Why BTM Solar + BESS Now?

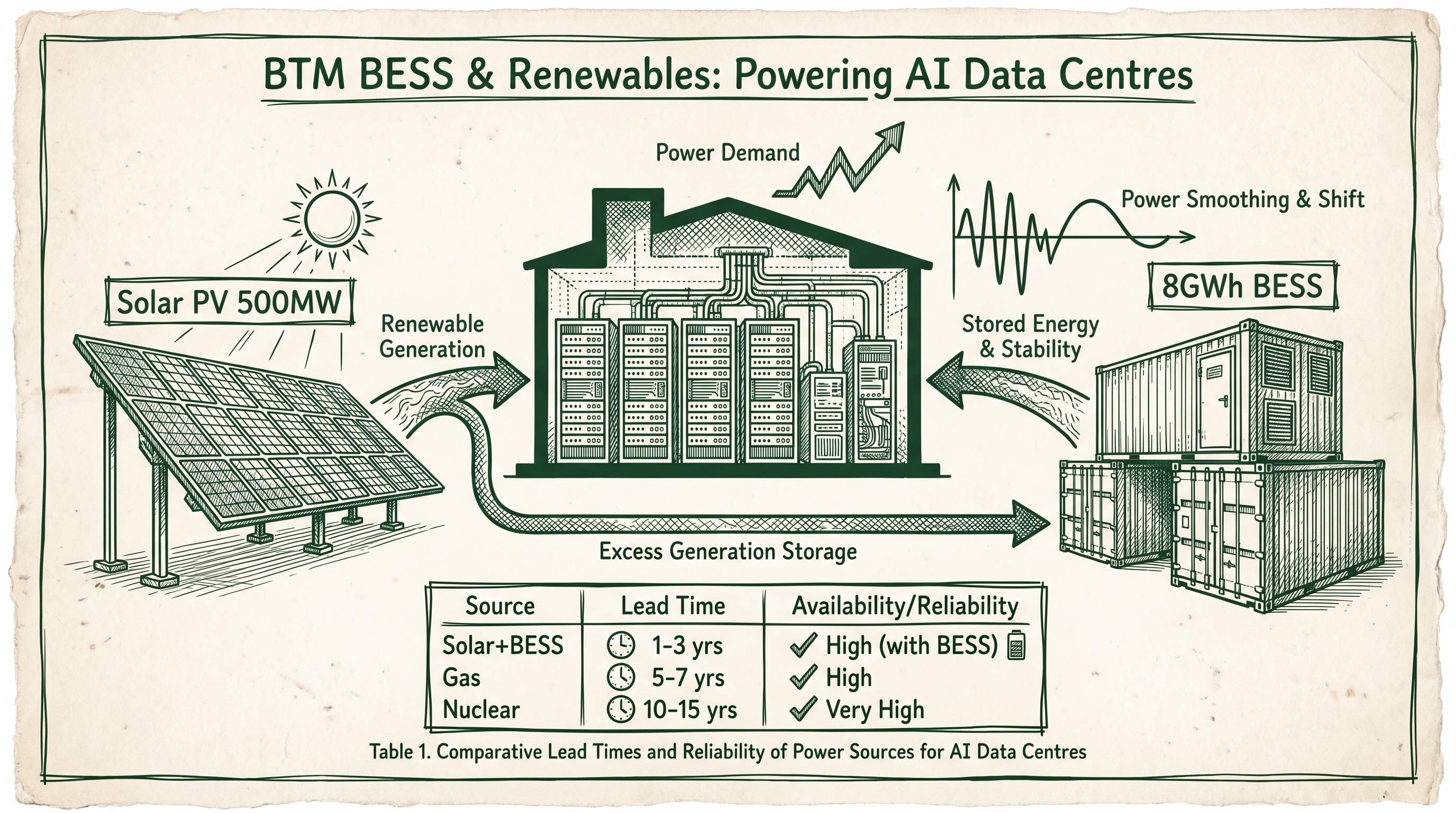

The Pantheon AI project in Croatia—500MW of solar paired with 8GWh of BESS to power a 1GW data centre—has demonstrated that hyperscalers are no longer willing to wait for grid connections. In Japan, this same imperative is becoming acute.

A METI working group report published in October 2025 confirmed that data centre applications in the Inzai-Shiroi corridor of Chiba Prefecture have already exceeded available grid capacity, with connection timelines stretching into years. NTT Global Data Centers has publicly cited waits of five to ten years for grid connection in the greater Tokyo area. Against a backdrop of USD 26 billion in announced hyperscaler investment from AWS, Oracle, and Microsoft, these delays represent an existential risk to project timelines.

