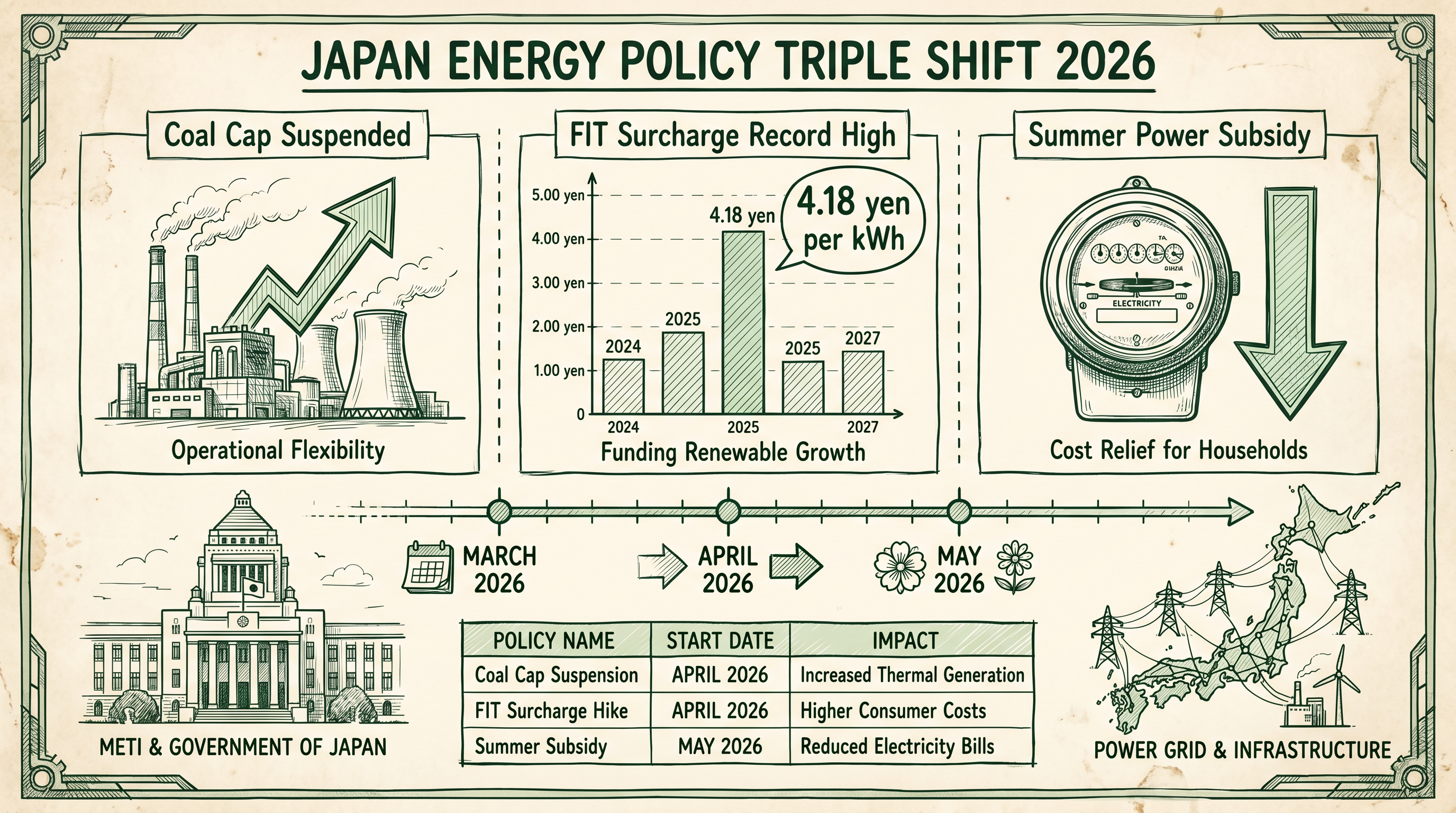

Three contradictory METI policies enacted in five weeks — coal cap suspension, record FIT levy at ¥4.18/kWh, and summer subsidy revival — reveal the structural tension between energy security and decarbonisation in Japan's electricity market.

In the span of five weeks between late March and late April 2026, Japan's Ministry of Economy, Trade and Industry (METI) enacted three energy policies that, taken together, expose a fundamental contradiction at the heart of Japan's electricity transition. On March 27, METI suspended its 50% utilisation rate cap on inefficient coal-fired power plants. On March 19, the government confirmed the FY2026 renewable energy surcharge (再エネ賦課金) at a record ¥4.18 per kilowatt-hour. And on April 30, Reuters reported that the government is considering reviving electricity and gas subsidies worth up to ¥500 billion for the July–September summer period. Three policies, three different directions, one energy crisis.

