Introduction: A Doubling in Five Weeks

On February 28, 2026, the United States and Israel launched military strikes against Iran, triggering a rapid deterioration in Middle East geopolitics. Iran announced the closure of the Strait of Hormuz — the critical chokepoint through which 20% of global LNG flows pass. Three weeks later, Iranian missiles struck Qatar's LNG liquefaction facilities, sidelining 12.8 million tonnes per year of liquefaction capacity for an estimated three to five years.

This sequence of events unleashed the most severe supply shock in global gas markets since the 2022 Russia-Ukraine war. The Asian LNG spot price benchmark JKM (Japan Korea Marker) surged from approximately $10/MMBtu before the conflict to $25.30/MMBtu within five weeks — a three-year high representing a 143% increase. Japan's JEPX next-day spot electricity price simultaneously climbed to ¥23.15/kWh, the highest level since January 2023.

This article analyzes the transmission mechanism from LNG prices to JEPX electricity markets in detail, reviews the 2022 historical precedent, and assesses the risk landscape and strategic responses for Japan's electricity market under the 2026 geopolitical shock.

Japan's Structural LNG Dependency

Understanding the LNG price transmission mechanism requires first recognizing the fundamental vulnerability of Japan's energy structure. Over 30% of Japan's electricity generation comes from natural gas-fired power plants, and virtually all of that gas is imported as LNG. Japan is the world's second-largest LNG importer, with annual imports of approximately 70 million tonnes sourced primarily from Australia (~35%), Malaysia (~12%), Qatar (~10%), Russia (~9%), and the United States (~9%).

The Japanese government's official position is that only 6% of Japan's LNG imports directly transit the Strait of Hormuz and that Japan holds approximately three weeks of domestic LNG inventory, limiting direct exposure. However, this view overlooks the highly integrated nature of global LNG markets: regardless of how diversified the procurement portfolio, Japan's LNG acquisition costs ultimately anchor to the global benchmark price JKM. The 2022 Russia-Ukraine war demonstrated this clearly — Russian LNG accounted for only 8.7% of Japan's imports, yet Japan's monthly LNG import bill surged from ¥221.3 billion (April 2021) to ¥878 billion (August 2022), nearly a fourfold increase.

