Introduction: Why This MoU Matters

On 13 February 2026, PowerX Inc. and Internet Initiative Japan (IIJ) signed a non-binding Memorandum of Understanding to jointly explore the development of containerised data centres integrated with battery energy storage systems (BESS). While the agreement is preliminary, its strategic significance extends well beyond a standard technology pilot.

The MoU represents the first major Japanese industry partnership explicitly designed to monetise BESS residual capacity from a data centre context. At its core, the partnership proposes a dual-revenue model: use integrated BESS to power data centre IT loads while simultaneously selling surplus stored energy to electricity markets during periods of high demand. This architecture, known as BTM (behind-the-meter) integration, offers a fundamentally different risk profile compared to standalone grid-scale BESS — and the timing could not be more strategic.

PowerX: The Vertically Integrated BESS Manufacturer

PowerX operates a vertically integrated business model spanning BESS manufacturing, sales, and operation. Its Okayama factory delivered Japan's first commercial grid-scale BESS unit in December 2025 — a 2,742 kWh system in a 20-foot ISO container using lithium iron phosphate (LFP) chemistry. The company's aggregation arm, PowerX Energy, centrally manages both its own and third-party BESS assets across three Japanese electricity markets: the JEPX spot market, the capacity market, and the EPRX balancing market.

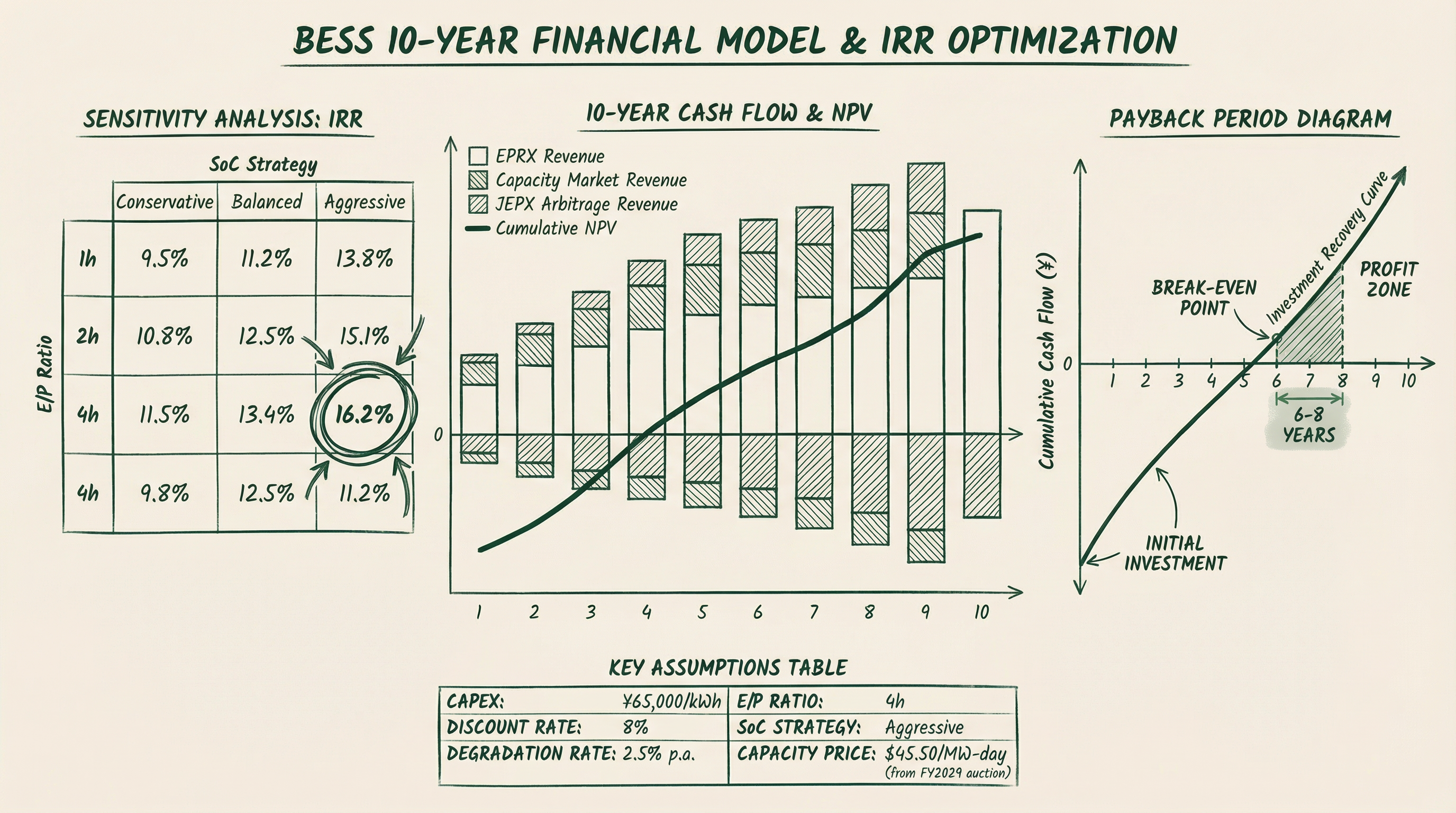

PowerX Energy offers two revenue strategies. The tolling model provides stable, infrastructure-like returns at approximately 4% IRR through fixed-fee arrangements. The merchant model captures market upside by participating in spot arbitrage, capacity auctions, and balancing market provision, targeting 4–10% IRR depending on market conditions.

