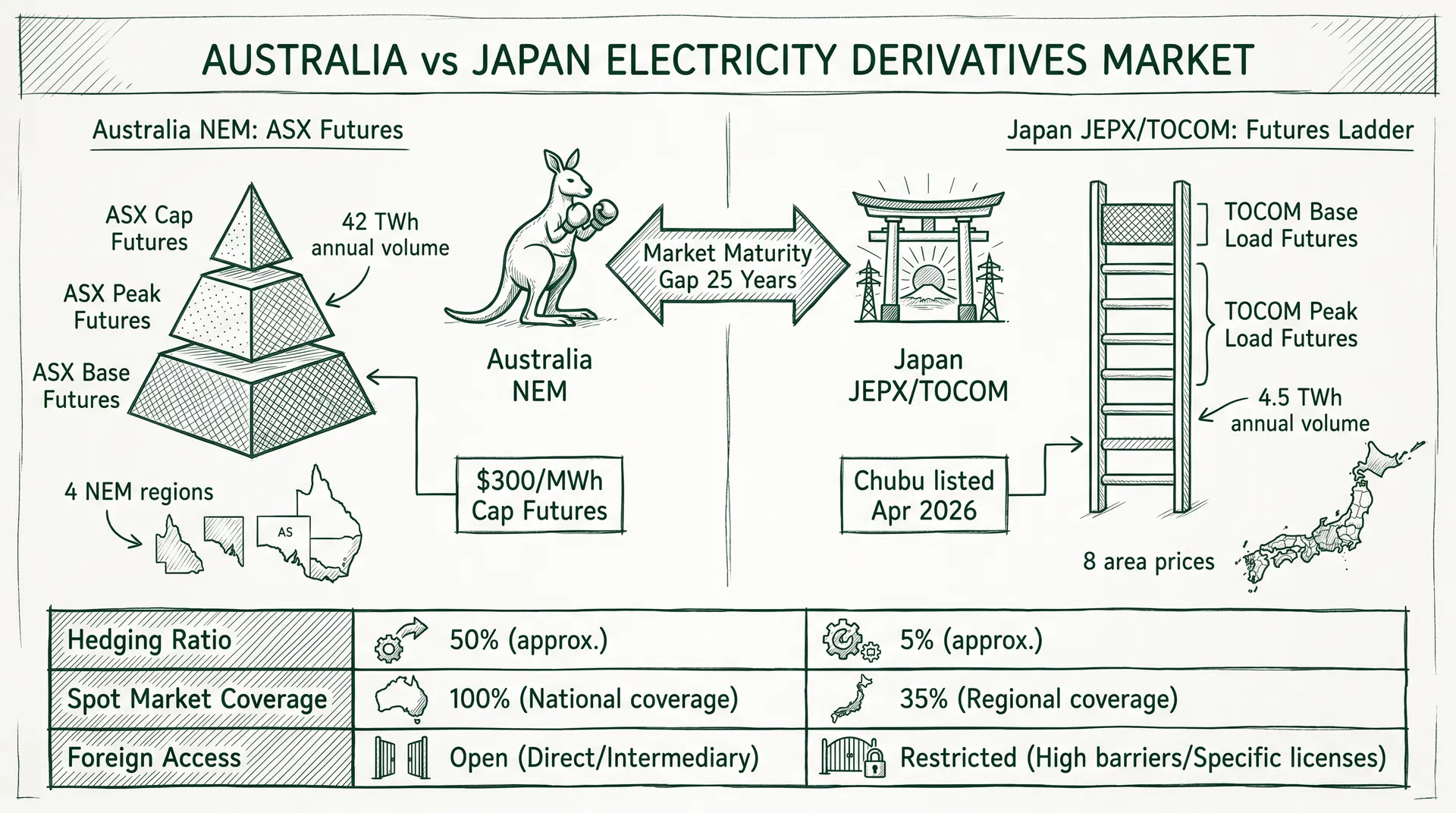

Introduction: Two Markets, a 25-Year Gap

In April 2026, the Tokyo Commodity Exchange (TOCOM) achieved a record annual trading volume for electricity futures, with FY2025 full-year volume reaching approximately 4,547 GWh (4.5 TWh), representing 2.2x year-on-year growth. This milestone energized market participants, but when compared to Australia's ASX Energy, the gap remains striking: ASX Energy's FY2024-2025 annual volume reached 422,383 contracts, equivalent to approximately 42 TWh—9 times TOCOM's volume.