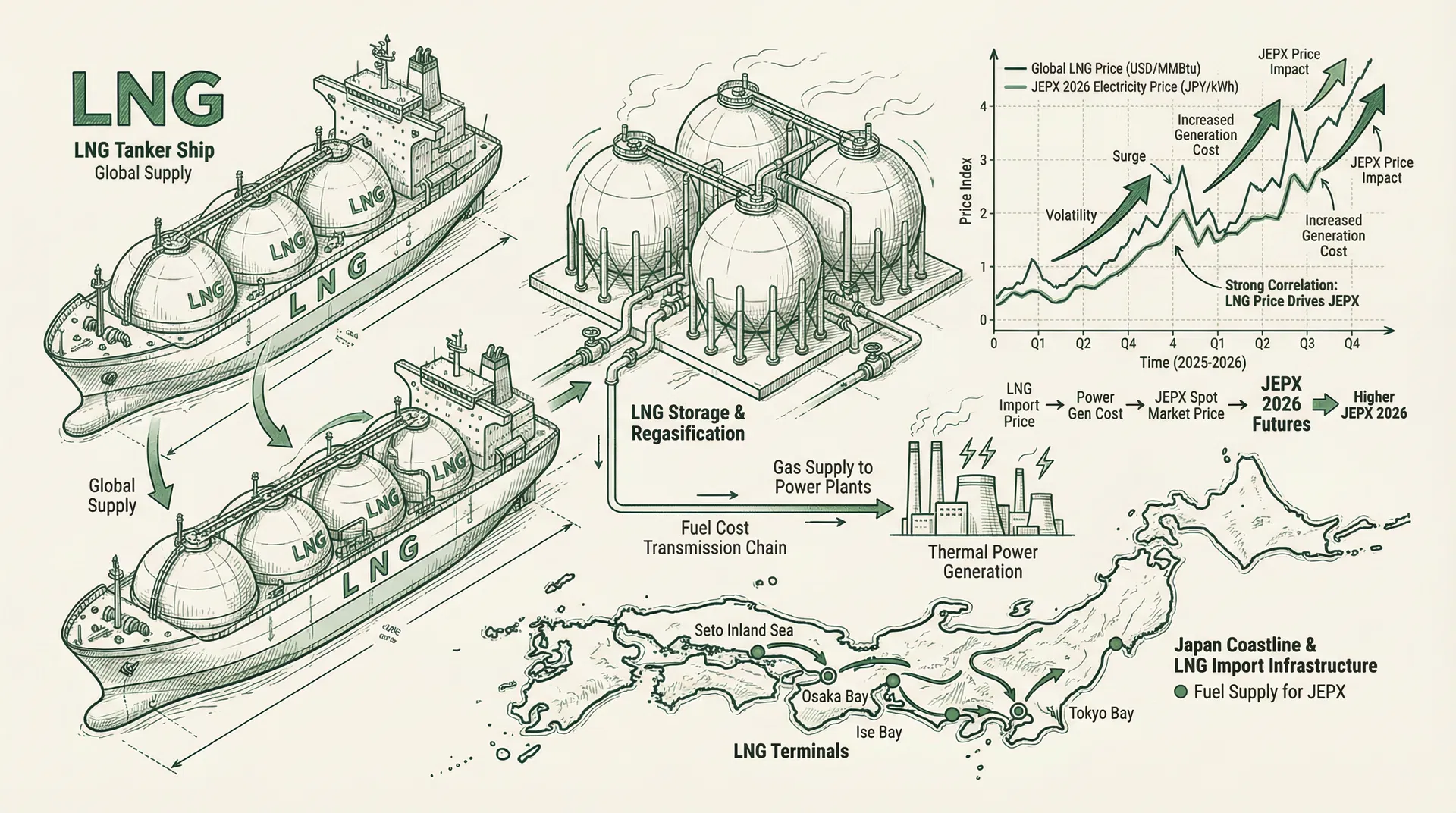

The LNG-to-JEPX Transmission Mechanism

LNG price transmission to JEPX electricity markets operates through four interconnected channels.

Channel 1: Marginal Cost Bidding Mechanism

Under Japan JEPX's gross bidding system, power companies submit bids based on marginal cost. Gas-fired power plants' marginal costs are primarily composed of fuel costs, so when JKM spot prices rise, gas plants' variable costs increase and their bids are raised accordingly. Since gas generation typically serves as the "marginal unit" (price setter) in Japan's power system, its cost changes directly determine JEPX clearing prices.

Channel 2: Long-Term Contract Oil Linkage

The majority of Japan's LNG imports (approximately 70-80%) are procured through long-term contracts (LTCs) with prices typically linked to Japan's crude oil import average price (JCC). After the 2026 conflict erupted, Brent crude surged from $72/barrel on February 27 to $103/barrel on March 17, with Iran warning that oil prices could reach $200/barrel. Rising crude oil prices transmit to LTC procurement costs through the JCC linkage mechanism with approximately a two-month lag, further increasing electricity companies' fuel costs.

