What Is the EPRX Supply-Demand Adjustment Market?

The Supply-Demand Adjustment Market (需給調整市場) is Japan's ancillary services market responsible for maintaining grid frequency stability and supply-demand balance. It is operated by the Electric Power Reserve Exchange (EPRX), a general incorporated association established in April 2021 as part of Japan's broader electricity market liberalization. The market was created to replace the traditional bilateral contract (随意契約) approach to procuring balancing capacity with a transparent, competitive market mechanism that ensures fair access for diverse resource types while reducing procurement costs.

Balancing capacity — the ability to rapidly increase or decrease output in response to system needs — is becoming increasingly critical as Japan expands its renewable energy penetration toward the national target of 36–38% by 2030. The variability of solar and wind generation creates new challenges for grid operators, making the efficient procurement of ancillary services a central concern for Japan's energy transition.

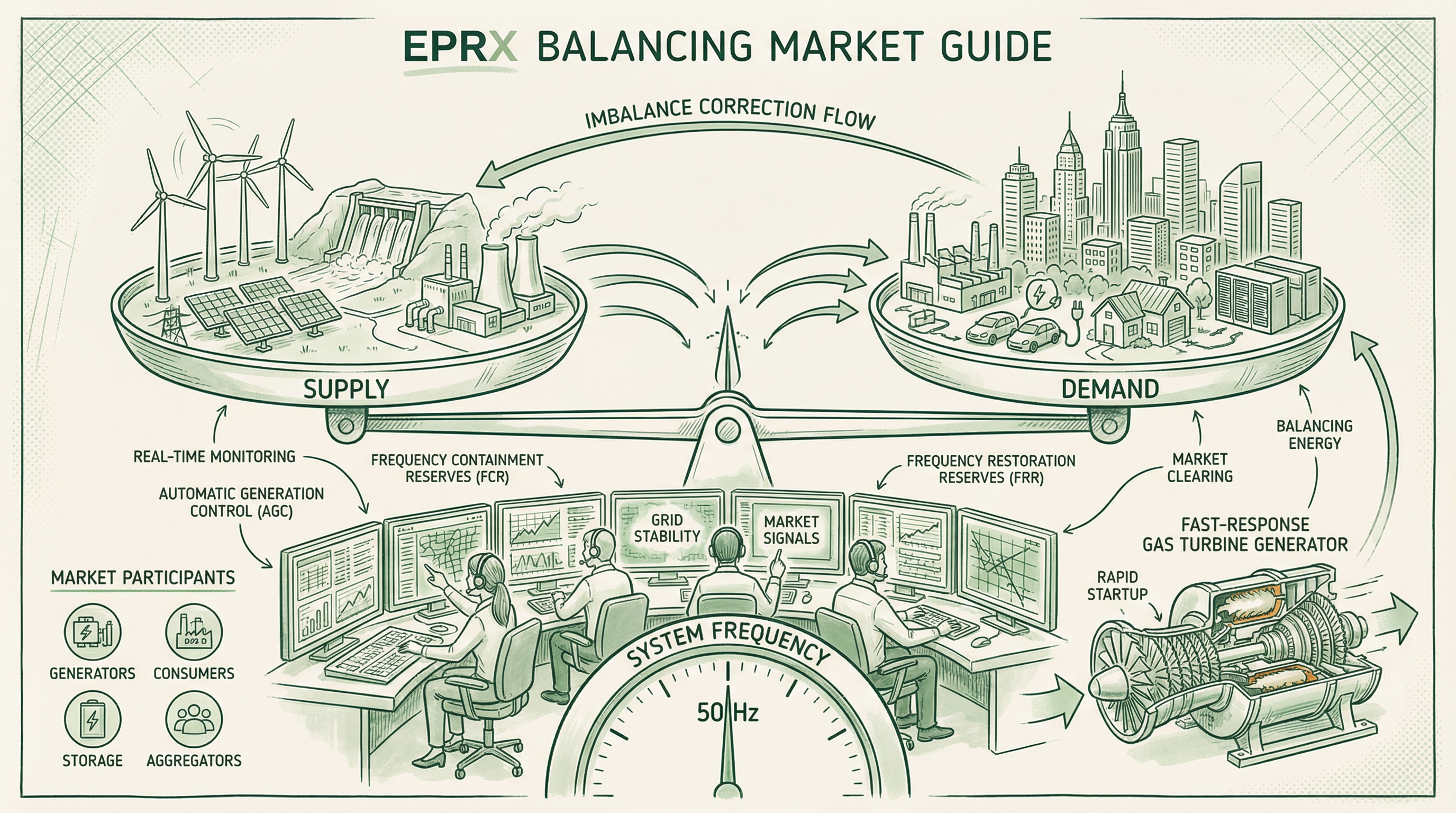

Market Participants

Any resource that meets the technical requirements of a given product category can register as a trading member and participate in the EPRX market. The participant base spans a wide range of technologies and business models.

| Participant Type | Representative Resources | Primary Products |

|---|

| Thermal power operators | Gas turbines, coal-fired plants | Tertiary-1, Tertiary-2 |

| Pumped hydro operators | Pumped-storage hydropower | All products |

| Battery storage operators | Large-scale lithium-ion BESS | All products (composite market) |

| Demand response providers | Industrial and commercial load control | Tertiary-1, Tertiary-2 |

| Aggregators | Bundled low-voltage resources | Tertiary-1, Tertiary-2 |

The Okinawa Electric Power service area is currently excluded from the EPRX market. Notably, a November 2025 revision to METI's Energy Resource Aggregation Business Guidelines formally opened the market to low-voltage resources (residential solar, electric vehicles) through aggregators, broadening the participation base significantly.