This 9x gap is no accident. It reflects 25 years of divergent choices in electricity liberalization timelines, regulatory design, and liquidity ecosystem development. Understanding the root causes of this gap is essential for predicting the trajectory of Japan's derivatives market over the next decade.

Market Structure: The Ecosystem from Spot to Futures

Australia NEM: One of the World's Most Mature Electricity Derivatives Markets

Australia's National Electricity Market (NEM) officially launched in 1998, making it one of the earliest fully competitive electricity markets globally. The NEM covers Queensland (QLD), New South Wales (NSW), Victoria (VIC), South Australia (SA), and Tasmania (TAS), settling spot prices every 5 minutes across 8,760 trading intervals per year.

Building on this foundation, ASX Energy offers a rich suite of derivative products:

| Product Type |

Description |

Primary Use |

| Base Load Futures |

Quarterly/annual baseload futures |

Core hedging |

| Peak Load Futures |

Peak period futures (weekdays 7am-10pm) |

Peak risk management |

| Cap Futures |

$300/MWh cap futures |

Extreme price protection |

| Options |

Futures options |

Non-linear hedging |

| Morning/Evening Peak |

New products launched July 2025 |

Granular time-of-day management |

Cap Futures represent Australia's most distinctive market innovation. When spot prices exceed $300/MWh, Cap futures holders receive compensation for the excess—functioning as "flood insurance" for electricity procurement. As of May 1, 2026, NSW Cap Q2 2026 open interest stood at 4,627 contracts, VIC at 4,930, and QLD at 7,111, reflecting strong market demand for extreme price risk protection.

Japan JEPX/TOCOM: A Rapidly Growing Emerging Market

Japan's electricity spot market (JEPX) launched in 2005, but liquidity only improved significantly after the full retail liberalization in 2016. Currently, JEPX's spot market accounts for approximately 35% of Japan's total electricity consumption—far below Australia's 100%.

