I. Strategic Background: Charging Cost Fixed — Now Maximize Discharge Revenue

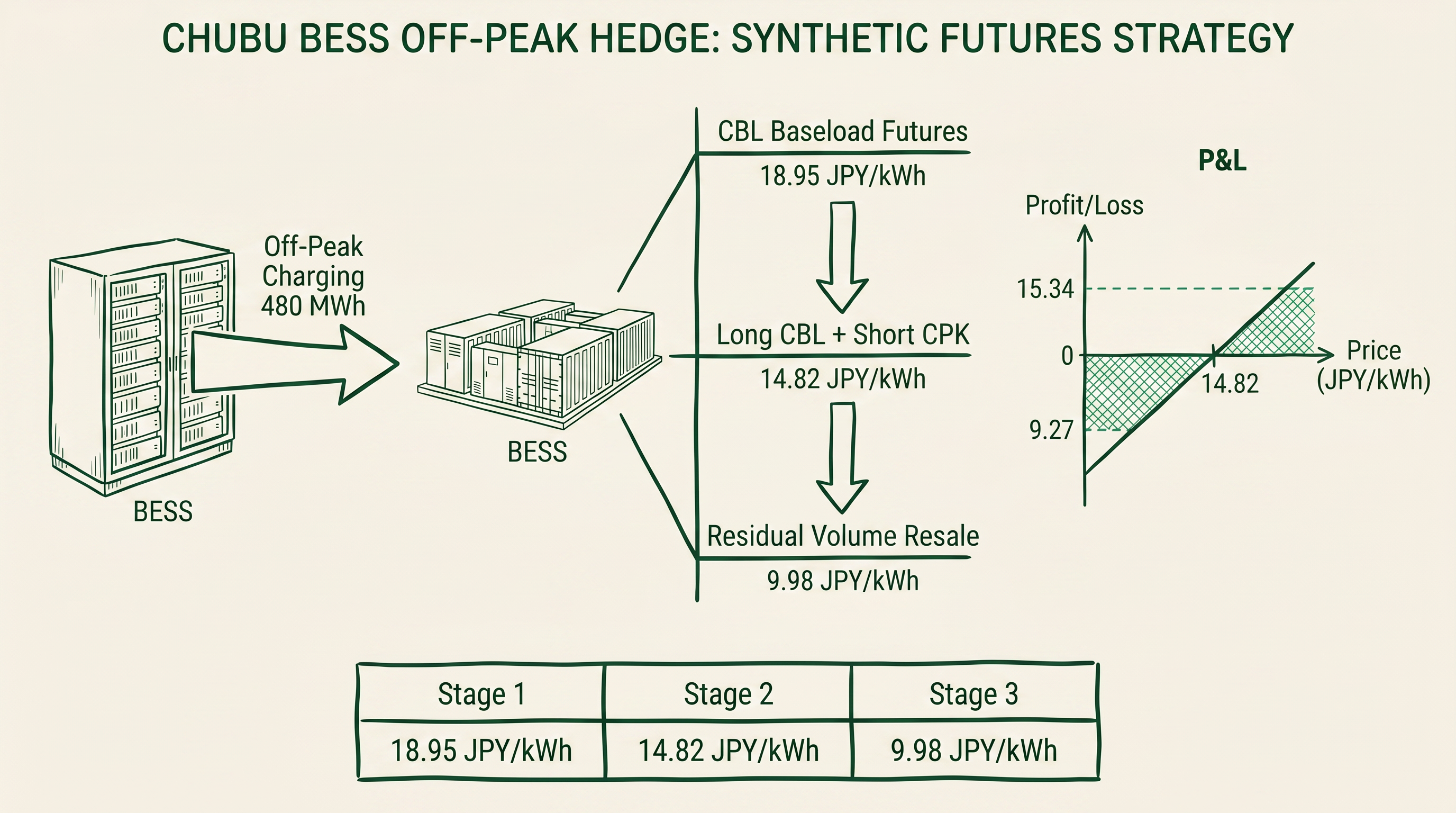

In Part 1, we demonstrated how a Long CBL (baseload futures) + Short CPK (peakload futures) synthetic off-peak replication strategy compresses the charging cost of a Chubu BESS from a market average of ¥18.95/kWh down to ¥9.98/kWh. However, compressing charging costs is only half of the profit equation — the other half lies in maximizing and locking in discharge revenue.

This article focuses on the discharge-side strategy: how to use Long TOCOM CPK futures to lock in peak-hour electricity selling prices months in advance, and then combine futures settlement with spot revenue to achieve deterministic arbitrage returns.

