1. Background: Why Was the LTDA Introduced?

Japan's capacity market (main auction) ensures short-term supply reliability, but its annual cadence and price volatility cannot provide sufficient investment certainty for long-lead, capital-intensive power sources such as nuclear, offshore wind, and BESS. The 2022 eastern Japan power supply crunch — partly attributed to accelerating retirements of aging thermal plants — prompted the government to launch the Long-Term Decarbonization Power Source Auction (LTDA) in FY2023.

[Policy Positioning]

The LTDA is the third tier of Japan's supply adequacy framework: Short-term (OCCTO emergency procurement) → Medium-term (Capacity Market Main Auction, 4 years ahead) → Long-term (LTDA, 20-year capacity assurance contracts). The three tiers complement each other to maintain system reliability.

2. System Design: Eligibility and Auction Format

The LTDA is administered by OCCTO and uses a pay-as-bid (multi-price) auction format — each winner receives the price they bid, unlike the uniform clearing price of the main capacity auction. Eligible resources fall into three broad categories:

| Category | Power Source Type | Key Requirements |

|---|

| Decarbonized Power Sources (Round 1: 4 GW target, Round 2: 5 GW) | Solar PV (new/replacement) | Cannot simultaneously receive FIT/FIP support |

| Onshore/Offshore Wind (new/replacement) | Cannot simultaneously receive FIT/FIP support |

| BESS / Pumped Hydro (new/replacement) | Round 2: split into 3–6 hour and 6+ hour discharge categories |

| Geothermal (new/replacement) | Minimum capacity 10 MW |

| Hydro – Regulated (new/replacement) | Minimum capacity 10 MW |

| Nuclear (new/replacement) | Must pass safety review |

| Biomass – Dedicated (new/replacement) | Full dedicated fuel by FY2050 |

| Existing Thermal Retrofit (Round 1 cap: 1 GW) | Hydrogen/Ammonia co-firing retrofit | Must submit decarbonization roadmap |

| CCS retrofit | Must achieve annual minimum CO₂ storage rate |

| LNG New-Build (Time-Limited Category) | LNG-fired (new/replacement) | Round 1: 6 GW over 3 years; decarbonization roadmap required |