The Hormuz Trigger: Why Coal Is Back

The immediate catalyst for Japan's policy reversal on coal is the effective closure of the Strait of Hormuz following the U.S.-Israel conflict with Iran. Japan imports approximately 4 million metric tons of LNG annually via the strait — roughly 6% of its total LNG imports. With that supply route disrupted, METI faced a stark arithmetic problem: how to maintain grid stability through the summer peak demand season without the LNG volumes it had counted on.

The answer, announced on March 27, was to temporarily suspend the 50% capacity utilisation cap that had been placed on coal-fired power plants with generation efficiency below 42%. These plants — older, dirtier, and previously restricted precisely because of their carbon intensity — are now permitted to run at higher utilisation rates for the entirety of FY2026 (April 2026 through March 2027). METI estimates the measure will reduce LNG consumption by approximately 0.5 million tons per year, equivalent to slightly more than 10% of Japan's Hormuz-route LNG imports.

At the time of the announcement, Japan held an LNG stockpile of around 4 million tons — roughly one year's worth of Hormuz-route supply. The coal cap suspension is therefore a precautionary measure as much as an emergency response: a buffer against further supply disruption rather than a response to an immediate shortage.

"This is strictly a short-term adjustment and does not alter our long-term decarbonisation policy." — METI official, March 27, 2026

The METI official's framing is important. The suspension is explicitly time-limited to one fiscal year and is presented as an emergency measure under the energy security provisions of Japan's electricity law. It does not, on paper, represent a policy reversal on coal. But the optics are difficult: Japan's 7th Strategic Energy Plan, finalised just 13 months earlier in February 2025, set a 2040 target of 40–50% renewable energy and approximately 20% nuclear, with coal's share expected to fall sharply. Reactivating the coal fleet — even temporarily — sends a signal to markets and investors that Japan's decarbonisation timeline is more conditional than its official targets suggest.

The FIT Surcharge: A Record That Keeps Rising

While the coal cap suspension attracted international headlines, a quieter but equally significant policy change took effect on May 1, 2026: the annual reset of Japan's renewable energy promotion surcharge (再エネ賦課金). For FY2026, the rate was set at ¥4.18 per kilowatt-hour — up ¥0.20 from FY2025's ¥3.98/kWh and the highest level since the surcharge was introduced in 2012.

The numbers are striking in their cumulative scale. When the FIT surcharge launched in 2012, the rate was approximately ¥0.22/kWh. In 14 years, it has risen roughly 19-fold. The total national burden in FY2026 is estimated at approximately ¥3.2 trillion — a record. For a typical household consuming 400 kWh per month, the monthly surcharge is now ¥1,672, or ¥20,064 per year. This is the first fiscal year in which the annual household burden has exceeded ¥20,000.

The mechanism behind the rise is structural rather than discretionary. The surcharge is calculated each year based on the gap between the fixed FIT purchase price paid to renewable generators and the "avoided cost" — the market price at which utilities would otherwise have purchased the equivalent electricity. When fossil fuel prices fall, the avoided cost falls, and the gap widens, pushing the surcharge higher. The stabilisation of LNG and coal prices in 2025 — ironically, before the Hormuz disruption — reduced the avoided cost calculation and drove the FY2026 surcharge to its record level.

📋 Key Terminology: Renewable Energy Surcharge

English

日本語

中文

Notes

Renewable Energy Surcharge

再エネ賦課金

再生能源賦課金

Official name: 再生可能エネルギー発電促進賦課金

FIT (Feed-in Tariff)

固定価格買取制度(FIT)

固定價格收購制度

Guaranteed purchase price for renewable generators

FIP (Feed-in Premium)

フィードインプレミアム(FIP)

市場連動型補貼(FIP)

Market-linked premium replacing FIT for new projects

Avoided Cost

回避可能費用

可迴避費用

Market price utilities would pay without FIT purchases

FIT Purchase Cost

FIT買取費用

FIT收購費用

Total cost utilities pay to renewable generators at fixed rates

Surcharge Unit Price

賦課金単価

賦課金單價

¥4.18/kWh in FY2026 (announced by ANRE each March)

Agency for Natural Resources and Energy (ANRE)

資源エネルギー庁

資源能源廳

METI sub-agency that sets annual surcharge rate

Renewable Energy Special Measures Act

再エネ特措法

再エネ特措法

Legal basis for the FIT/FIP system and surcharge

Net Load

残余需要(ネット需要)

淨負載

Total demand minus renewable generation

Output Curtailment

出力制御

出力抑制

Grid operator instruction to reduce renewable output

The surcharge's trajectory also reflects the success of Japan's renewable energy buildout. More solar and wind capacity receiving FIT payments means a larger total payment obligation, even as per-unit FIT rates for new projects have fallen. Japan's cumulative installed solar capacity has grown dramatically since 2012, and the FIT payment pool has expanded accordingly.