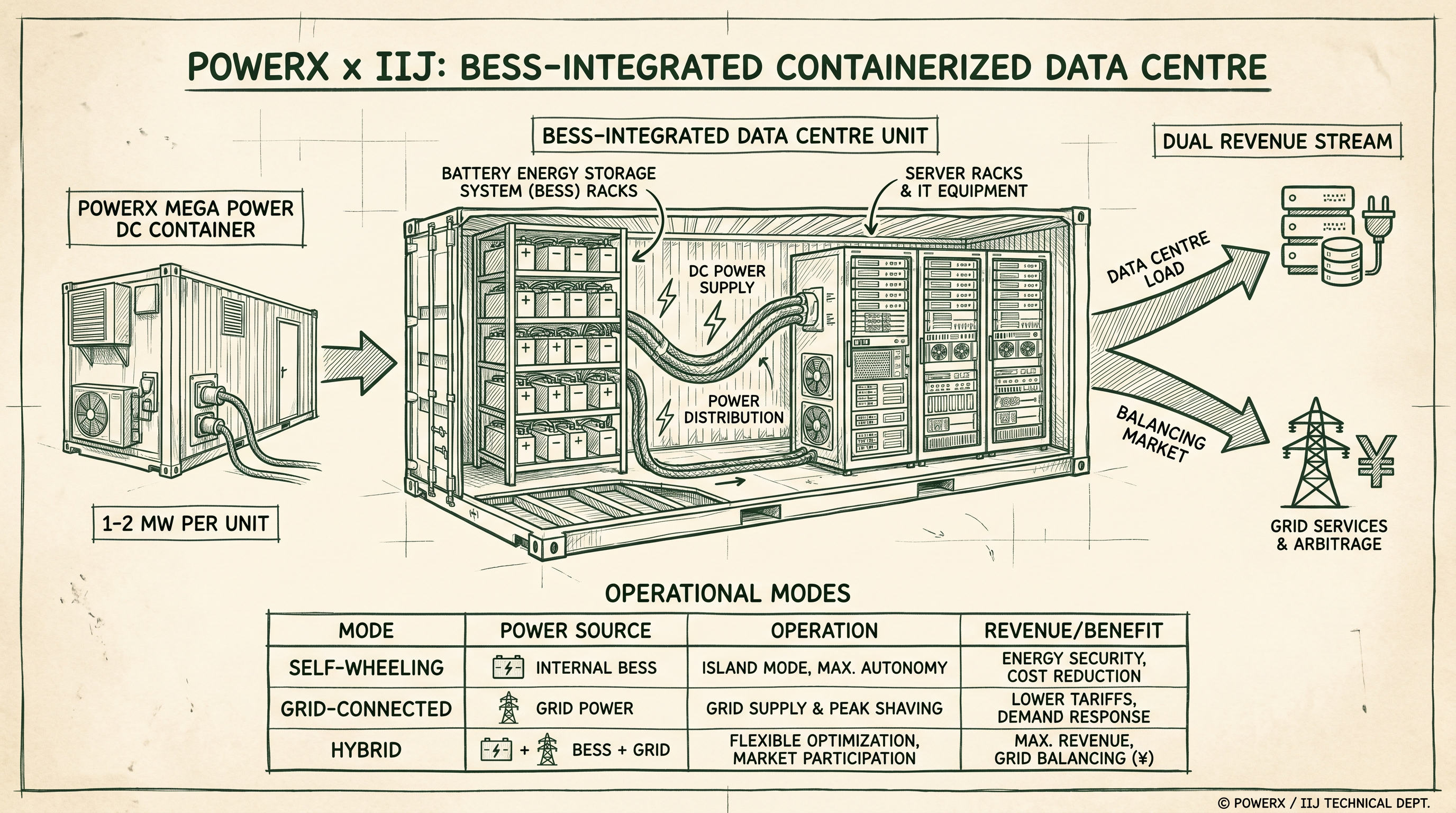

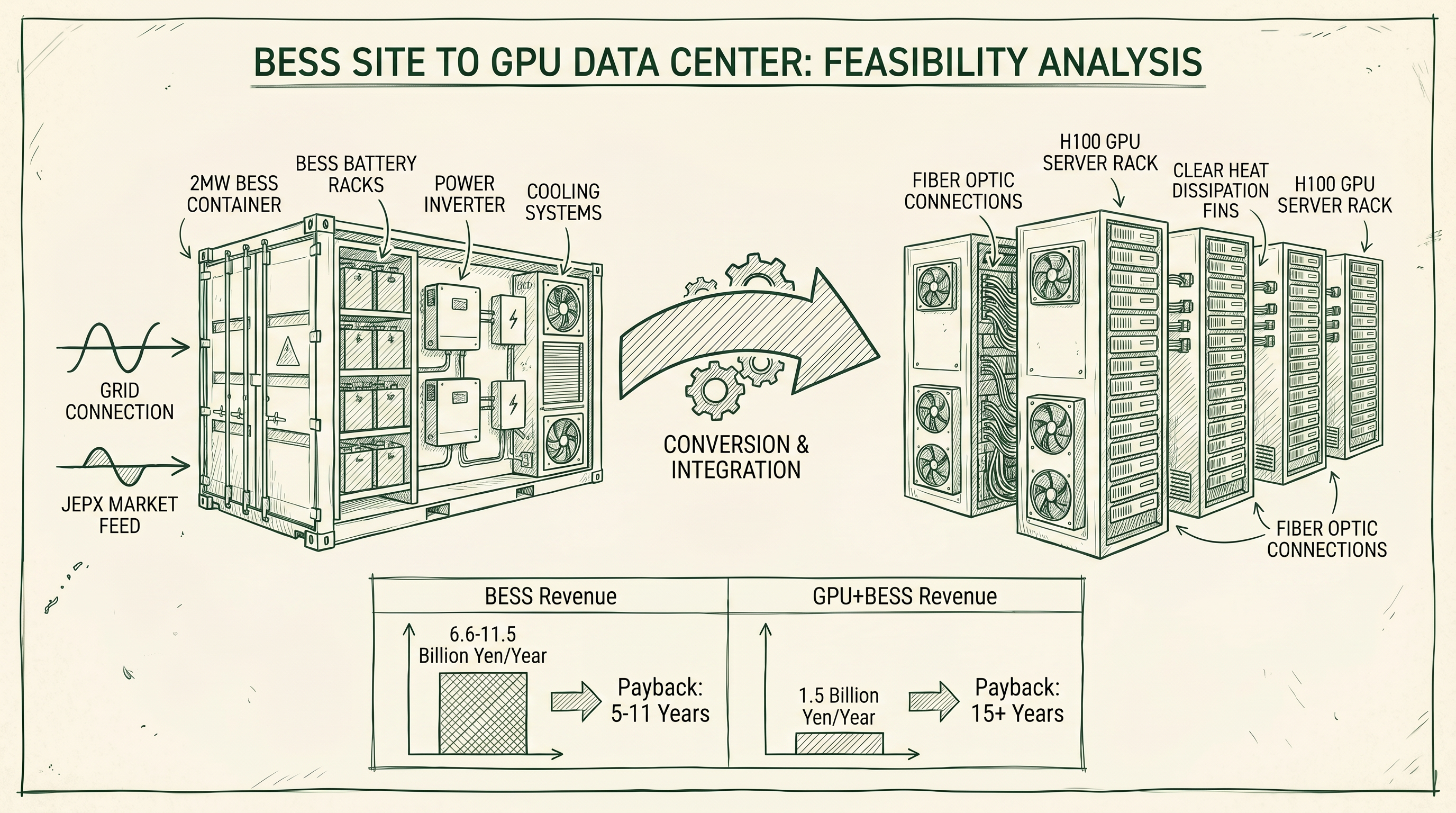

The "Mega Power DC" product, announced alongside the MoU, applies this BESS expertise to data centre infrastructure. Built on a 10-foot ISO High-Cube container, each unit integrates 4–6 industry-standard 42U racks with an optional 800 kWh BESS module, a proprietary closed-loop liquid cooling system capable of up to 150 kW per rack, and a DC-first power architecture that minimises conversion losses. Against conventional building-type data centres, Mega Power DC claims approximately 25% lower CapEx and a deployment timeline of roughly one year versus four to five years. Mass production at the Okayama factory is scheduled to begin in 2027.

IIJ: Japan's Container Data Centre Pioneer

Founded in 1992, IIJ is one of Japan's largest internet service providers and has operated a container-based data centre in Matsue City, Shimane Prefecture since 2011 — making it one of the earliest adopters of containerised DC infrastructure in Japan. The company currently operates approximately 17 locations domestically and five internationally, and has separately partnered with ZellaDC on containerised data centre solutions.