| Existing Nuclear Safety Investment | Added in Round 2; cap 1.5 GW |

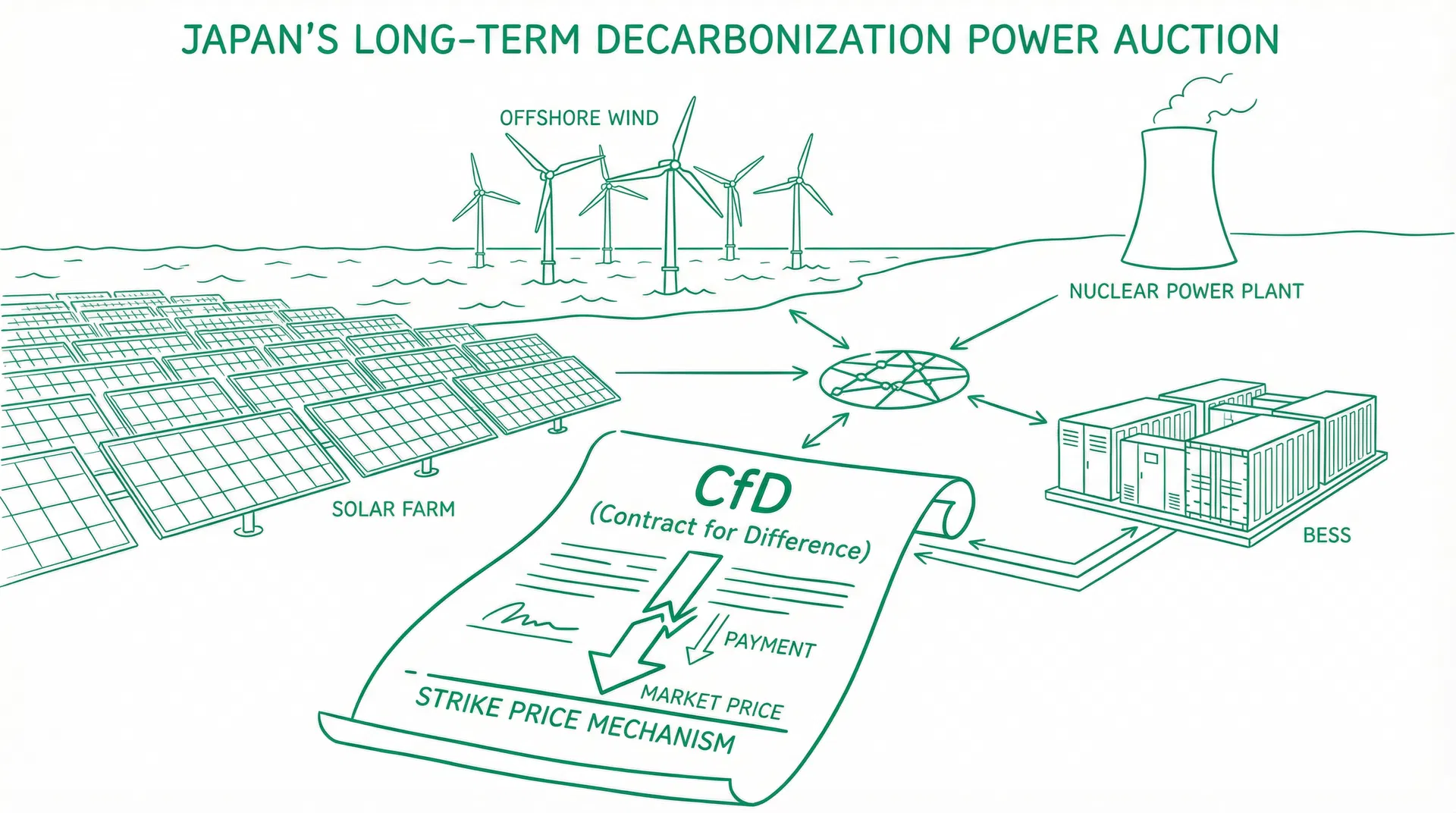

3. CfD Settlement Mechanism

The core financial design of the LTDA is a Contracts for Difference (CfD) capacity assurance scheme, ensuring winners can recover fixed costs over 20 years while preventing windfall profits.

3.1 Capacity Assurance Contract Payments

After winning, OCCTO signs a capacity assurance contract with the operator. Each fiscal year, OCCTO pays the capacity provider monthly:

Capacity Assurance Payment = Contract Unit Price (¥/kW/year) × Contract Capacity (kW)

This revenue represents the fixed-cost-level capacity income — paid regardless of market electricity prices, ensuring investment recovery certainty.

3.2 Market Revenue Clawback (Three-Tier Structure)

Once operational, the contracted power source must return approximately 90% of market revenues (revenue from JEPX spot, balancing market, non-fossil value market, minus variable costs) to OCCTO under a three-tier structure:

| Clawback Zone | Clawback Rate | Description |

|---|

| Zone (A): Market revenue ≤ capital cost equivalent | 95% | Ensures operator retains minimum capital cost return |

| Zone (C): Capital cost < Market revenue ≤ Main auction price × contract capacity | 90% | Standard clawback zone |

| Zone (B): Market revenue > Main auction price × contract capacity | 85% | Reduced clawback on excess revenue to incentivize efficient operation |

[Design Logic]

The three-tier clawback prevents double-dipping (receiving capacity payments while also profiting from high electricity prices). However, retaining 5–15% of market revenues preserves the operator's incentive to generate during high-price periods. Negative market revenues in any year are carried forward and netted against future revenues.

4. Historical Auction Results

4.1 Round 1 (FY2023 Bidding Year, Results Announced: April 2024)

| Category | Target Capacity | Awarded Capacity | Total Contract Value (annual avg.) |

|---|

| Decarbonized Power Sources | 4.0 GW | 4.01 GW | ¥233.6 bn/year |

| └ BESS / Pumped Hydro | Cap 1.0 GW | 1.67 GW | (included above) |

| └ Existing Thermal Retrofit | Cap 1.0 GW | 0.83 GW | (included above) |

| LNG New-Build | 6.0 GW (3-year total) | 5.76 GW | ¥176.6 bn/year |

| National Total | — | 9.77 GW | ¥410.2 bn/year |

Round 1 saw total national bids of 13.56 GW with a 72% award rate. By technology: pumped hydro award rate 69% (0.84 GW bid), BESS award rate only 24% (4.56 GW bid, highly competitive), LNG new-build 100% award rate. New-build/replacement accounted for 91% of awarded capacity.