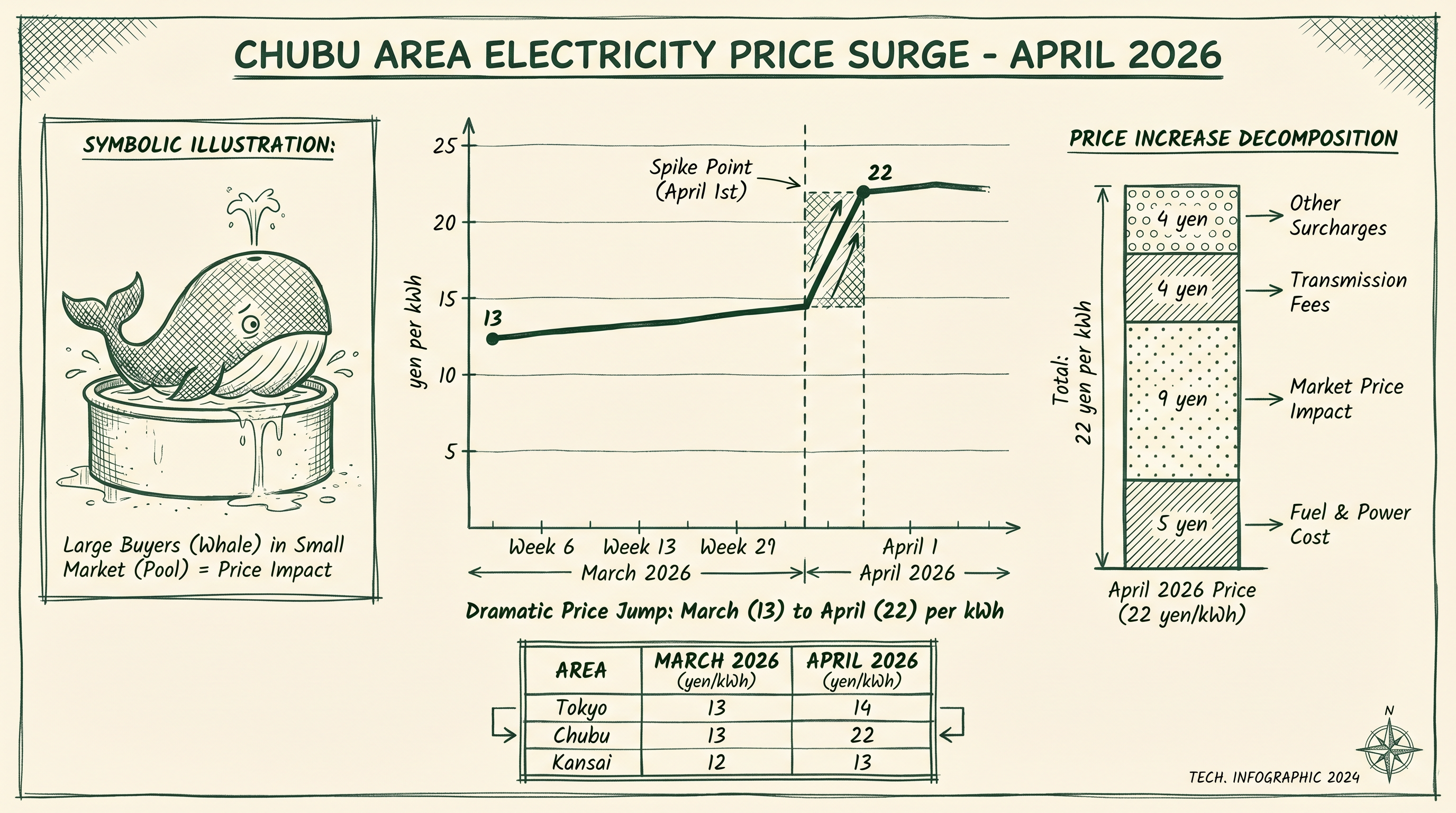

Channel 3: Fuel Cost Adjustment Mechanism

Japan's electricity retail tariffs incorporate a "fuel cost adjustment mechanism" (燃料費調整制度) that allows utilities to reflect fuel cost changes in retail electricity rates with approximately a two-month lag. TEPCO and Chubu Electric have announced rate increases from April 2026, with an estimated annual increase of approximately ¥15,000 per household. However, regulated tariffs have caps, and during extreme fuel price shocks utilities cannot fully recover costs — nine major utilities recorded net losses in 2022.

Channel 4: Imbalance Fee Amplification

Rising JEPX electricity prices also produce an amplification effect through the imbalance fee (インバランス料金) mechanism. As detailed in Article 11 on this site, the C-value was raised from ¥200 to ¥300/kWh from April 2026. When JEPX electricity prices rise sharply due to LNG price increases, the penalty costs for supply-demand imbalances expand simultaneously, with particularly significant impacts on small retailers and renewable energy generators.