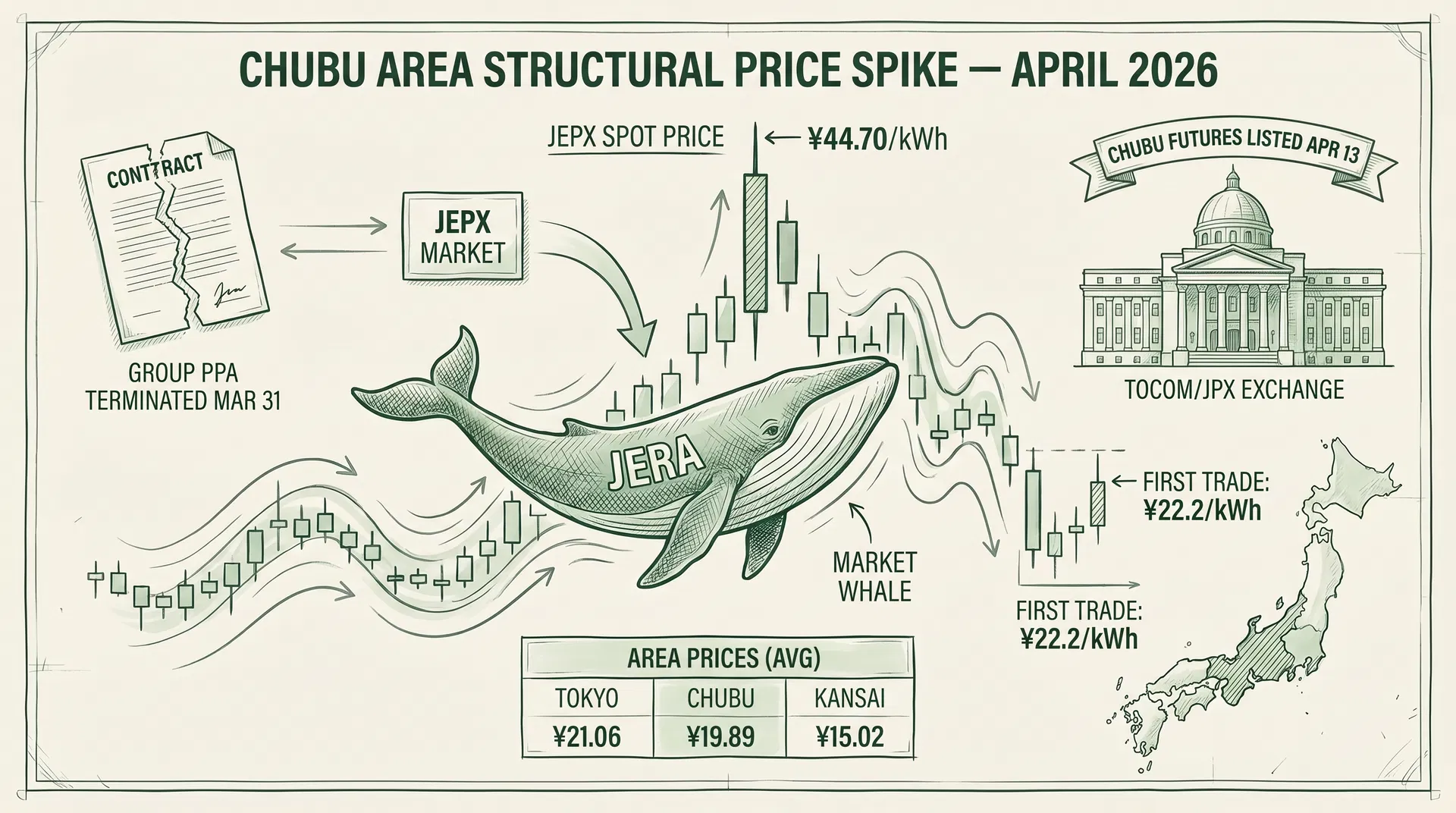

TOCOM electricity futures launched in 2019, offering monthly and annual contracts for the East Area (Eastern Japan) and West Area (Western Japan). In May 2025, fiscal-year contracts were added, significantly improving the convenience of corporate hedging. On April 13, 2026, Chubu Area electricity futures officially listed, marking Japan's electricity derivatives market advancing toward more granular regional pricing.

Liquidity Comparison: Dissecting the 9x Gap

| Metric |

Australia ASX (FY2024-25) |

Japan TOCOM (FY2024-25) |

Gap |

| Annual trading volume |

~42 TWh |

~4.5 TWh |

9.3x |

| Open interest (Base) |

NSW 16,805 contracts |

East Area ~2,000 (est.) |

~8x |

| Forward curve |

Through 2030 |

36 months (through 2028) |

— |

| Options market |

Active (NSW 21,398 OI) |

None |

— |

Electricity futures markets face a classic "chicken and egg" problem: low liquidity leads to wide bid-ask spreads, wide spreads increase transaction costs, high costs reduce participation, and fewer participants further reduce liquidity. Japan's TOCOM is in the early stages of this cycle, while Australia's ASX broke through it 25 years ago.

TOCOM has taken aggressive measures to break this cycle: a ~50% fee discount campaign launched in September 2025 (running through March 2027), and active expansion of the market maker network. FY2025 volume growing 2.2x year-on-year indicates these measures are beginning to take effect.