The Five Product Categories

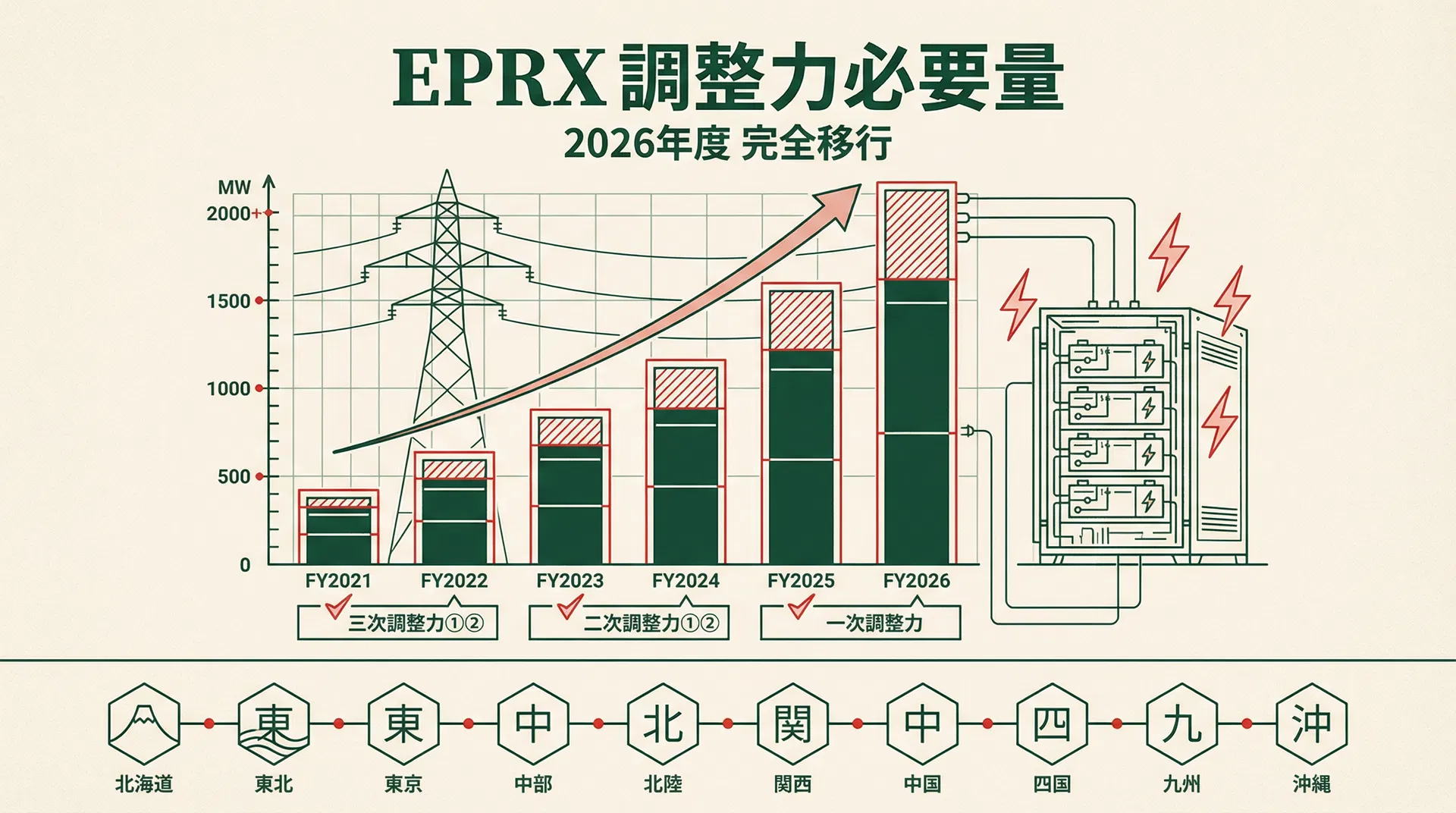

EPRX products are classified into five tiers based on response speed and the type of grid disturbance they address. The market was rolled out incrementally: Tertiary-2 launched in April 2021, Tertiary-1 in April 2022, and the three faster products (Primary, Secondary-1, Secondary-2) were added in April 2024, completing the full product suite.

| Product | Launch | Response Time | Duration | Addresses | Control Method |

|---|

| Primary (一次調整力) | Apr 2024 | ≤ 10 seconds | ≥ 5 min | Ultra-short-cycle fluctuations, sudden generation loss | Governor Free (GF) |

| Secondary-1 (二次調整力①) | Apr 2024 | ≤ 5 minutes | 30 min | Short-cycle fluctuations, generation loss | Load Frequency Control (LFC) |

| Secondary-2 (二次調整力②) | Apr 2024 | ≤ 5 minutes | 30 min | Long-cycle fluctuations (trend errors) | Economic Dispatch Control (EDC) |

| Tertiary-1 (三次調整力①) | Apr 2022 | ≤ 15 minutes | 30 min | Post-gate-close demand/renewable forecast errors, generation loss | Manual dispatch |

| Tertiary-2 (三次調整力②) | Apr 2021 | ≤ 60 minutes | 30 min | FIT renewable day-ahead forecast errors | Manual dispatch |

From a technical standpoint, the Primary product uses Governor Free (GF) control, where generators automatically adjust output upon detecting frequency deviations without requiring external commands — making it the fastest-responding tier. Secondary-1 operates via Load Frequency Control (LFC) signals received every few seconds to correct short-cycle frequency noise. Secondary-2 uses Economic Dispatch Control (EDC) signals at lower frequency to reload the Secondary-1 reserves consumed during dispatch. The Tertiary products are slower reserves dispatched manually to address larger-scale imbalances and replace secondary reserves.