IIJ's motivation for the MoU reflects a broader industry crisis. AI-driven demand has placed unprecedented pressure on power availability and grid connection timelines. In central Tokyo, grid interconnection queues have been reported to extend five to ten years in some cases, rendering conventional build-and-connect approaches inadequate for the pace of AI infrastructure deployment. IIJ's operational expertise in containerised facilities and technical requirements definition makes it a natural partner for PowerX's hardware-led approach.

Four Deployment Models for Mega Power DC

PowerX categorises Mega Power DC deployments across four configurations based on site context and power source:

| Deployment Model |

Scale |

Power Source |

Key Advantage |

| Hyperscale |

125+ units (50 MW) |

Adjacent large-scale source (thermal) |

~1 ha site, no grid connection required |

| Power plant co-location |

125 units (25 MW) |

Internal load of existing plant |

Minimal transmission loss, relocatable |

| Battery power plant integration |

1–10 units (0.2–2 MW) |

Solar + BESS |

Faster grid connection, energy arbitrage |

| Edge / on-site |

1 unit (0.2 MW) |

Existing site power |

Urban deployment, BCP backup |

The "battery power plant integration" model most closely mirrors the MoU's target use case: solar generation combined with BESS to supply data centre IT loads, with surplus capacity sold to electricity markets — what PowerX describes as simultaneous optimisation of "bits (compute) and watts (power)."

The Dual-Revenue Model: Structure and Mechanics

The commercial logic of the MoU rests on exploiting BESS capacity across two distinct revenue streams simultaneously.

Primary revenue: captive load supply and grid cost avoidance

By integrating BESS directly with data centre IT loads, operators can avoid grid interconnection costs (which can reach hundreds of millions to billions of yen), eliminate long connection queues, and reduce ongoing grid charges including the renewable energy surcharge (currently approximately ¥3.5/kWh). The DC-first power architecture further reduces conversion losses and improves PUE (Power Usage Effectiveness).