Cap Futures: Australia's Most Important Risk Management Tool

Cap futures are Australia's most distinctive feature and the hardest innovation for other markets to replicate. The design logic is as follows:

Australia's NEM employs a "price cap" mechanism where spot prices can reach up to $16,600/MWh, but electricity retailers holding sufficient Cap futures can lock their procurement cost ceiling at $300/MWh—effectively purchasing "flood insurance" for electricity. As of May 1, 2026, NSW Cap Q2 2026 closed at $16.68/MWh, VIC at $9.75/MWh, QLD at $6.70/MWh, and SA at $17.50/MWh. South Australia's high Cap premium reflects its high dependence on renewable energy and greater supply volatility.

Japan currently lacks a comparable Cap futures mechanism. JEPX spot prices have an administrative cap (¥50/kWh), but this is an "emergency brake" rather than a tradeable risk management tool. As Japan's electricity market volatility increases—evidenced by the December 2025 Hokkaido event and the April 2026 Chubu event—establishing a Cap futures-equivalent mechanism will become an important market development agenda item.

Regulatory Framework: Fundamental Differences in Institutional Design

Australia's Australian Energy Regulator (AER) introduced the Market Liquidity Obligation (MLO) in 2021, requiring large electricity retailers to provide a minimum number of bid-ask quotes in the ASX market, ensuring market liquidity. This institutional design fundamentally addresses the electricity futures market's "chicken and egg problem" by mandating that large participants become liquidity providers.

Japan currently has no mandatory hedging requirement equivalent to the MLO. The improvement of Japanese accounting standards in 2025—allowing hedge accounting for electricity futures—represents an important institutional breakthrough expected to attract more corporate treasury departments to the TOCOM market.

Foreign Access: Fundamental Differences in Openness

| Market Access Condition |

Australia ASX |

Japan TOCOM |

| Foreign direct participation |

Open, no special license required |

Requires Japanese PPS (electricity retail) license |

| Offshore institutional investors |

Can trade directly |

Must go through Japanese local intermediaries |

| Bank/fund participation |

Active (providing liquidity) |

Extremely limited (institutional barriers) |

| Market makers |

Multiple international banks |

Primarily Japanese local institutions |

ASX's openness has attracted numerous international financial institutions, bringing not only liquidity but also more sophisticated pricing models and risk management tools. For TOCOM to break through its liquidity bottleneck, opening foreign direct participation will be a critical step.

Japan's Catch-Up Path: Lessons from Australia's 25-Year Journey

Phase 1 (2026-2028): Building the Foundation

- Complete futures listing for all 8 electricity areas (Chubu completed April 2026)

- Promote hedge accounting adoption to attract corporate treasury departments

- Expand market maker network, reduce bid-ask spreads

- Target: Annual volume of 20 TWh

Phase 2 (2028-2032): Attracting Financial Institutions

- Research institutional framework for relaxing foreign direct participation

- Introduce options market

- Establish extreme price protection mechanism analogous to Cap futures

- Target: Annual volume of 100 TWh

Phase 3 (2032+): Mature Market

- Establish complete forward curve (3+ years)

- Attract international hedge funds and bank proprietary trading desks

- Achieve interconnection with global electricity derivatives markets

- Target: Annual volume of 500 TWh (~50% of Japan's total electricity consumption)

Conclusion

The gap between Australia and Japan's electricity derivatives markets is fundamentally a gap in institutional design, regulatory philosophy, and market openness. Australia spent 25 years building a mature, liquid, and diverse electricity derivatives ecosystem. Japan stands at the starting point of rapid development, with TOCOM's record FY2025 trading volume, the listing of Chubu Area futures, and improvements in hedge accounting all serving as positive signals.

For electricity market participants, understanding the differences between these two markets not only helps identify development opportunities in Japan's market but also provides new perspectives for cross-market arbitrage and risk management.