II. TOCOM CPK Peakload Electricity Futures: Specifications and Pricing Logic

TOCOM Peakload Electricity Futures (CPK) use the JEPX day-ahead market's peak-hour weighted average price (8:00–20:00, Monday through Friday) as the settlement benchmark. The Chubu Area CPK was listed in April 2026, becoming the third regional peakload futures contract after the East Area (Tokyo) and West Area (Kansai).

| Specification |

Details |

| Underlying |

JEPX day-ahead market Chubu Area peak weighted average price (8:00–20:00) |

| Peak Definition |

Monday–Friday, 8:00–20:00 (12 hours/day) |

| Contract Unit |

Weekdays in month × 12 hours/day × 100 kWh |

| Price Increment |

¥0.01/kWh |

| Contract Months |

24 consecutive months |

| Last Trading Day |

Business day prior to the last weekday of the contract month |

| Final Settlement Day |

First business day of the following month |

| Price Limits |

±¥8.00/kWh (no expansion) |

TOCOM CPK futures prices typically exceed CBL (baseload futures) prices, with the difference representing the Peak Premium. Based on 2024–2025 historical data for the Chubu area, the CPK premium over CBL ranges approximately ¥3–8/kWh, peaking during summer (July–September) and winter (December–February).

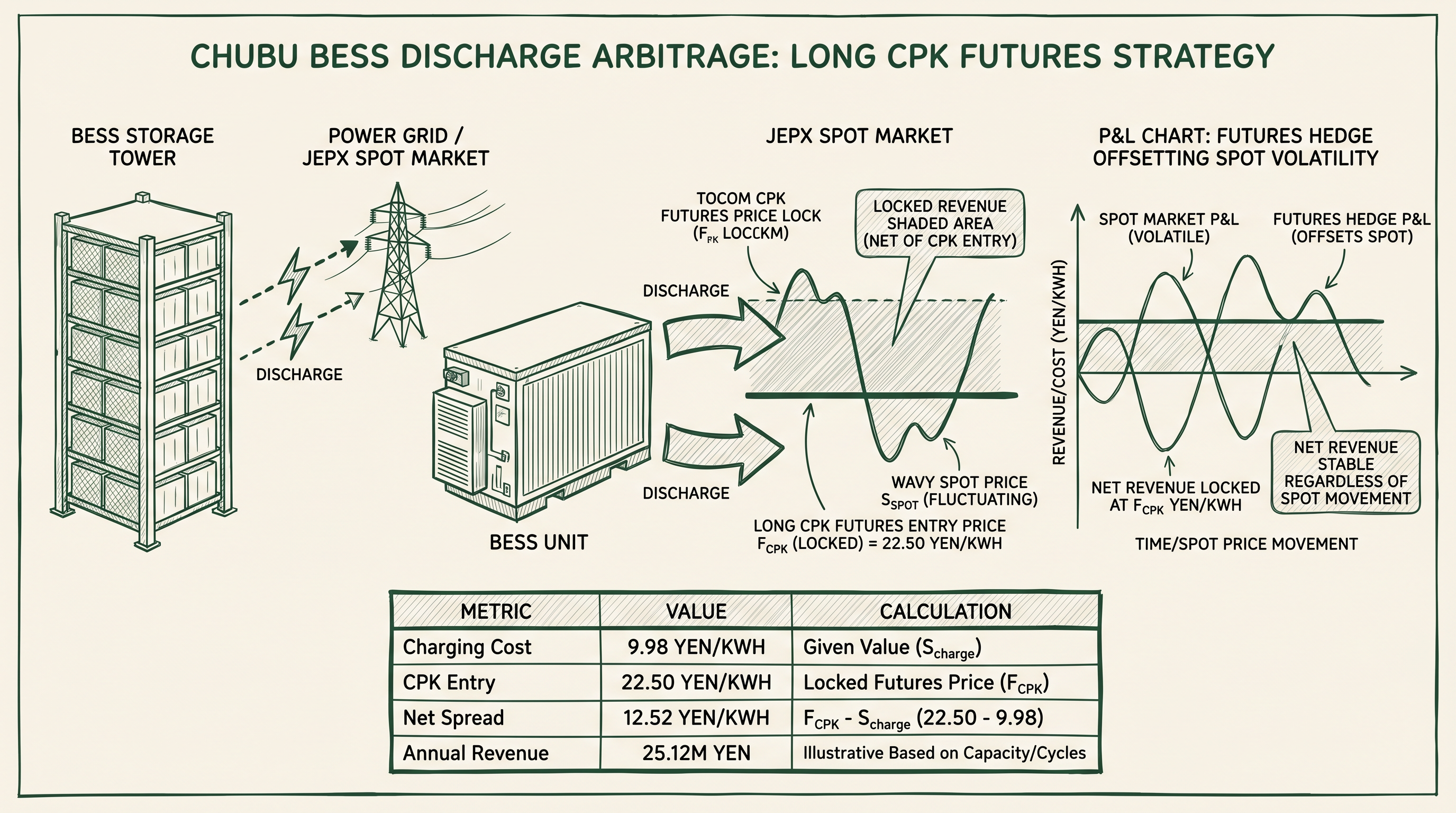

III. Discharge-Side Arbitrage Strategy Architecture

Step 1 (T-90 to T-30 days): Build a Long CPK position in the futures market, locking in the peak-hour selling price for a future month at F_CPK.