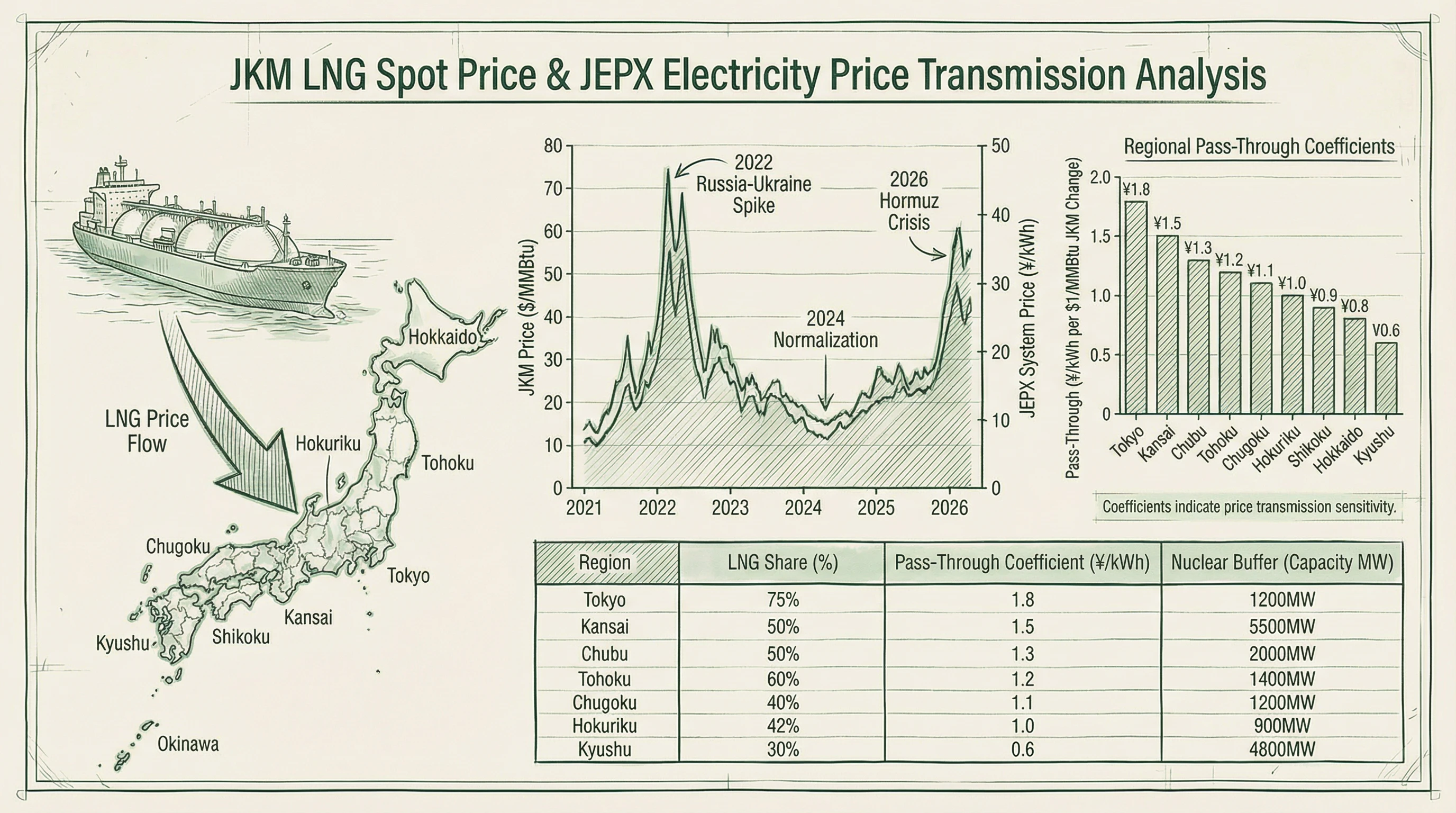

The 2022 Russia-Ukraine War: Lessons from Historical Precedent

The 2022 Russia-Ukraine war provides the most direct historical precedent for LNG price shock transmission to Japan's electricity market. JKM surged from $5/MMBtu in February 2021 to $56/MMBtu in October 2021, and further above $70/MMBtu in 2022. JEPX's annual average system price rose from ¥13.43/kWh in FY2021 to ¥20.41/kWh in FY2022, with spikes exceeding ¥65/kWh during periods of extreme volatility.

This shock had profound structural impacts on the market. 195 electricity retailers (27.6% of those registered in April 2021) suspended contracts, withdrew, or exited the market. Nine major utilities recorded net losses for the April-December 2022 period. Japan's fossil fuel import bill surged from $93 billion (¥17 trillion) in 2021 to $185 billion (¥33.7 trillion) in 2022, with the trade deficit expanding to over $110 billion (¥20 trillion).