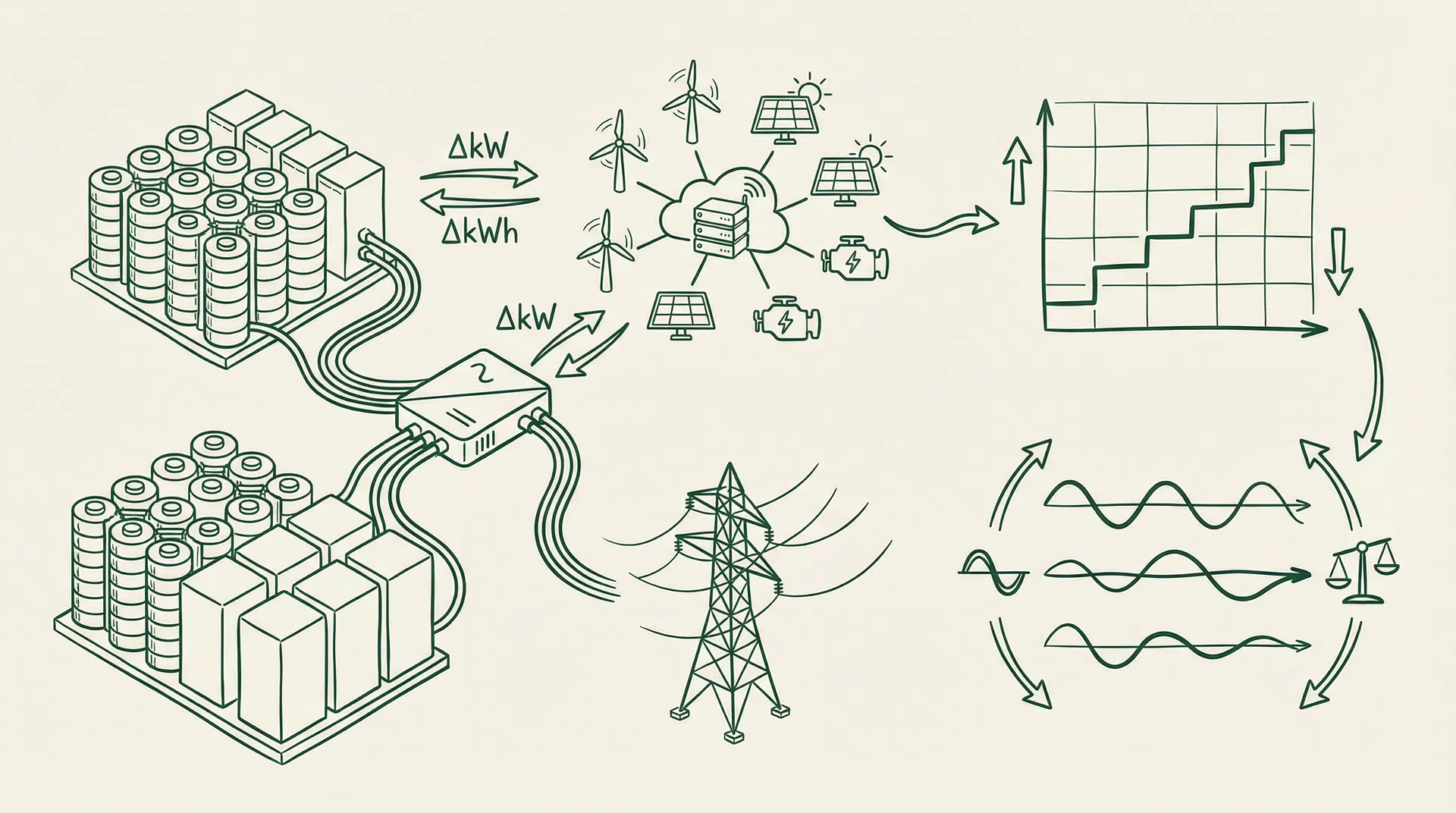

The ΔkW Bidding and Clearing Mechanism

The EPRX market operates on a capacity market design: the traded commodity is not electricity generation (kWh) but rather adjustment capacity (ΔkW, Delta Kilowatt) — the maximum output change a resource can provide upon receiving a dispatch signal. This represents a reservation of "standby capability" rather than a commitment to generate a specific quantity of electricity.

Each bid submitted to the EPRX market contains two pricing components. The ΔkW charge (capacity payment) is a fixed fee paid to resources for maintaining standby availability, regardless of whether they are actually dispatched — compensating for fixed costs such as capital and maintenance. The adjustment energy charge (energy payment) is a variable fee paid or charged when the transmission system operator issues an upward or downward dispatch signal and the resource actually responds, based on the quantity of energy delivered.

Clearing follows a price-priority principle: bids are accepted in ascending price order until the procurement volume (募集量) is satisfied. Bids at the same price are processed in random order to ensure fairness. Once cleared, the ΔkW charge is locked in for the entire contract period (one day for day-ahead products; formerly one week under the pre-March 2026 weekly product structure).