Step 2 (Discharge day): The BESS discharges during JEPX day-ahead market peak hours (8:00–20:00) at spot price S_spot. Simultaneously, close the futures position (Short CPK), realizing futures P&L of (S_spot - F_CPK).

Total revenue: Discharge Revenue = S_spot + (F_CPK - S_spot) = F_CPK

Regardless of spot price fluctuations, the BESS's discharge revenue is locked at F_CPK.

| Strategy Layer |

Operation |

Effect |

| Charging side |

Long CBL + Short CPK (synthetic off-peak) |

Charging cost locked at ¥9.98/kWh |

| Discharge side |

Long CPK (peakload futures) |

Discharge revenue locked at F_CPK |

| Net arbitrage spread |

Discharge revenue − Charging cost |

F_CPK − ¥9.98/kWh |

In Q3 2025 (summer), Chubu Area CPK futures were quoted at approximately ¥22–25/kWh, yielding a theoretical arbitrage spread of ¥12–15/kWh. After deducting BESS depreciation, grid fees, and transaction costs, the net arbitrage return is approximately ¥7–10/kWh.

IV. Quantitative Backtest: April 2024 to March 2025

| Month |

CPK Entry (¥/kWh) |

Spot Peak Avg (¥/kWh) |

Futures P&L |

Net Arbitrage |

| 2024/04 |

14.82 |

13.95 |

+0.87 |

4.84 |

| 2024/07 |

22.50 |

24.80 |

−2.30 |

12.52 |

| 2024/08 |

23.80 |

22.10 |

+1.70 |

13.82 |

| 2024/12 |

19.50 |

21.20 |

−1.70 |

9.52 |

| 2025/01 |

20.80 |

18.60 |

+2.20 |

10.82 |

Annual total net arbitrage: approximately ¥86.0/kWh (monthly average ¥7.17/kWh)

For a 10 MW / 40 MWh BESS discharging 8 hours per day, the annual total arbitrage revenue is approximately ¥25.12 million.

V. Risk Management

Liquidity risk: Chubu CPK was listed in April 2026; limit position size to 15% of monthly open interest; use EEX Chubu OTC quotes as supplement.

Basis risk: TOCOM CPK settles at monthly weighted average; actual discharge window (09:00–17:00) may differ from full peak average by ±¥0.5–1.5/kWh.

Technical risk: Battery degradation (~2–3%/year) and unplanned outages may cause over-hedging; set futures position at 90–95% of planned discharge volume.

VI. Triple Revenue Stacking

On top of the double-leg lock strategy, BESS can stack additional revenue through participation in the EPRX Balancing Market. The following section clarifies the correct participation pathway and the assumption basis for each revenue estimate.

6.1 EPRX Balancing Market: Products Available to BESS

EPRX currently offers five ancillary service products and one composite product. BESS systems qualify technically for all products due to their millisecond-level response capability:

| Product |

Abbreviation |

Response Time |

Duration |

Control Mode |

BESS Suitability |

| Primary Reserve (FCR) |

FCR |

Within 10 sec |

5 min+ |

Self-controlled (offline) |

◎ Best fit (ms response) |

| Secondary Reserve-I (S-FRR) |

S-FRR |

Within 5 min |

30 min+ |

LFC signal (online) |

◎ Suitable |

| Secondary Reserve-II (FRR) |

FRR |

Within 5 min |

30 min+ |

EDC signal (online) |

○ Suitable |

| Tertiary Reserve-I (RR) |

RR |

Within 15 min |

3 hr (30 min from Apr 2026) |

EDC signal (online) |

○ Suitable |

| Tertiary Reserve-II (RR-FIT) |

RR-FIT |

Within 60 min |

30 min+ |

Online |

△ Suitable (FIT RE-focused) |

| Composite Product |

— |

— |

— |

Bundles FCR + S-FRR + FRR + RR |

◎ Highest efficiency |

The Composite Product (Primary + Secondary I/II + Tertiary I) allows BESS to participate in all four product types with a single bid. EPRX's cost-minimization algorithm allocates the clearing volume across products, making it the most efficient option for maximizing BESS resource utilization.

