Japan Grid-Scale Battery Storage Policy: Rapid Grid Connection and Non-Firm Access Reform (April 2026)

Introduction

Japan's Ministry of Economy, Trade and Industry (METI) is actively pursuing significant reforms to its grid-scale battery storage (BESS) policies, aiming to accelerate grid connection and introduce non-firm access mechanisms. These initiatives, detailed in April 2026 working group documents, are crucial for integrating a rapidly expanding renewable energy landscape and enhancing grid stability. The policy adjustments are designed to address current limitations, particularly the underutilization of BESS for energy arbitrage, and to pave the way for a more flexible and resilient power grid by 2040 [1] [2].

Current Landscape of Grid-Scale Battery Storage in Japan

Installed Capacity and Future Targets

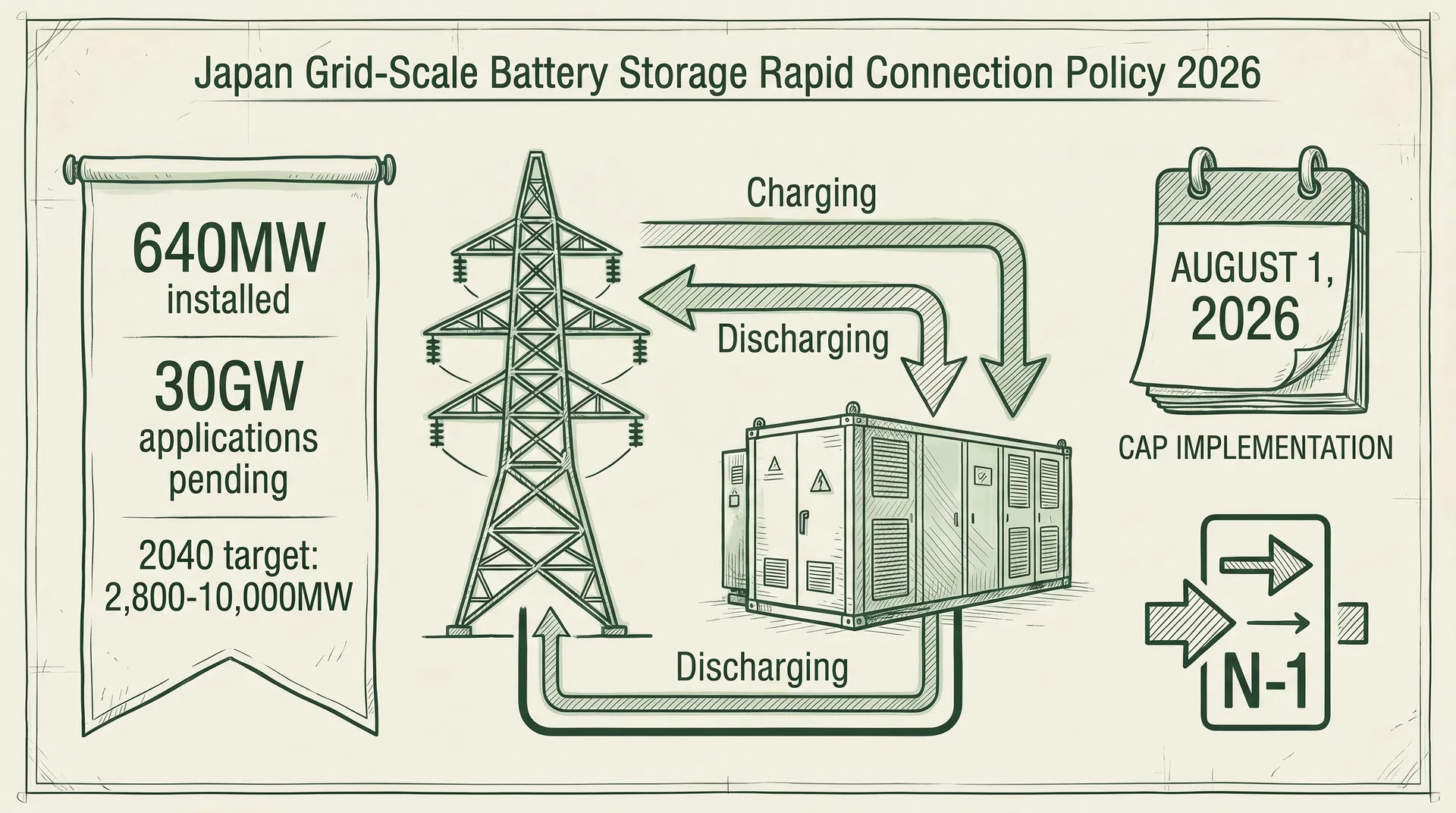

As of April 2026, Japan's grid-scale BESS installed capacity stands at 640 MW (64万kW). However, the ambition for future expansion is substantial, with contracted applications already reaching approximately 30 GW (3,000万kW). METI has set an ambitious target for 2040, aiming for a total grid-scale BESS capacity between 2,800 MW and 10,000 MW (280万〜1,000万kW) [1]. This significant increase underscores the strategic importance of battery storage in Japan's long-term energy strategy.

Key Issues: Ancillary Services vs. Arbitrage

Currently, grid-scale BESS in Japan is predominantly utilized for ancillary services (調整力), which involve maintaining grid stability by balancing supply and demand fluctuations. While essential, this focus has led to limited deployment for arbitrage use, where batteries charge during periods of low electricity prices and discharge during high prices, thereby optimizing economic value and reducing overall system costs. The existing regulatory framework and operational practices have largely constrained BESS to a reactive role rather than a proactive one in market optimization [2].

Policy Direction: Promoting 'Storage-Type Operation'

To unlock the full potential of grid-scale BESS, METI is promoting a shift towards 'storage-type operation' (ストレージ式運用). This policy direction aims to empower Transmission System Operators (TSOs) to flexibly manage the State of Charge (SoC) within the surplus capacity of BESS units. By enabling this flexibility, BESS can participate more effectively in energy markets, facilitating arbitrage opportunities and contributing to a more efficient and cost-effective grid operation. This approach is expected to maximize the economic benefits of battery storage beyond just ancillary services [1].