The Composite Market (複合市場) allows resources to bid simultaneously across multiple product categories. A battery storage system, for example, can submit a composite bid covering Primary, Secondary-1, and Secondary-2 simultaneously; the system automatically selects the optimal product combination to minimize total procurement costs for the transmission operator. For resources technically capable of meeting multiple product requirements — particularly battery storage — the composite market significantly expands revenue opportunities.

Trading Schedule

Tertiary-2 (day-ahead from inception): Since its launch in 2021, Tertiary-2 has operated as a day-ahead market. Because it addresses FIT renewable forecast errors that crystallize on the day before delivery, procuring this product the day before is operationally logical.

Primary through Tertiary-1 (formerly weekly products; transitioned to day-ahead March 2026): These four products originally used a weekly trading schedule. Bidding opened on the Monday before the delivery week (14:00) and closed Tuesday (14:00), with clearing completed by Tuesday 15:00. The contract covered Saturday through the following Friday — a seven-day window.

Day-ahead transition from March 13, 2026: Primary through Tertiary-1 products transitioned to day-ahead trading starting with the March 13, 2026 trade (delivery date March 14). This aligns procurement timing with spot market outcomes and next-day supply-demand forecasts, enabling more accurate and responsive balancing capacity procurement. The approximately one-week lag inherent in the weekly product structure — during which significant changes in the supply-demand environment could occur — has been eliminated.

The Role of Battery Energy Storage Systems (BESS) in EPRX

Battery Energy Storage Systems (BESS) have emerged as the fastest-growing resource category in Japan's EPRX balancing market. A 2022 amendment to the Electricity Business Act formally classified BESS facilities of 10 MW or more as "power generation businesses," enabling simultaneous participation in the JEPX spot market, the EPRX balancing market, and the capacity market — unlocking a multi-layered revenue stacking model that has attracted substantial investment interest.

When participating in EPRX at 1 MW or above, a BESS facility can adopt one of four participation modes depending on its grid connection configuration and operational design. The first mode is as a generation resource with reverse power flow to the grid. The second is as a demand response (DR) resource without reverse power flow, providing adjustment capacity through controlled charging. The third is as a component of an aggregated DR portfolio managed by a licensed aggregator. The fourth is a hybrid generation-DR mode that switches flexibly based on system conditions.

BESS assets are technically well-suited for the highest-value products — Primary (FCR) and Secondary-1 (S-FRR) — given their millisecond-level response times, which far exceed those of conventional thermal generators. In the composite market (composite clearing), batteries can simultaneously bid into multiple product categories, maximizing the utilization of their flexible capacity. Market data from fiscal year 2024 illustrates this advantage clearly: BESS assets in composite products achieved average clearing prices of JPY 15.70 per ΔkW/30min, compared to the all-resource average of JPY 5.77, reflecting the scarcity premium that fast-response battery storage commands in the high-value balancing products.

However, the revenue outlook for BESS in EPRX faces a significant structural challenge. METI has proposed reducing the price cap for Primary, Secondary-1, and composite products from JPY 19.51 to JPY 7.21 per ΔkW/30min (a reduction of approximately 63%) from fiscal year 2026, while simultaneously reducing procurement volumes to a 1σ standard. Together, these reforms will substantially compress balancing market revenues for battery storage, necessitating a fundamental reassessment of revenue stacking strategies — with greater emphasis on Long-Term Decarbonization Power Source Auction (LTDA) 20-year fixed contracts and JEPX spot market arbitrage.

Looking further ahead, from March 2026, low-voltage resources including residential batteries and electric vehicles will be eligible to participate in the balancing market through aggregators, provided device-level metering infrastructure is in place. This expansion broadens the market's resource base but also intensifies competition, particularly in the slower-response product categories.