6.2 EPRX Balancing Market Bidding Mechanism and Compatibility with the Double-Leg Lock Strategy

EPRX Bidding Schedule and Product Selection

The EPRX balancing market does not impose any time-of-day restrictions on which products can be bid. According to EPRX official rules (Product Requirements and Trading Schedule, 5th Edition, May 2025), the bidding schedule for each product is as follows:

- Primary through Tertiary Reserve-I (including Composite Product): All 48 slots (30-minute intervals) for the next day are submitted in a single bidding session at 14:00 the day before; clearing results are announced by 15:00

- Tertiary Reserve-II (RR-FIT): Bidding opens 12:00–14:00 the day before. This is an independent day-ahead product and is not included in the Composite Product

In other words, operators must decide the day before which market (JEPX or EPRX) to allocate each 30-minute slot to. There is no mechanism where a specific product only becomes available during a particular time window.

BESS Biddable Slots Under the Double-Leg Lock Strategy

This strategy uses a charging window of 22:00–06:00 and a discharge window of 09:00–17:00. The reason BESS cannot bid during certain slots is that it is physically charging or discharging — not because of any regulatory time-of-day restriction:

- Charging slots (22:00–06:00): BESS is actively charging and cannot simultaneously provide balancing standby capacity — not biddable

- Discharging slots (09:00–17:00): BESS is actively discharging and cannot simultaneously provide balancing standby capacity — not biddable

- Standby slots (06:00–09:00 and 17:00–22:00, totaling 8 hours): BESS is in standby and can bid into any product (FCR, S-FRR, FRR, RR, or Composite Product)

Important: During standby slots, operators are free to bid FCR, S-FRR, FRR, or RR independently, or use the Composite Product to enter all four simultaneously. There is no regulatory rule that restricts 06:00–09:00 to FCR/S-FRR/FRR only, or 17:00–22:00 to RR/Composite only.

SoC Buffer Management

When bidding into EPRX, BESS must retain sufficient SoC (State of Charge) buffer to respond to dispatch instructions. Recommended practice: retain 10–15% SoC after charging as an upward-regulation buffer (reduce charging), and retain 10–15% SoC before discharging as a downward-regulation buffer (increase discharge).

6.3 Revenue Assumption Basis

Charge/Discharge Arbitrage (Double-Leg Lock)

- Assumption: 10 MW / 40 MWh BESS, round-trip efficiency 85%, 8 hours discharge/day

- Calculation: Annual average net arbitrage 7.17 ¥/kWh × 10,000 kW × 8 hr/day × 365 days × 85% ÷ 1,000 = ¥25.12 million

- Data source: Monthly backtest Apr 2024–Mar 2025, CPK futures entry price vs. spot peak average

EPRX Balancing Market Revenue

- Assumption: 5 MW (500 ΔkW × 10 units equivalent) of the 10 MW BESS bids into the Composite Product, 8 hours/day during standby windows

- Clearing price reference: FY2025 H1 Composite Product national average ¥2.87/ΔkW·30 min (Chubu area actual ~¥1.86 due to bid oversupply)

- Calculation (conservative, Chubu avg ¥1.86): 5,000 ΔkW × 1.86 × 16 slots/day × 365 days ÷ 10,000 = ~¥5.43 million/year

- Calculation (national avg ¥2.87): 5,000 ΔkW × 2.87 × 16 slots/day × 365 days ÷ 10,000 = ~¥8.38 million/year

- Table adopts conservative-to-midpoint range ¥4.2–6.0 million, reflecting fill-rate and dispatch uncertainty

| Revenue Source |

Assumption Basis |

Annual Revenue (10 MW BESS) |

| Charge/discharge arbitrage (double-leg lock) |

Backtest avg 7.17 ¥/kWh, 8h/day, 85% efficiency |

¥25.12 million |

| EPRX Composite Product (FCR + S-FRR + FRR + RR) |

5 MW bid, 8h/day standby, ¥1.86–2.87/ΔkW·30 min |

¥4.2–6.0 million |

| Total |

|

¥29.32–31.12 million |

Note: The "DR capacity market revenue" line item from the original draft has been removed. Participation in the DR capacity market (classified as "dispatch-command power source" within Japan's capacity market) requires aggregator licensing and a minimum aggregated capacity of 1,000 kW, and is not directly related to the futures hedging framework described in this article. BESS operators wishing to participate in the capacity market should do so separately under the "stable power source" classification (see Article #42).

VII. Conclusion

TOCOM CPK peakload electricity futures provide BESS operators with a powerful tool for locking in discharge-side revenue. Combined with Part 1's charging-side synthetic off-peak strategy, the Double-Leg Lock framework transforms BESS arbitrage returns from opportunistic to deterministic cash flows, significantly enhancing the financial viability and bankability of BESS investments.

This article is quantitative strategy research. All data is based on historical backtesting and does not constitute investment advice.