Mega Solar's Exit from FIT: A Structural Transition

On March 19, 2026 — eight days before the coal cap announcement — METI made a separate but structurally significant decision: it will discontinue FIT and FIP (Feed-in Premium) support for ground-mounted commercial solar power plants from FY2027 onwards. Rooftop solar and residential installations will continue to receive support, but utility-scale ground-mounted projects will need to compete in the market without guaranteed purchase prices.

The decision follows the "Mega Solar Countermeasure Package" adopted at an inter-ministerial meeting at the end of 2025, which brought together METI, the Ministry of the Environment, and the Ministry of Agriculture, Forestry and Fisheries to address the social and environmental impacts of large-scale solar development — including land use conflicts, deforestation, and community opposition. The package has three pillars: strengthening legal regulations on inappropriate projects, improving collaboration with local communities, and prioritising support for community-integrated installations.

For the electricity market, the end of FIT for mega solar has two implications. First, it will slow the pace of large-scale solar development in Japan, as developers lose the revenue certainty that FIT provided. Second, it will gradually reduce the FIT payment pool over time, potentially easing the surcharge burden on consumers in future years — though the existing FIT contracts for already-installed capacity will continue to be honoured for their full 20-year terms.

Summer Subsidies: The Third Policy Lever

The third element of Japan's policy response emerged on April 30, 2026, when Reuters reported that the government is considering reviving electricity and gas subsidies for the July–September summer period. The proposed budget is up to ¥500 billion ($3.1 billion), to be funded from existing reserve funds rather than a supplementary budget.

The context is the expected pass-through of higher LNG costs into retail electricity prices. Industry Minister Ryosei Akazawa has indicated that the impact of elevated LNG prices on retail tariffs is likely to begin emerging around June 2026 — just as summer demand peaks. The government's concern is that households and businesses, already facing the record FIT surcharge from May, will face a compounding increase in their electricity bills precisely when consumption is highest.

The subsidy proposal is the third time in recent years that Japan has used direct price support to cushion the impact of energy market volatility on consumers. The government has already drawn on ¥2 trillion in reserves for gasoline subsidies in response to the Hormuz disruption. Adding electricity and gas subsidies would accelerate the depletion of those reserves, raising questions about fiscal sustainability if energy prices remain elevated through the autumn.

The Structural Tension: Three Policies, One Contradiction

Viewed together, the three policies reveal a structural tension that Japan's energy transition has not yet resolved. The coal cap suspension prioritises energy security over decarbonisation. The record FIT surcharge reflects the accumulated cost of the renewable buildout that decarbonisation requires. And the summer subsidy proposal attempts to shield consumers from the price consequences of both the energy security crisis and the transition costs simultaneously.

This is not a contradiction born of poor planning. It is the predictable result of Japan's geography and energy mix. Japan has no domestic fossil fuel resources, no pipeline connections to neighbouring countries, and a nuclear fleet that, despite 15 reactor restarts since Fukushima, still provides only 5.6% of electricity generation. The 7th Strategic Energy Plan's 2040 targets — 40–50% renewables, 20% nuclear — are ambitious precisely because the starting point is so challenging.

The Hormuz crisis has accelerated the timeline on which these tensions become visible. What might have played out gradually over years — the phase-out of coal, the rising cost of the renewable transition, the fiscal limits of consumer subsidies — has been compressed into a single fiscal year. For electricity market participants in Japan, the policy environment in FY2026 is unusually complex: a coal fleet operating at higher utilisation, a record FIT levy, the end of mega solar FIT support, and the possibility of summer price subsidies that may distort retail market signals.

Implications for JEPX and Power Market Participants

For traders and generators active in the Japan Electric Power Exchange (JEPX), the coal cap suspension has a direct market implication. Higher coal plant utilisation increases baseload supply, which, all else equal, exerts downward pressure on JEPX spot prices — particularly during off-peak hours when coal plants cannot easily reduce output. However, the Hormuz-driven LNG supply uncertainty simultaneously creates upside price risk during peak demand periods when gas-fired peakers are needed.

The net effect on JEPX prices in FY2026 is therefore ambiguous and will depend heavily on the actual LNG supply situation as it evolves. If LNG supplies via alternative routes (Australia, US, Qatar via Cape of Good Hope) prove sufficient to cover the Hormuz shortfall, the coal cap suspension may simply add to an already well-supplied market, suppressing prices. If LNG supply tightens further, the coal capacity may prove insufficient to prevent price spikes during summer peak periods.

The end of mega solar FIT support from FY2027 is a longer-term signal for renewable developers: the era of guaranteed returns for ground-mounted solar in Japan is ending. Future large-scale solar projects will need to be structured around corporate PPAs, capacity market revenues, or merchant market exposure — a more complex financing environment that will likely slow development in the near term but may ultimately produce a more market-integrated renewable sector.

This site uses cookies to remember your language preference and collect anonymous traffic statistics to improve our content. You can choose to accept or decline non-essential cookies. Learn more