4.2 Area Breakdown – Round 1

| Area | Bids (GW) | Awards (GW) | Award Rate |

|---|

| Hokkaido | 0.08 | 0.04 | 49% |

| Tohoku | 1.04 | 0.72 | 70% |

| Tokyo | 3.76 | 3.25 | 86% |

| Chubu | 1.88 | 1.56 | 83% |

| Kansai | 2.23 | 1.89 | 85% |

| Chugoku | 1.21 | 0.78 | 65% |

| Shikoku | 0.06 | 0.00 | 0% |

| National | 13.56 | 9.77 | 72% |

4.3 Round 2 (FY2024 Bidding Year, Results Announced: April 2025)

| Category | Target Capacity | Awarded Capacity | Total Contract Value (annual avg.) |

|---|

| Decarbonized Power Sources | 5.0 GW | 5.03 GW | ¥346.4 bn/year |

| └ BESS/Pumped Hydro (3–6 hr discharge) | — | 0.96 GW | (included above) |

| └ BESS/Pumped Hydro (6+ hr discharge) | — | 0.77 GW | (included above) |

| └ Existing Thermal Retrofit | — | 0.10 GW | (included above) |

| └ Existing Nuclear Safety Investment | Cap 1.5 GW | 3.15 GW | (included above) |

| └ Conventional Hydro (regulated) | — | 0.05 GW | (included above) |

| LNG New-Build | 2.24 GW | 1.32 GW | ¥45.6 bn/year |

| National Total | — | 6.35 GW | ¥392.0 bn/year |

Round 2 saw total national bids of 13.62 GW with only a 47% award rate (more competitive than Round 1). The headline result was the first inclusion of existing nuclear safety investment, with 3.15 GW awarded (4.35 GW bid, 73% award rate), reflecting Japan's nuclear restart policy. BESS bids surged to 6.96 GW (+53% vs. Round 1) but the award rate fell to 20%.

4.4 Round Comparison

| Metric | Round 1 (FY2023) | Round 2 (FY2024) |

|---|

| Decarbonized source target | 4.0 GW | 5.0 GW (+25%) |

| Total national awards | 9.77 GW (72% rate) | 6.35 GW (47% rate) |

| Decarbonized source contract value | ¥233.6 bn/year | ¥346.4 bn/year (+48%) |

| LNG new-build awards | 5.76 GW | 1.32 GW (sharply reduced) |

| BESS bids | 4.56 GW | 6.96 GW (+53%) |

| BESS award rate | 24% | 20% (more competitive) |

| New source category | — | Existing nuclear safety investment (3.15 GW) |

| BESS discharge duration split | Not differentiated | 3–6 hr / 6+ hr categories |

5. Capacity Levy Impact on Retail Suppliers

The LTDA capacity levy is calculated alongside the main auction levy, allocated to each area by H3 demand ratio, then distributed among retailers by their market share. Based on Round 2 results, the estimated FY2028 national LTDA capacity levy is approximately ¥69.3 billion/year (grid operators ¥5.4 bn + retailers ¥63.9 bn), on top of the main auction levy. As subsequent rounds add more contracted capacity, the LTDA share of total capacity levies is projected to rise significantly through the 2030s.

6. Strategic Implications for BESS and Renewable Investors

The LTDA provides critical revenue certainty for BESS investors. A 20-year fixed capacity assurance contract significantly de-risks financing, making project finance more accessible. However, since ~90% of market revenues must be returned, BESS business models must be built around the capacity assurance payment as the primary revenue stream, not market arbitrage.