Quantitative Assessment of the 2026 Shock

The 2026 Middle East shock resembles the 2022 Russia-Ukraine war in several dimensions but also presents structural differences. Similarities include the sudden contraction of global LNG supply (2022: Russian pipeline gas cutoff; 2026: Qatar liquefaction capacity loss), the competitive dynamic of Asia and Europe competing for limited spot cargoes, and the amplification of import costs by yen weakness.

The key difference lies in the durability of the supply gap. Qatar's 12.8 mtpa liquefaction capacity loss is expected to require three to five years to repair, whereas the 2022 European energy crisis was partially alleviated within one to two years through new supply (US LNG expansion). Additionally, US LNG export facilities are already operating near full capacity in 2026, making it difficult to quickly replace lost volumes.

| Metric |

2022 Russia-Ukraine |

2026 Middle East |

| JKM Peak | ~$70/MMBtu | $25.30/MMBtu (as of Mar 19) |

| JKM Increase | ~1,300% (from $5 bottom) | +143% (five weeks) |

| JEPX Peak | >¥65/kWh | ¥23.15/kWh (3-year high) |

| Supply Gap Duration | 1-2 years | Est. 3-5 years (Qatar repair) |

| Japan Direct Supply Impact | Low (Russia 8.7%) | Low (Hormuz direct 6%) |

| Global Market Transmission | High | High |

| Government Subsidies | ¥13.4 trillion (2022-2025) | ¥5 trillion (Feb 2026 package) |

Forward Outlook: Market Signals from the Futures Curve

As of early April 2026, market views on the LNG price outlook diverge significantly. Rabobank forecasts Asian LNG average prices at $16.62/MMBtu for 2026 and declining to $13.60/MMBtu in 2027. UBS holds a more pessimistic view, forecasting 2026 average prices at $23.60/MMBtu and $14.50/MMBtu in 2027.

The pre-conflict (January 2026) market consensus was approximately $10/MMBtu for 2026 JKM average, as forecast by Kpler and others. After the conflict erupted, the forward curve shifted sharply upward, with the premium between pre-war and post-war forward curves (the shaded area in this article's chart) representing the market's pricing of geopolitical risk.

Key variables affecting the subsequent trajectory include: the duration of the Strait of Hormuz closure, the pace of Qatar LNG facility repairs, whether US LNG exports can be further increased, whether China increases procurement to fill the gap, and yen exchange rate movements.

Implications for Electricity Market Participants

The 2026 Middle East shock's impact on Japan's electricity market participants varies significantly by participant type. For small retailers dependent on short-term JEPX procurement, the sharp rise in electricity procurement costs directly compresses margins and risks repeating the 2022 market exit wave. For retailers holding long-term fixed-price contracts, the short-term impact is relatively contained, but if high prices persist until contract expiration, renewal risk becomes significant.

For renewable energy generators, rising JEPX prices boost spot revenues while the imbalance fee amplification effect also increases supply-demand management difficulty. For utilities holding natural gas generation assets, managing the spread between high fuel costs and high electricity prices, along with the lag effects of the fuel cost adjustment mechanism, constitutes the primary financial management challenge.

From a long-term structural perspective, the 2026 shock has again highlighted the urgency of Japan's energy structure transformation. IEEFA and others note that LNG supply diversification strategies cannot fundamentally protect Japan from global price shocks, and that accelerating domestic renewable energy deployment is the true solution to reducing dependence on global LNG markets.

Conclusion

LNG price transmission to JEPX electricity markets is a concentrated manifestation of Japan's energy security vulnerability. From geopolitical events in the Strait of Hormuz to rising household electricity bills in Japan, this transmission chain operates through four mutually reinforcing channels: spot market bidding, long-term contract oil linkage, the fuel cost adjustment mechanism, and imbalance fees. The historical precedents of the 2022 Russia-Ukraine war and the 2026 Middle East shock demonstrate that even when Japan's direct supply exposure is limited, the integration of global LNG markets ensures full transmission of shocks.

For electricity market participants, deep understanding of the LNG-JEPX transmission mechanism, building diversified electricity procurement strategies, improving supply-demand forecast accuracy, and actively deploying flexibility resources such as battery storage are the core capabilities required to maintain competitiveness in a highly uncertain geopolitical environment.