Rapid Grid Connection Measures

To address the bottleneck of grid connection for new BESS projects, METI is introducing several rapid grid connection measures. These measures are designed to allow early grid integration without necessitating immediate, costly grid reinforcement, thereby accelerating deployment.

N-1 Charging Stop Devices

One key measure involves the installation of N-1 charging stop devices (N-1充電停止装置). These devices are designed to automatically halt battery charging if a critical grid component (e.g., a transmission line or transformer) fails, thus preventing an N-1 contingency (the loss of one system element) from cascading into a wider outage. By mitigating this risk, BESS projects can connect to the grid more quickly, as the need for extensive grid upgrades to handle N-1 scenarios is reduced [2].

Charging Restrictions During Specific Periods

Another measure involves agreements to implement charging restrictions during specific time periods. This means BESS operators would agree to limit or cease charging during certain hours when grid congestion is anticipated or when renewable energy output is low. This proactive management of charging patterns helps to alleviate strain on the existing grid infrastructure, allowing for faster grid connection without requiring immediate reinforcement [1].

Major Regulatory Changes by OCCTO

Per-Operator Cap on Grid Connection Study Applications

In a significant regulatory development, the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) plans to revise its regulations from August 1, 2026. This revision will introduce a per-operator cap on grid connection study applications. This means each TSO will have a specific limit on the number of new grid connection applications they can process simultaneously. The exact cap numbers are currently being calculated by individual TSOs and will be published on their respective websites [2].

Implementation Timeline and Impact

Applications exceeding these newly imposed caps will not be processed until the cap is resolved, either through the completion of existing studies or an increase in TSO capacity. This measure aims to streamline the application process, prevent backlogs, and ensure that TSOs can manage the influx of new connection requests more efficiently. While potentially slowing down some projects in the short term, the long-term goal is to create a more predictable and manageable grid connection process [2].