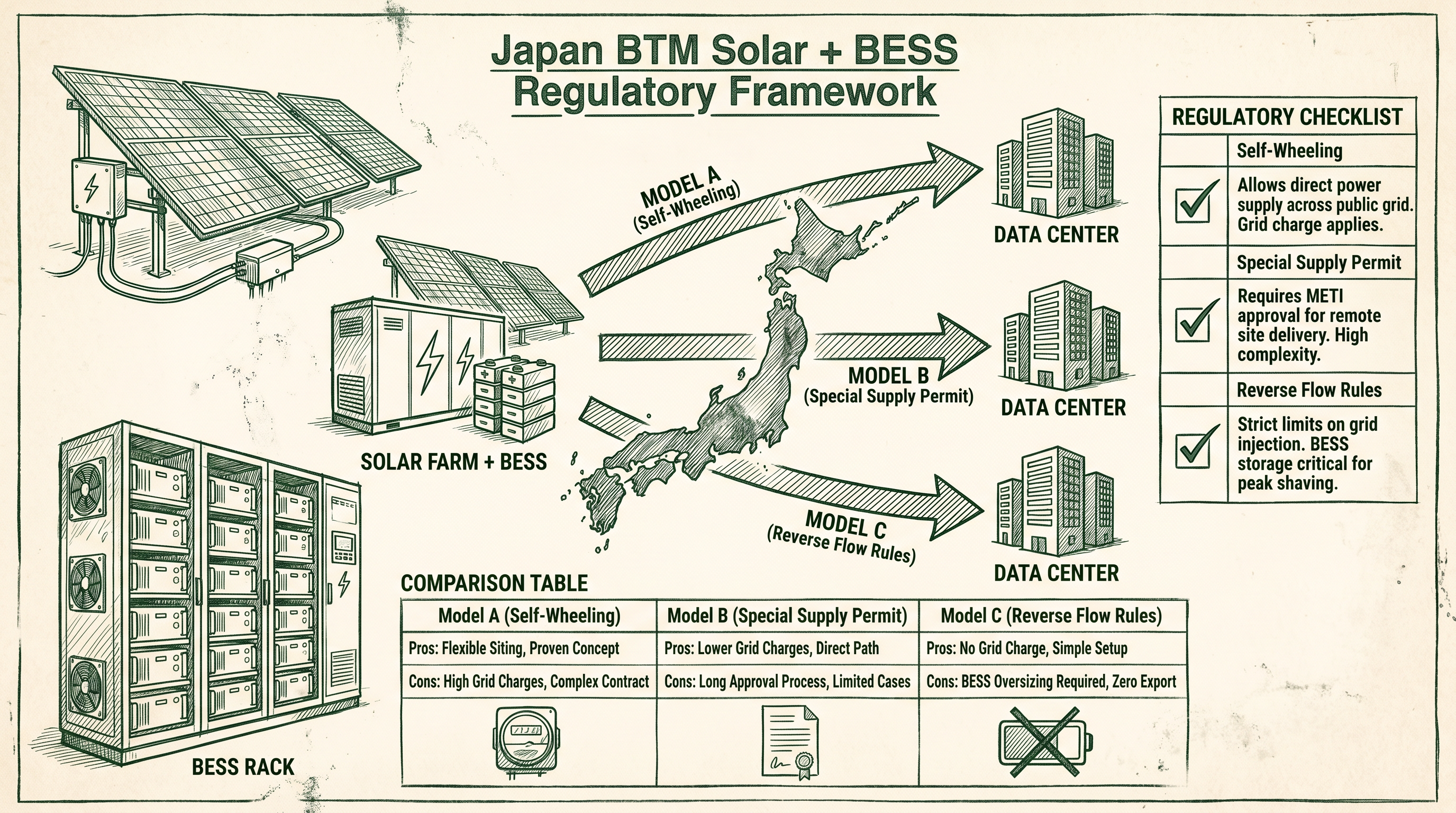

The BTM model—deploying solar and BESS behind the meter to serve data centre loads without relying on new grid connections—has emerged as the most credible near-term solution. But implementing BTM solar and BESS in Japan requires navigating three distinct regulatory frameworks under the Electricity Business Act: self-wheeling (自己託送), tokutei kyokyu special supply (特定供給), and reverse power flow rules (逆潮流規制).

Regulatory Pillar 1: Self-Wheeling (自己託送)

Self-wheeling allows a company to own a power plant at a remote location and deliver that electricity to its consumption site via the transmission and distribution grid. METI's Self-Wheeling Guidelines set out four cumulative requirements.

First, the generation equipment must qualify as non-electricity-business electrical equipment. Second, it must be self-installed and self-operated—not leased or transferred from a third party. Third, there must be a "close relationship" (密接な関係) between the generator operator and the consumption site. Fourth, the supply must serve the final electricity consumer's demand.

The "close relationship" criterion is the most consequential for data centre operators. It encompasses parent-subsidiary relationships as defined under company law, relationships where one party dispatches more than half of the other's directors, and relationships involving long-term continuous provision of materials or services. In practical terms, the parties must be regarded as a single enterprise under prevailing social norms.