Ichiji Offline Framework and Composite Product Clearing Mechanism

The Ichiji Offline Framework (一次オフライン枠)

The "ichiji offline" framework is a specialized participation pathway within the Primary adjustment product market, designed for small-scale or technically constrained resources that cannot receive real-time online dispatch signals. Standard Primary product participation requires resources to respond to automated online control signals, but three categories of resources are exempt from this requirement and may participate through the offline framework.

| Category | Eligibility Condition |

|---|

| Aggregated small generators | Aggregation of generators each below 1 MW |

| Medium-scale battery storage | BESS of 1 MW or above but below 10 MW, connected at extra-high voltage (some 22 kV) or high voltage |

| Demand-side load facilities | Customer load facilities where all on-site generation meets prescribed fuel/technology criteria (LNG, hydro, BESS, geothermal, nuclear, solar, wind, etc.) |

The bidding procedure for the offline framework is identical to standard Primary product participation; the only difference lies in the dispatch signal reception method. By creating this pathway, EPRX enables medium-scale batteries and demand-side resources that would otherwise be excluded by technical constraints to contribute to the fastest frequency regulation service, enhancing the diversity and resilience of the market's resource base.

Composite Product (複合商品) Clearing Mechanism

Composite clearing (複合約定) is one of EPRX's most distinctive institutional design features, allowing a single resource to bid simultaneously into multiple product categories. The theoretical foundation is the principle of "asynchronicity" (不等時性): the peak demand for each product category does not occur simultaneously, meaning the same resource can provide different adjustment services at different times without physical conflict.

The mechanics of composite bidding work as follows. A resource first selects the product category for which it has the largest available bid volume as its "primary product" and submits a full bid for that product. For all other eligible product categories, the resource then submits full bids using the primary product's capacity as the ceiling — these are treated as "subsets" (内数) of the primary bid. For example, a 100 MW battery storage system that selects Secondary-1 as its primary product can simultaneously bid 100 MW as a subset into both the Primary product and the Tertiary-1 product.

The price clearing mechanism for composite products operates as follows:

| Parameter | Detail |

|---|

| Price cap (current) | JPY 19.51 per ΔkW/30min (Primary through Secondary-1 and composite products) |

| Price cap (post-FY2026 reform) | JPY 7.21 per ΔkW/30min (unified across all products except Tertiary-2) |

| Clearing method | Marginal price clearing (pay-as-cleared) |

| ΔkW settlement calculation | ΔkW clearing price × ΔkW cleared volume × number of 30-minute slots |

| Adjustment energy payment | Separately settled at the adjustment energy unit price when dispatch is actually activated |

The strategic significance of composite clearing for BESS operators lies in its ability to dramatically improve capacity utilization efficiency: the same physical asset can secure clearing in multiple product categories simultaneously, multiplying revenue per unit of installed capacity. However, the FY2026 price cap unification reform will eliminate the premium previously accorded to high-cap products (Primary and Secondary-1), narrowing the revenue advantage of composite bidding and requiring operators to develop more sophisticated, data-driven bidding strategies to maintain competitiveness.

Bilateral Contracts (相対契約) and Their Market Impact

The second half of 2025 brought a significant institutional development to Japan's electricity market: transmission system operators (TSOs) were authorized under specific conditions to procure adjustment capacity through "bilateral contracts" (相対契約, also referred to as 随意契約), bypassing the competitive bidding mechanism of the EPRX market. This change represents a meaningful departure from the market-based procurement model that has been the cornerstone of EPRX since its establishment in 2021.

The rationale for introducing bilateral contracts stems from the recognition that competitive market procurement alone cannot always guarantee stable supply of certain specialized adjustment capacity types. Pumped hydro storage is the paradigmatic case: pumped hydro facilities possess large-capacity, long-duration adjustment capabilities that are indispensable for grid stability, but their cost structure differs fundamentally from thermal generators or battery storage, creating challenges for competitive market participation.

Chubu Electric Power (中部電力) represents a prominent example of the bilateral contract framework in practice. Chubu Electric operates multiple large-scale pumped hydro facilities within its service territory, assets that have historically served as the backbone of system balancing in the Chubu region. Under the bilateral contract framework, Chubu Electric's pumped hydro resources can enter into direct adjustment capacity procurement agreements with Chubu Electric Power Grid (the transmission subsidiary), outside the EPRX market mechanism. This arrangement ensures the availability of these strategically critical resources while providing greater revenue predictability for the facility operator.