Medium to Long-Term Goals: Non-Firm Grid Access

Charging Side Reform

Looking towards the medium to long term, METI aims to introduce non-firm grid access (ノンファーム型接続) for the charging side (forward power flow) of BESS. Non-firm access allows connection to the grid without guaranteed transmission capacity, meaning that in times of grid congestion, the BESS may be curtailed. This approach significantly reduces the cost and time associated with grid connection, as it avoids the need for immediate grid reinforcement to accommodate full firm capacity [1].

Comparison with Generation/Discharge Side

This concept of non-firm access is not entirely new to Japan's energy market; it already exists for the generation/discharge side of power sources, particularly for renewable energy generators. Extending non-firm access to the charging side of BESS will create a more symmetrical and efficient framework, further accelerating the deployment of battery storage by reducing connection barriers and costs [1].

Demand-Side Management Targets

METI's policy direction also includes ambitious targets for demand-side management (DSM) and demand-side batteries, recognizing their crucial role in a flexible energy system.

DR Targets by 2040

Japan aims to achieve Demand Response (DR) targets of 7,500–15,000 MW (750万〜1,500万kW) by 2040. DR programs incentivize consumers to reduce or shift their electricity consumption during peak demand periods, thereby alleviating grid stress and optimizing energy use [1].

Demand-Side Battery Targets by 2040

Complementing DR, the target for demand-side batteries is set at 8,000–33,000 MW (800万〜3,300万kW) by 2040. These batteries, installed at homes, businesses, and industrial facilities, can store energy and provide flexibility to the grid, further enhancing resilience and enabling greater integration of renewables [1].

Cybersecurity Considerations

With the increasing digitalization and interconnectedness of the energy grid, cybersecurity is a paramount concern. METI emphasizes that all Energy Resource Aggregation Business (ERAB) systems must comply with the ERAB Cybersecurity Guidelines. This ensures the robust protection of critical energy infrastructure from cyber threats, maintaining the reliability and security of Japan's power supply [2].

Conclusion

Japan's METI is embarking on a transformative journey for its grid-scale battery storage policy. The rapid grid connection measures, including N-1 charging stop devices and charging restrictions, coupled with OCCTO's per-operator cap, are designed to accelerate BESS deployment in the short term. The long-term vision includes the crucial introduction of non-firm grid access for the charging side, mirroring existing provisions for generation. These policy reforms, alongside ambitious demand-side management and battery targets, underscore Japan's commitment to building a flexible, resilient, and decarbonized energy system by 2040. The emphasis on 'storage-type operation' and robust cybersecurity frameworks will be instrumental in realizing these goals, positioning Japan at the forefront of grid modernization and renewable energy integration.

Comparison Table 1: Current vs. Target Capacity

| Category |

Current (April 2026) |

2040 Target |

| Grid-Scale BESS Installed Capacity |

640 MW (64万kW) |

2,800–10,000 MW (280万〜1,000万kW) |

| Contracted BESS Applications |

~30 GW (3,000万kW) |

N/A |

| Demand Response (DR) |

N/A |

7,500–15,000 MW (750万〜1,500万kW) |

| Demand-Side Battery |

N/A |

8,000–33,000 MW (800万〜3,300万kW) |

Comparison Table 2: Policy Measures and Impact

| Policy Measure |

Description |

Expected Impact |

| N-1 Charging Stop Devices |

Installation of devices that automatically halt charging during grid component failures. |

Allows early grid connection without extensive grid reinforcement. |

| Charging Restrictions |

Agreements to limit charging during grid congestion or low renewable output. |

Alleviates strain on existing grid infrastructure, accelerating connection. |

| Per-Operator Cap |

Limits the number of new connection applications each TSO can process (from Aug 2026). |

Streamlines application process and prevents backlogs. |

| Non-Firm Access (Charging Side) |

Allows grid connection without guaranteed transmission capacity (medium/long-term goal). |

Significantly reduces costs and time associated with grid connection. |

| Promoting 'Storage-Type Operation' |

Empowers TSOs to flexibly manage SoC within surplus capacity. |

Facilitates arbitrage opportunities and maximizes economic benefits. |

References