The key financial advantage of self-wheeling is exemption from the renewable energy promotion surcharge, currently around 3.5 yen per kWh. However, the self-wheeling entity must assume imbalance risk, which is typically outsourced to a specialist forecasting service. A significant regulatory tightening in February 2024 also prohibited the supply of self-wheeled power to tenants of buildings owned by the self-wheeling company—a restriction that directly affects multi-tenant data centre operators.

Regulatory Pillar 2: Tokutei Kyokyu Special Supply (特定供給)

When self-wheeling extends to multiple consumption sites across a corporate group, the supply arrangement may be classified as tokutei kyokyu, requiring a permit from the Minister of Economy, Trade and Industry. Tokutei kyokyu is defined as electricity supply by a non-retail electricity business entity, conducted with ministerial permission.

Two categories of supply are exempt from tokutei kyokyu requirements: supply that does not constitute a "business" (such as a company consuming its own on-site solar generation), and supply to a single building or premises. For data centre groups operating multiple facilities, however, a group-level solar and BESS system supplying several DC buildings will typically require a tokutei kyokyu permit.

The permit application process requires demonstrating the "close relationship" between all supply and consumption parties, and accepted operators must fulfil ongoing reporting obligations. While this adds administrative burden, the permit unlocks the ability to supply multiple data centre buildings from a single large-scale BTM solar and BESS installation—maximising the economics of the investment.

The reverse power flow question is where BTM BESS deployments most frequently encounter regulatory misunderstanding. The critical distinction is between self-consumption and grid export.

When on-site BTM solar and BESS are used exclusively for self-consumption, no reverse power flow occurs. No retail electricity business registration is required, and the regulatory pathway is straightforward. This is the baseline BTM model.

When a BESS discharges electricity back into the grid—for example, to participate in the balancing market or sell surplus energy—that act constitutes electricity sales and requires either retail electricity business registration or notification as a power generation business. The PowerX × IIJ model, which envisions selling surplus BESS capacity to grid markets, is predicated on obtaining this registration.

METI's March 2026 announcement that FIT/FIP support for ground-mounted commercial solar will end from fiscal year 2027 is a significant tailwind for the BTM model. Solar and BESS systems designed for self-consumption are insulated from FIT/FIP policy risk, making them a structurally more stable long-term investment than grid-connected generation.

Three Supply Models: A Decision Framework

Drawing on the three regulatory pillars above, data centre operators can choose from three distinct supply architectures.

Model A: On-site BTM places solar panels on the data centre roof or car park, paired with BESS for peak shaving and backup. No special permits are required, and the renewable surcharge exemption applies. The constraint is roof area: most data centres can cover only 10–30% of their power demand through on-site solar alone.

Model B: Off-site Self-Wheeling involves the data centre company owning a remote solar farm and delivering power to the DC via the grid. The renewable surcharge exemption is retained, but wheeling charges of approximately 3–5 yen per kWh apply, and imbalance risk must be managed. Cross-area wheeling adds the complexity of indirect auction participation, introduced in October 2018.

Model C: Tokutei Kyokyu Group Supply allows a parent company to own a large solar and BESS installation and supply multiple DC subsidiaries or affiliates. This model offers the highest scalability but requires a ministerial permit and ongoing reporting. It is the appropriate architecture for large corporate groups operating multiple data centre facilities.

| Criterion |

Model A (On-site) |

Model B (Off-site Self-Wheeling) |

Model C (Tokutei Kyokyu) |

| Permit required |

None |

None (same area) |

METI minister's permit |

| Surcharge exemption |

Yes |

Yes |

Yes |

| Wheeling charges |

None |

~3–5 yen/kWh |

Applicable |

| Scalability |

Low (roof-constrained) |

Medium |

High |

| Imbalance risk |

None |

Yes |

Yes |

| Typical use case |

Single DC, initial deployment |

Single company, single area |

Corporate group, multiple sites |

Strategic Implications for Japan

The end of FIT/FIP for ground-mounted commercial solar from FY2027 is a structural accelerant for the BTM model. Self-consumption solar and BESS, decoupled from subsidy regimes, offer data centre operators a stable, policy-risk-free power source that simultaneously addresses the grid connection bottleneck and advances 24/7 Carbon-Free Energy commitments.

The practical first step for any data centre operator is to map its corporate structure against the three supply models: a single-entity operator will find Model A or B most accessible, while a corporate group operating multiple facilities should evaluate the tokutei kyokyu pathway. Early engagement with a solar and BESS development partner experienced in Japan's regulatory environment will be decisive in the Speed-to-Power competition that is already under way.

References

[1] METI FAQ on Self-Wheeling,

[2] Japan Energy Hub, "Self-Wheeling Guide",

[3] White & Case, "Japan Renewable Energy Update: Tightening Regulations for Solar Power" (April 2026),

[4] Data Center Dynamics, "PowerX, IIJ ink MoU to develop BESS-integrated containerized data centers in Japan" (February 2026),

[5] Introl, "Japan's $26 Billion Data Center Paradox" (January 2026)