The market impact of bilateral contracts is inherently two-sided. On the positive side, the framework secures stable supply of specific strategic resources — particularly large pumped hydro — and reduces system operational risk. On the negative side, shifting a portion of adjustment capacity procurement from the open market to bilateral agreements reduces EPRX market liquidity and competitive intensity, potentially impairing the market's price discovery function. For other market participants such as battery storage operators, the expansion of bilateral contracting effectively reduces the volume of capacity available for competitive bidding, a factor that must be incorporated into long-term business planning and investment analysis.

Recent Market Trends and the 2026 Reforms

Following the April 2024 completion of the full product suite, the EPRX market encountered serious underbidding challenges. Multiple product categories saw procurement volumes go unmet, and day-ahead product (Tertiary-2) costs surged. This backdrop prompted METI and OCCTO to undertake intensive reform discussions through late 2025, resulting in three major structural changes taking effect in fiscal year 2026.

Reform 1: Universal Day-Ahead Transition

As described above, the shift of Primary through Tertiary-1 products to day-ahead trading eliminates the information lag of the weekly product structure. Procurement decisions can now be made with the benefit of the latest weather forecasts, renewable output predictions, and demand projections, improving both accuracy and market efficiency.

Reform 2: Procurement Volume Reduction (Unified 1σ Standard)

Under the current regime, Primary and Secondary-1 products are procured at up to 3σ (three standard deviations) of demand variability through the market, while Secondary-2 and Tertiary-1 are capped at 1σ. The reform proposal unifies all products at a maximum of 1σ, with the transmission operators' own reserve capacity (pumped hydro, etc.) filling the gap. This effectively shrinks the market size, reducing the revenue opportunities available to battery storage operators who have relied on the market for primary income.

Reform 3: Price Cap Reduction (Unified at JPY 7.21/ΔkW/30min)

The current price cap structure grants a premium to faster-response products: Primary, Secondary-1, and all composite products are capped at JPY 19.51/ΔkW/30min, while Secondary-2 and Tertiary-1 single products are capped at JPY 7.21/ΔkW/30min. The reform proposal unifies all products (Primary through Tertiary-1) at JPY 7.21/ΔkW/30min (approximately JPY 14.42/ΔkW/h), a reduction of approximately 63% for the premium products. Tertiary-2 retains no price cap.

The impact on battery storage economics is substantial. During FY2024, BESS assets in the composite market achieved average clearing prices of JPY 15.70/ΔkW/30min — far above the all-resource average of JPY 5.77. Even after mid-year procurement volume reductions, BESS units averaged JPY 10.84/ΔkW/30min in April 2025. The proposed cap unification would eliminate the scarcity premium that battery storage has relied upon, requiring a fundamental reassessment of project economics for both existing and planned BESS developments.

Strategic Implications for Battery Storage Operators

The triple reform of 2026 demands a strategic recalibration for battery storage operators in Japan. Revenue diversification is now essential: the era of relying primarily on high-value balancing market arbitrage is ending. Operators should actively evaluate combined revenue models spanning JEPX spot market arbitrage, the Long-Term Decarbonization Power Source Auction (LTDA) capacity contracts, and EPRX balancing market participation.

Composite market participation remains a key advantage for batteries capable of meeting multiple product requirements simultaneously. Even in a smaller market, composite bidding maximizes clearing opportunities. The day-ahead transition also rewards operators who invest in accurate next-day supply-demand forecasting and automated bidding systems — capabilities that will increasingly differentiate competitive participants.

Finally, operators should monitor METI's ongoing policy discussions closely. The reform documents explicitly note that price caps will be "reviewed as appropriate based on circumstances," suggesting the JPY 7.21 level is not necessarily permanent. The System Review Working Group remains the key venue for tracking these developments.

Conclusion

The EPRX supply-demand adjustment market is an indispensable pillar of Japan's electricity system transformation. The three-pronged 2026 reform — day-ahead transition, procurement volume reduction, and price cap harmonization — signals a policy shift from "secure balancing capacity at any cost" toward "balance efficiency with cost control." For battery storage operators, this represents both a challenge to existing business models and an opportunity to develop more sophisticated, diversified revenue strategies. As Japan advances toward its 2030 renewable energy targets, the EPRX market's role in enabling a stable, low-carbon grid will only grow in importance.