Secondary revenue: residual BESS capacity market sales

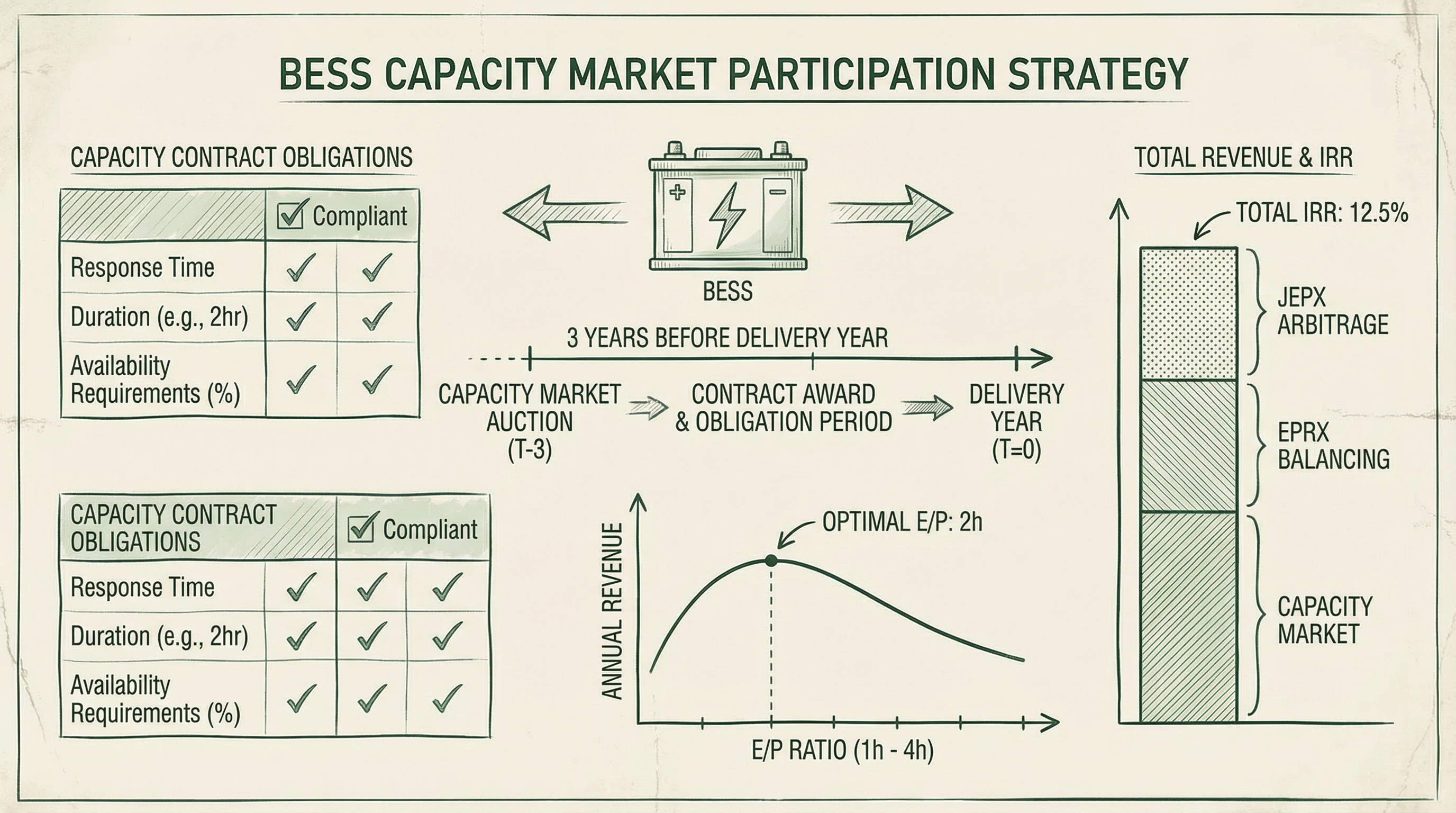

Data centre IT loads are not constant. During off-peak hours — nights, weekends, and low-utilisation periods — surplus BESS capacity can be directed to JEPX spot arbitrage (charge during low-price periods, discharge during high-price periods) or offered as fast-response capacity to the EPRX balancing market. PowerX Energy's aggregation service handles market participation on behalf of the operator.