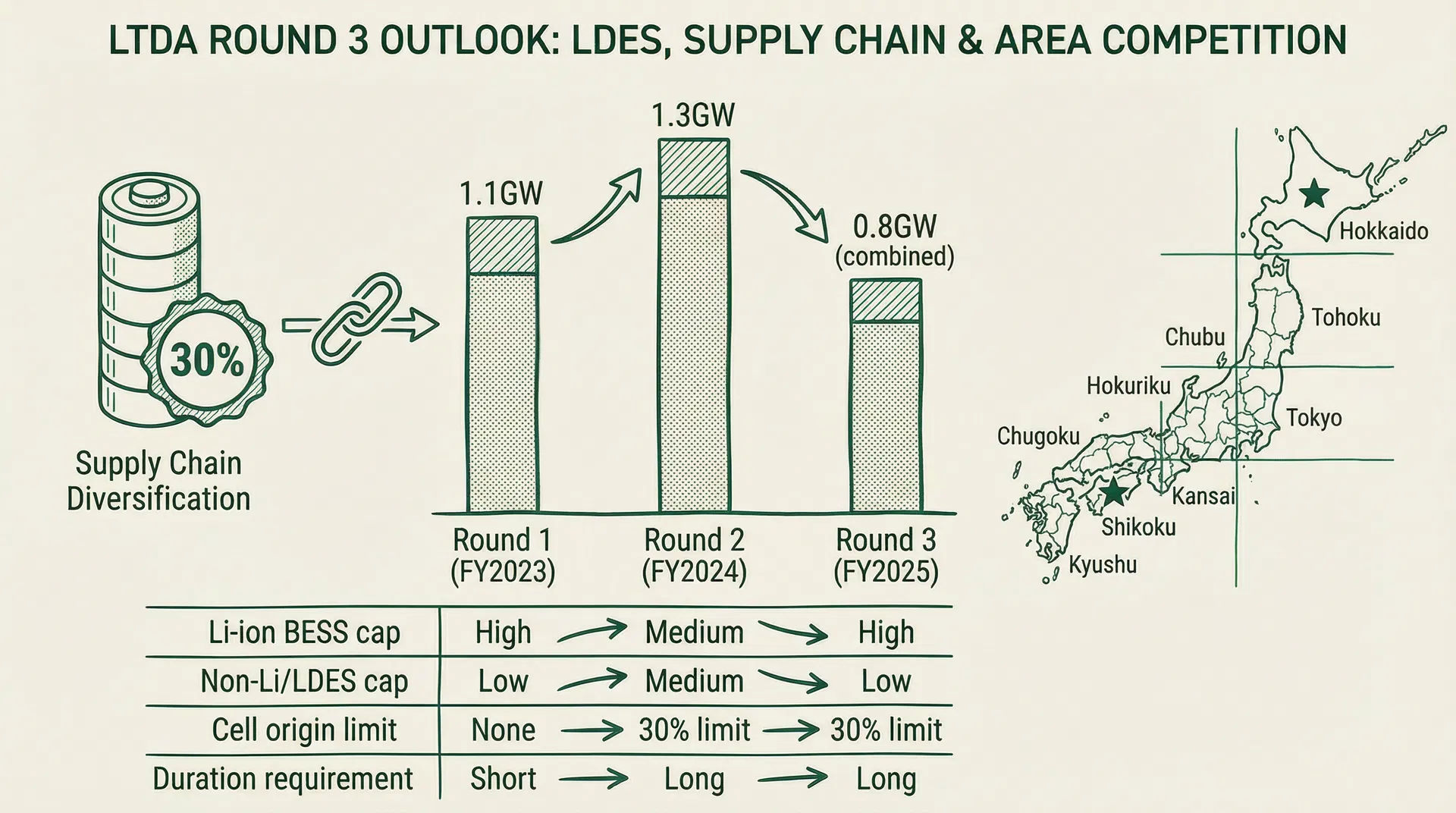

[Round 3 Key Changes (FY2025 Bidding Year)]

Round 3 introduces significant reforms: ① New Long-Duration Energy Storage (LDES) category for non-lithium BESS; ② Separate procurement caps for non-lithium BESS (liquid flow batteries, compressed air storage); ③ Cells manufactured in any single non-Japan country limited to 30% of total BESS awards (supply chain diversification); ④ Bid price cap threshold revised to ¥200,000/kW/year.

7. Controversies and Reform Outlook

The LTDA has faced criticism on several fronts. First, the inclusion of LNG new-build is seen as greenwashing — while decarbonization roadmaps are required, most plans do not achieve full decarbonization until the 2040s. Second, BESS award rates of 20–24% mean most storage investment plans cannot secure long-term revenue certainty, potentially slowing Japan's storage deployment. Third, the inclusion of existing nuclear safety investment has been controversial, with critics arguing it uses consumer funds to subsidize nuclear life extension rather than driving genuinely new low-carbon investment.

"The Long-Term Decarbonization Power Auction is a pivotal policy tool in Japan's power sector decarbonization, but its effectiveness ultimately depends on the competitive dynamics of each technology category and the rigor with which decarbonization roadmaps are enforced."