| Revenue Stream |

Mechanism |

Market |

Estimated Return |

| Grid cost avoidance |

Interconnection & tariff savings |

Internal |

¥100M–¥1B+ (one-time) |

| Spot arbitrage |

Charge low / discharge high |

JEPX |

IRR 4–10% (merchant) |

| Balancing market |

Fast-response capacity provision |

EPRX |

¥7.21/ΔkW/30min (post-cap) |

| Capacity market |

Long-term decarbonisation auction |

LTDA |

Stable, infrastructure-like |

| Tolling |

Fixed fee to aggregator |

PowerX Energy |

IRR ~4% |

METI's Price Cap Reduction and Why BTM Wins

In October 2025, METI proposed reducing the price cap for premium balancing market products — Primary, Secondary-1, and composite — from ¥19.51 to ¥7.21 per ΔkW/30min effective April 2026, a reduction of approximately 63%. The proposal came in response to concerns that BESS bids had clustered at the price ceiling, driving up balancing costs.

The impact on standalone grid BESS economics is significant. During fiscal year 2024, BESS assets participating in composite balancing products achieved average settlement prices of ¥15.70 per ΔkW/30min — well above the proposed cap. Even after mid-year volume reductions, BESS units settled at an average of ¥10.84 per ΔkW/30min in April 2025. The cap effectively removes the scarcity premium that many BESS projects relied upon to offset degradation costs.

However, the BTM BESS plus data centre model is structurally insulated from this headwind. The data centre IT load provides a guaranteed primary revenue stream that does not depend on electricity market prices. Balancing market participation is additive upside, not the economic foundation. This is a fundamentally different risk profile from standalone grid BESS, where balancing market revenue is often the primary justification for investment.

As Greenberg Traurig's analysis observes, the price cap reduction is effectively incentivising BESS developers to reorient toward the capacity market (via LTDA), corporate PPAs, and BTM integration — precisely the direction the PowerX×IIJ MoU represents.

Implications for Japan's Electricity Market Participants

The business model emerging from this MoU carries strategic implications across multiple market segments.

Power generators and utilities can explore siting Mega Power DC units within existing plant premises, converting surplus generation into a captive data centre load. Combined with direct supply arrangements (特定供給), this creates a new revenue stream from existing assets while minimising transmission losses.

New power retailers can leverage PowerX Energy's aggregation service to access balancing and capacity markets without owning BESS assets. Pairing data centre supply contracts with PPA structures opens pathways to 24/7 carbon-free electricity (CFE) certification, increasingly demanded by hyperscaler tenants.

BESS developers facing revenue compression from the balancing market price cap can reframe their investment thesis around BTM integration with data centres, where a guaranteed captive load provides the economic foundation and market participation provides incremental upside.

Conclusion

The PowerX×IIJ MoU marks a strategic inflection point in Japan's data centre power landscape. If Mega Power DC reaches mass production as planned in 2027, BESS-integrated containerised data centres could become a standard option in Japan's AI infrastructure deployment toolkit.

The dual-revenue model — captive IT load supply plus residual BESS capacity market sales — offers a more resilient economic structure than standalone grid BESS, particularly in the context of METI's balancing market price cap reduction. For Japan's electricity market participants, this represents a structural shift that warrants serious strategic attention.

References

[1] DataCenter Dynamics, "PowerX, IIJ ink MoU to develop BESS-integrated containerized data centers in Japan" (13 February 2026)

[2] PowerX, "Mega Power DC" product page

[3] PowerX, "Aggregation Service — PowerX Energy"

[4] Greenberg Traurig, "METI Proposes Price Cap Reductions in Japan's Balancing Market: Implications for Battery Energy Storage Systems" (12 January 2026)

[5] PowerX and IIJ, "PowerX and IIJ Begin Joint Exploration of Battery Storage-Integrated Containerized Data Centers" (13 February 2026)